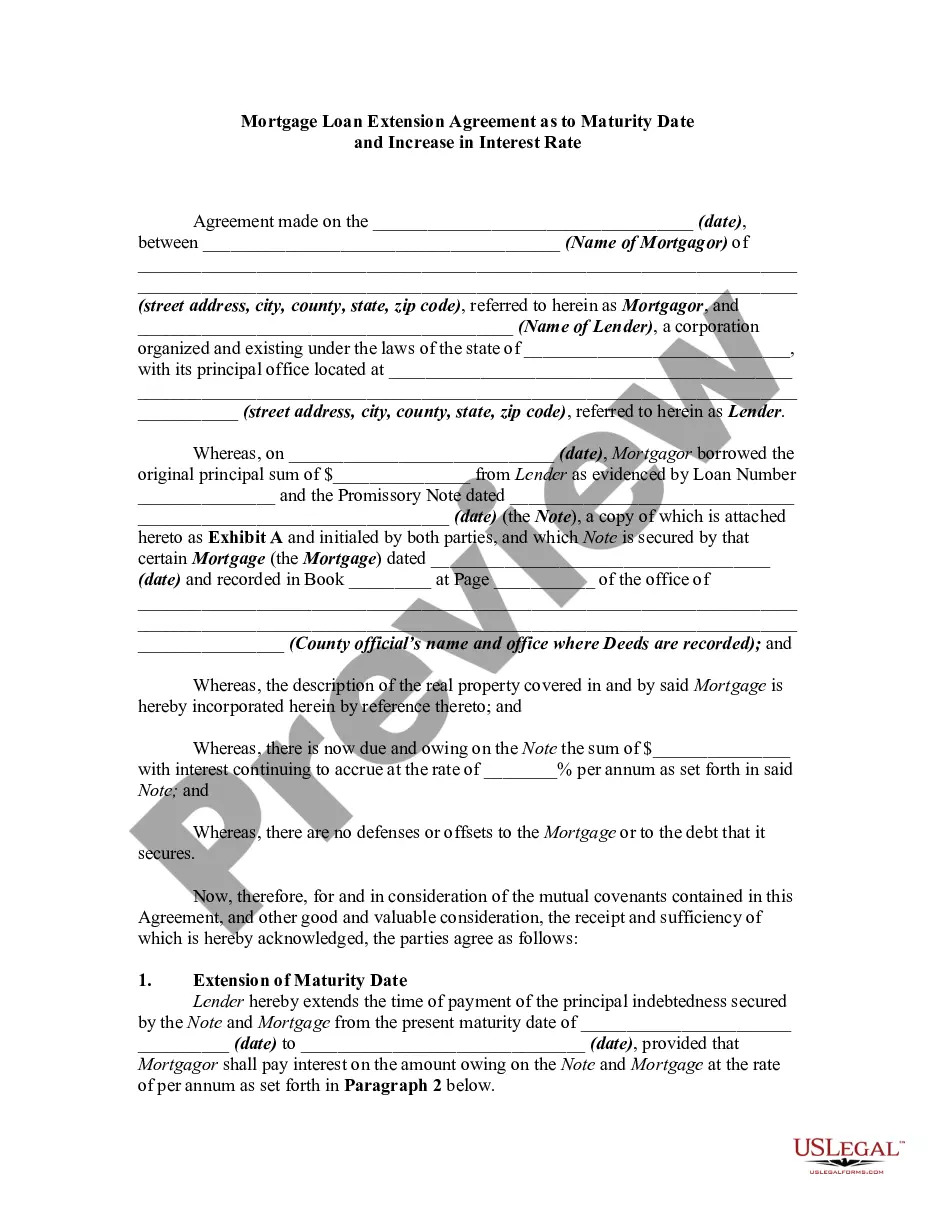

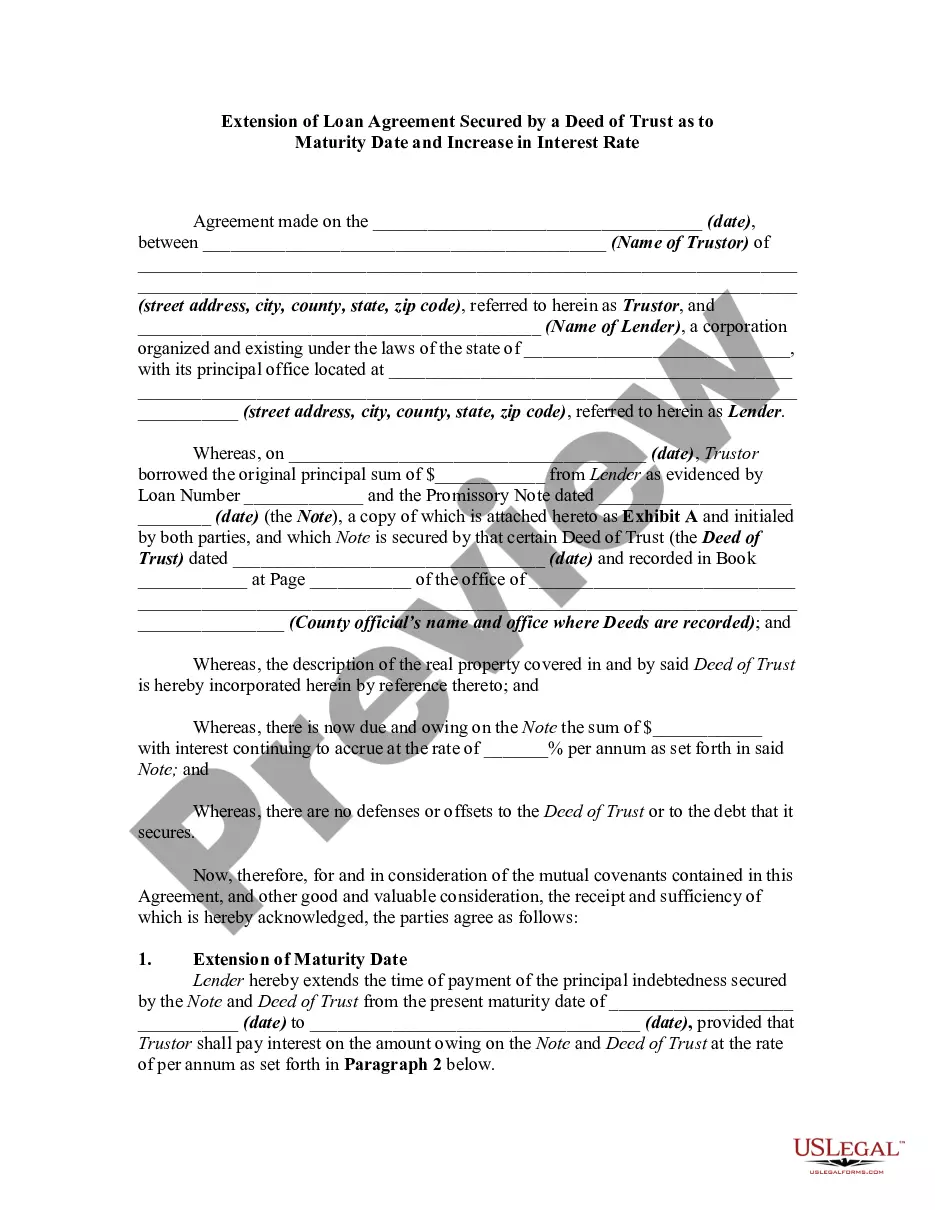

Second Mortgage For Extension

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

- Login to your US Legal Forms account or create a new one if you're a first-time user.

- Browse through the extensive online library to find the specific form related to a second mortgage for extension.

- Use the Preview mode to ensure you select the correct document suited to your needs and local jurisdiction.

- If necessary, utilize the Search tab to find additional templates that may better fit your requirements.

- Click the 'Buy Now' button next to your chosen document and select your preferred subscription plan.

- Complete your purchase by entering your payment details or using PayPal for convenience.

- Download your form and save it on your device, ensuring easy access anytime through the 'My Forms' section in your profile.

US Legal Forms empowers you with a streamlined process for acquiring the correct legal documentation. This ensures that every step you take towards your second mortgage for extension is legally sound and efficient. With premium support available, you can have confidence in your completed documents.

Start today and unlock the potential of your home with US Legal Forms!

Form popularity

FAQ

In some cases, you may be able to write off a second mortgage for extension, particularly if the funds were used for home improvements. It's crucial to understand the IRS guidelines regarding mortgage interest deductions, as they can vary. Seeking advice from a financial consultant can provide clarity on what options are available to you.

The disadvantages of a second mortgage for extension include higher monthly payments and the risk of losing your home if you default. Additionally, it can lead to increased financial strain if not managed carefully. Evaluate your financial stability and consider alternatives before proceeding with a second mortgage.

Yes, you can extend an existing mortgage term through refinancing, which may include rolling in a second mortgage for extension. This option can lower your monthly payment, giving you financial breathing room. Be sure to explore various lenders and their terms to find the best fit for your needs.

A second mortgage for extension can be a good idea if you plan to use the funds wisely, such as for necessary home improvements or consolidating higher-interest debts. Always assess your financial landscape before proceeding, as this decision introduces further obligations. A clear repayment strategy can make this option more suitable for your circumstances.

The average term of a second mortgage for extension typically ranges from five to 15 years. Lenders often offer various terms based on your creditworthiness and financial profile. It is essential to find a term that aligns with your financial goals and repayment capabilities.

Taking out a second mortgage for extension can be a beneficial option if you need additional funds for home improvements or debt consolidation. However, you should carefully consider your financial situation and the potential risks involved, as you are adding another layer of debt. Analyze your ability to repay both loans before committing to this decision.

To qualify for a second mortgage, you need to demonstrate strong financial health. This includes a good credit score, a manageable debt-to-income ratio, and sufficient equity in your home. Platforms like UsLegalForms can help you understand the documentation and processes required to make your application for a second mortgage for extension easier.

The process of acquiring a second mortgage can be more challenging compared to a first mortgage. Lenders may have strict criteria due to the increased risk involved. However, if you research and understand the requirements, you can navigate these challenges and successfully obtain a second mortgage for extension.

A key downside to a second mortgage is the increased financial burden it adds. You will have to manage additional monthly payments, which can strain your budget. Moreover, if you cannot meet these payments, you risk losing your home. Hence, careful consideration is essential before pursuing a second mortgage for extension.

Getting approved for a second home can present some challenges, especially if your financial circumstances are not optimal. Lenders will scrutinize your credit profile and income. However, if you present a solid financial picture, you may find getting a second mortgage for extension to be an attainable goal.