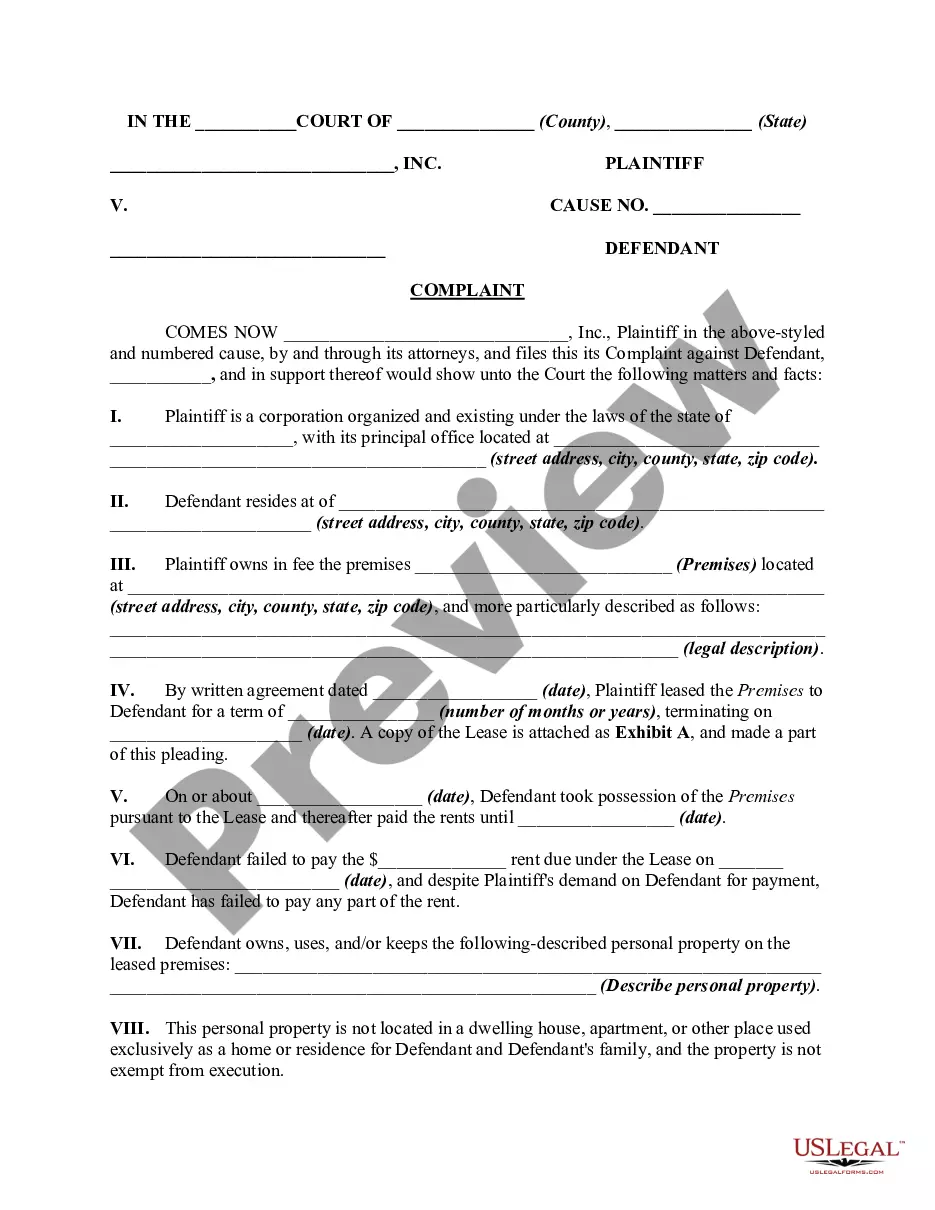

Lien Foreclosure Action With Foreclosed Property

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Complaint Or Petition To Foreclose On Mechanic's Lien?

- Log in to your US Legal Forms account. If you're a new user, begin by registering for an account.

- Browse our extensive library and use the Preview mode to check the form description and ensure it meets your needs and local jurisdiction requirements.

- If the desired form isn’t visible, use the Search feature to find a suitable template.

- Select the 'Buy Now' option and pick your preferred subscription plan to gain full access to our repository of resources.

- Complete your purchase using either your credit card or PayPal account.

- Download the document to save it on your device, allowing for easy access later in the 'My Forms' section of your profile.

By utilizing US Legal Forms, you ensure that your legal documents are not only accurate but also compliant with local regulations.

Start your journey to securing documents for your lien foreclosure action today by visiting US Legal Forms and accessing our robust library.

Form popularity

FAQ

The 120 day rule for foreclosure requires that lenders must provide a notice of default and then wait at least 120 days before proceeding with a foreclosure action. This period gives the borrower a chance to remedy the situation, either by paying the debt or negotiating terms. Adhering to this guideline is crucial in any lien foreclosure action with foreclosed property to ensure a legally sound process. Proper legal guidance can clarify these requirements.

To foreclose on a lien, you must follow specific legal steps established by your state's laws. Start by issuing a notice to the debtor, outlining their default and the impending foreclosure action on the foreclosed property. After providing necessary time for them to respond, you can then file a lawsuit to begin the foreclosure process. Utilizing a resource like US Legal Forms can simplify this process and help you obtain the right documentation.

After foreclosure, the property ownership typically transfers to the lender or the entity that initiated the foreclosure. Once the foreclosure process is complete, the lender may choose to sell the property to recover its losses. In some cases, individuals can regain ownership through redemption rights, depending on state regulations. It’s beneficial to consult experts in lien foreclosure actions with foreclosed property to explore your options.

Yes, specific liens may survive the foreclosure process, meaning they remain attached to the property despite the foreclosure sale. This is often the case with federal tax liens and certain types of special assessments. If you find yourself in a lien foreclosure action with foreclosed property, knowing which liens survive is essential for future ownership decisions. Legal guidance can help navigate these complexities.

Certain liens are not eliminated by a foreclosure sale, such as tax liens or child support liens. These liens usually follow the property and may still affect the new owner, even after a foreclosure action has taken place. Understanding the implications of these liens is crucial when dealing with foreclosed property. Engaging with resources from USLegalForms can clarify what steps to take.

To respond to a foreclosure lien, you should first review the notice you received thoroughly. Next, consider consulting a legal professional who specializes in lien foreclosure actions with foreclosed property. They can help you understand your options, such as negotiating with the lienholder or contesting the lien. Taking prompt action may lead to a more favorable outcome.

In New Jersey, tenants can typically remain in a foreclosed property for a period defined by the foreclosure process, often up to a few months after the property changes ownership. Once the new owner takes possession, they may have to go through eviction proceedings to remove tenants. Understanding your rights as a tenant during a lien foreclosure action with foreclosed property can help you navigate this situation effectively. If issues arise, seeking legal assistance can be beneficial.

The new foreclosure law in New Jersey aims to provide greater protections for homeowners facing a lien foreclosure action with foreclosed property. Recent changes require lenders to follow stricter guidelines that enhance communication and offer mediation options. These reforms intend to reduce the number of foreclosures and help homeowners find resolutions before the process escalates. Staying up to date with these laws can empower you as a homeowner.

Foreclosures in New Jersey begin with a lender filing a lien foreclosure action with foreclosed property in court. This process involves several stages, including pre-foreclosure, a court hearing, and potentially a sheriff's sale. Homeowners may have options to negotiate their mortgage terms or participate in mediation during the process. Awareness of how foreclosures work can help homeowners make informed decisions.

A house in New Jersey typically stays in pre-foreclosure for about 3 to 6 months, depending on various factors. During this time, the lender has filed a lien foreclosure action with foreclosed property, and the homeowner may still have opportunities to repay the debt or sell the house. It's essential to stay informed and seek options for avoiding foreclosure during this crucial period. Being proactive can greatly influence your situation.