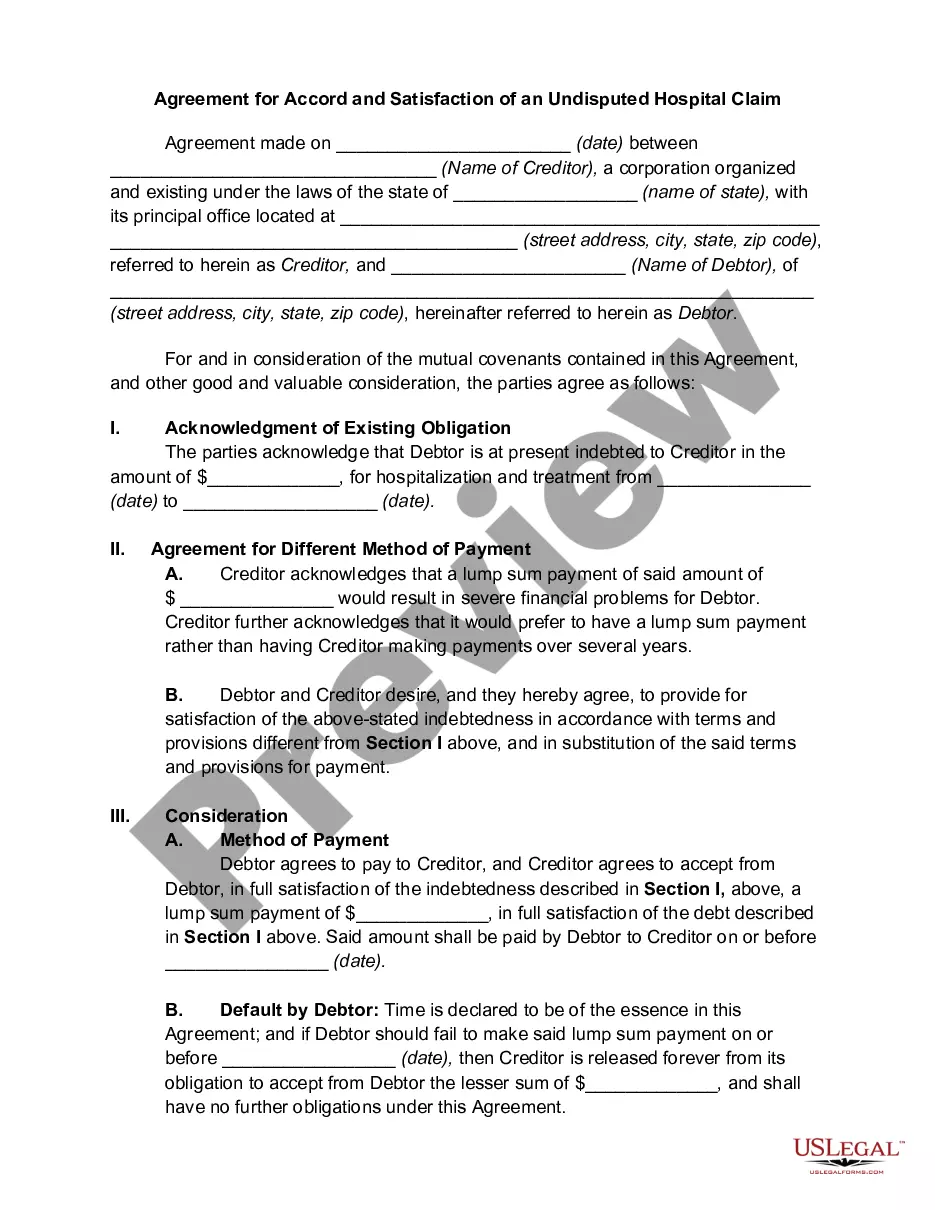

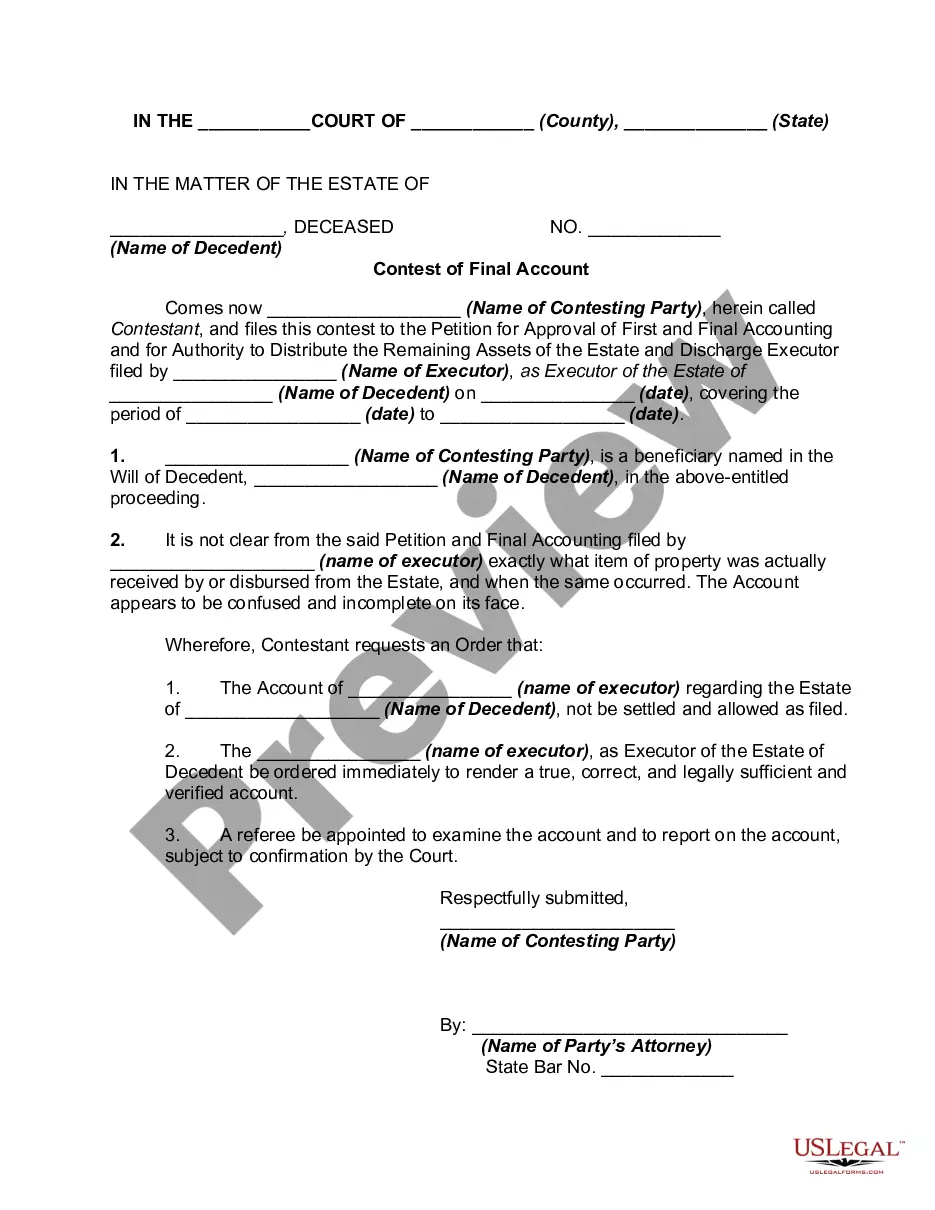

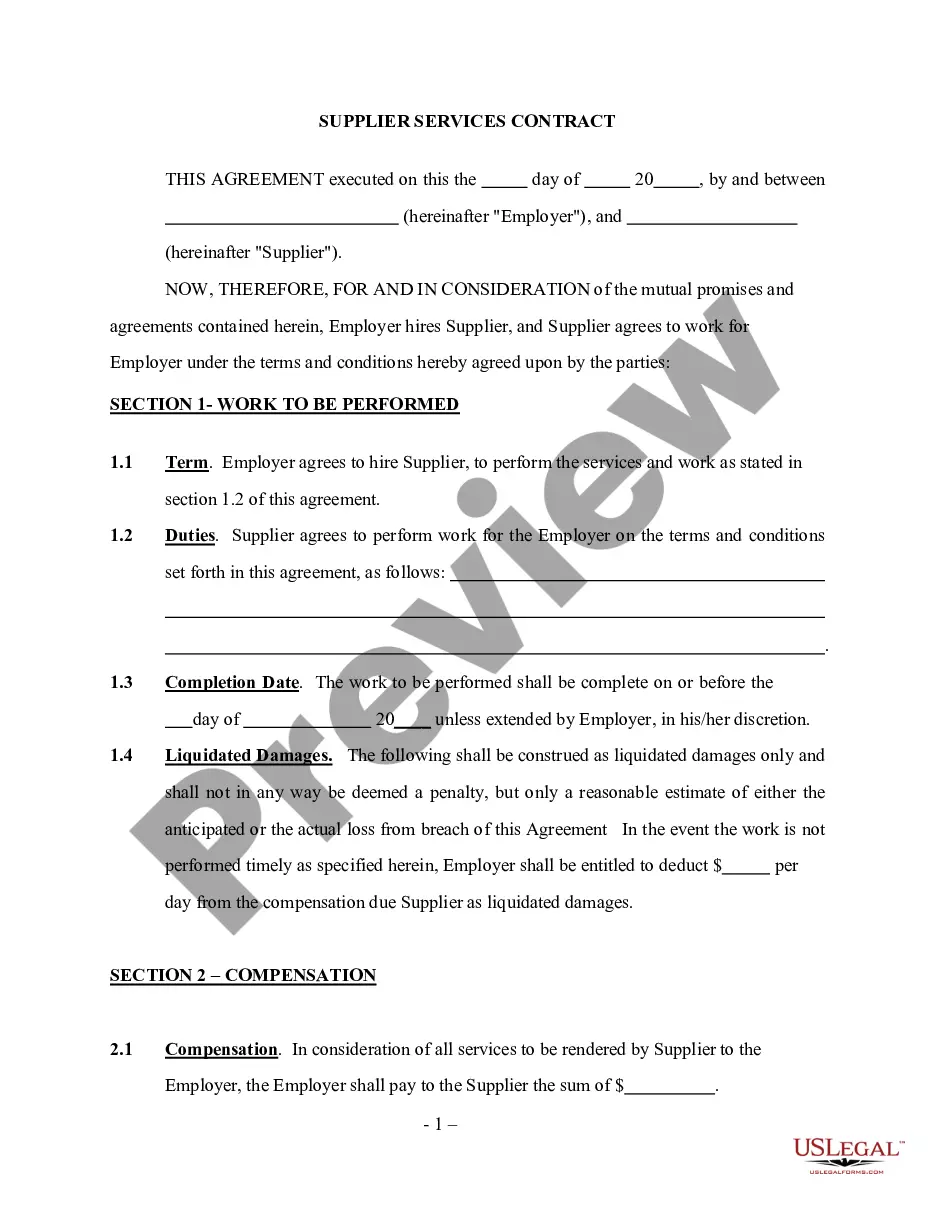

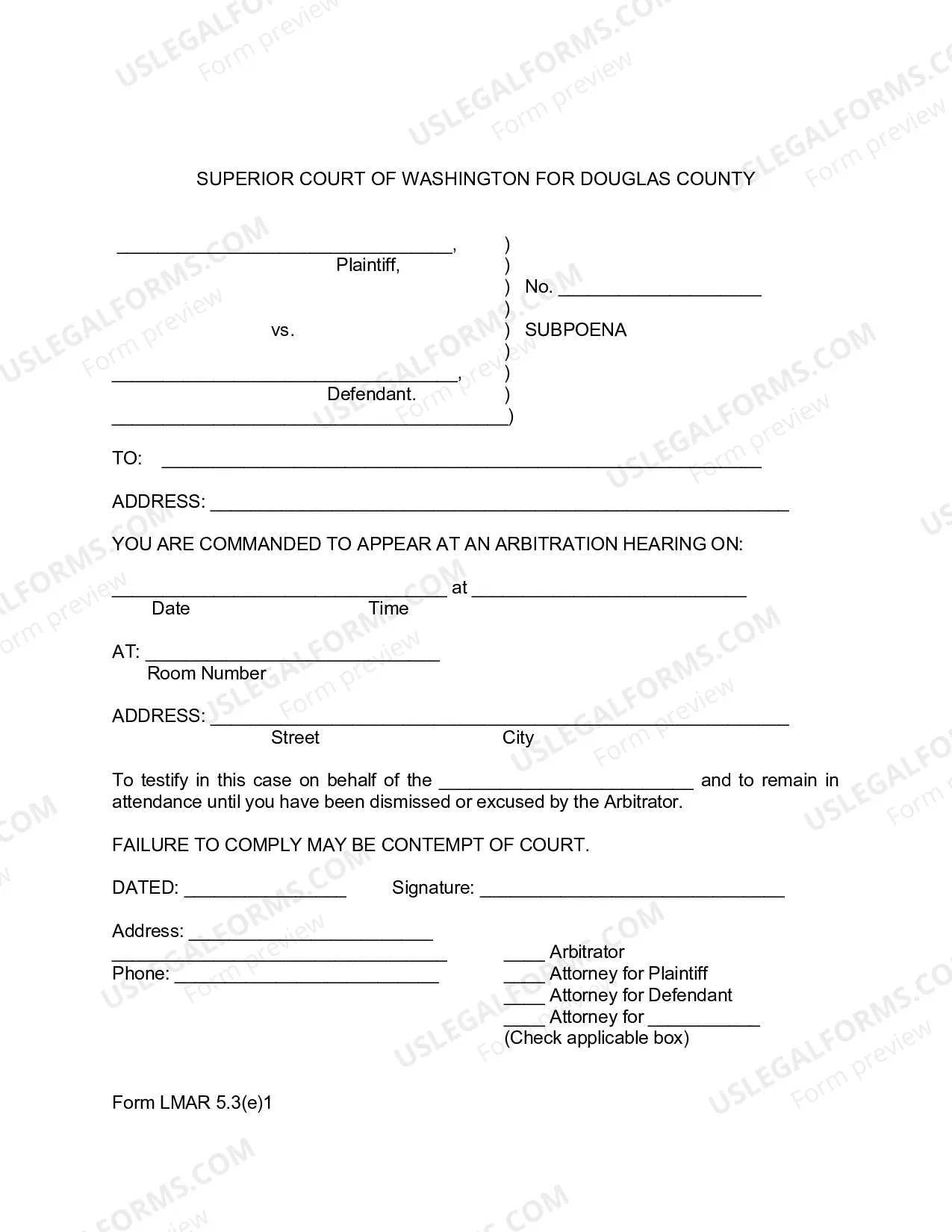

Debt Covered With Interest

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

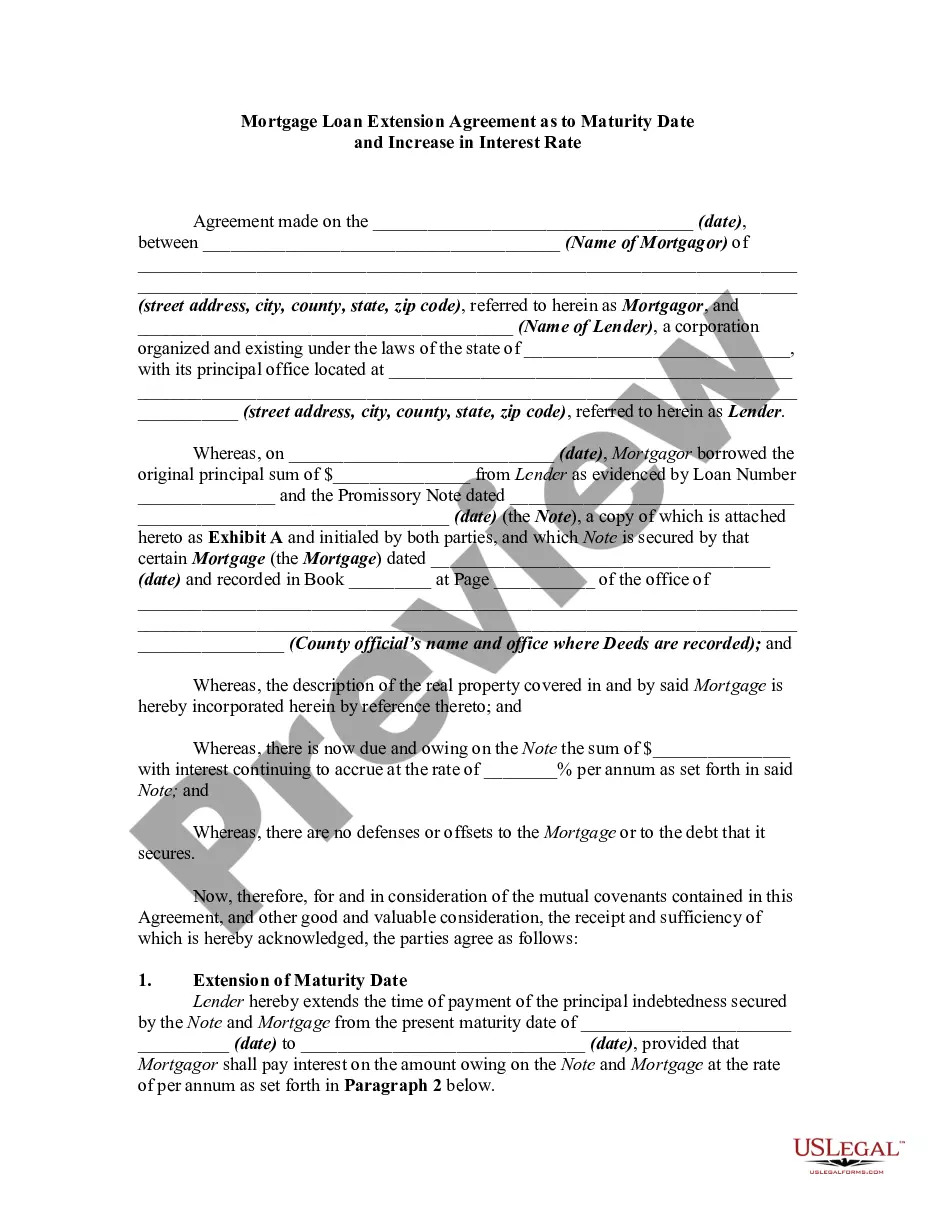

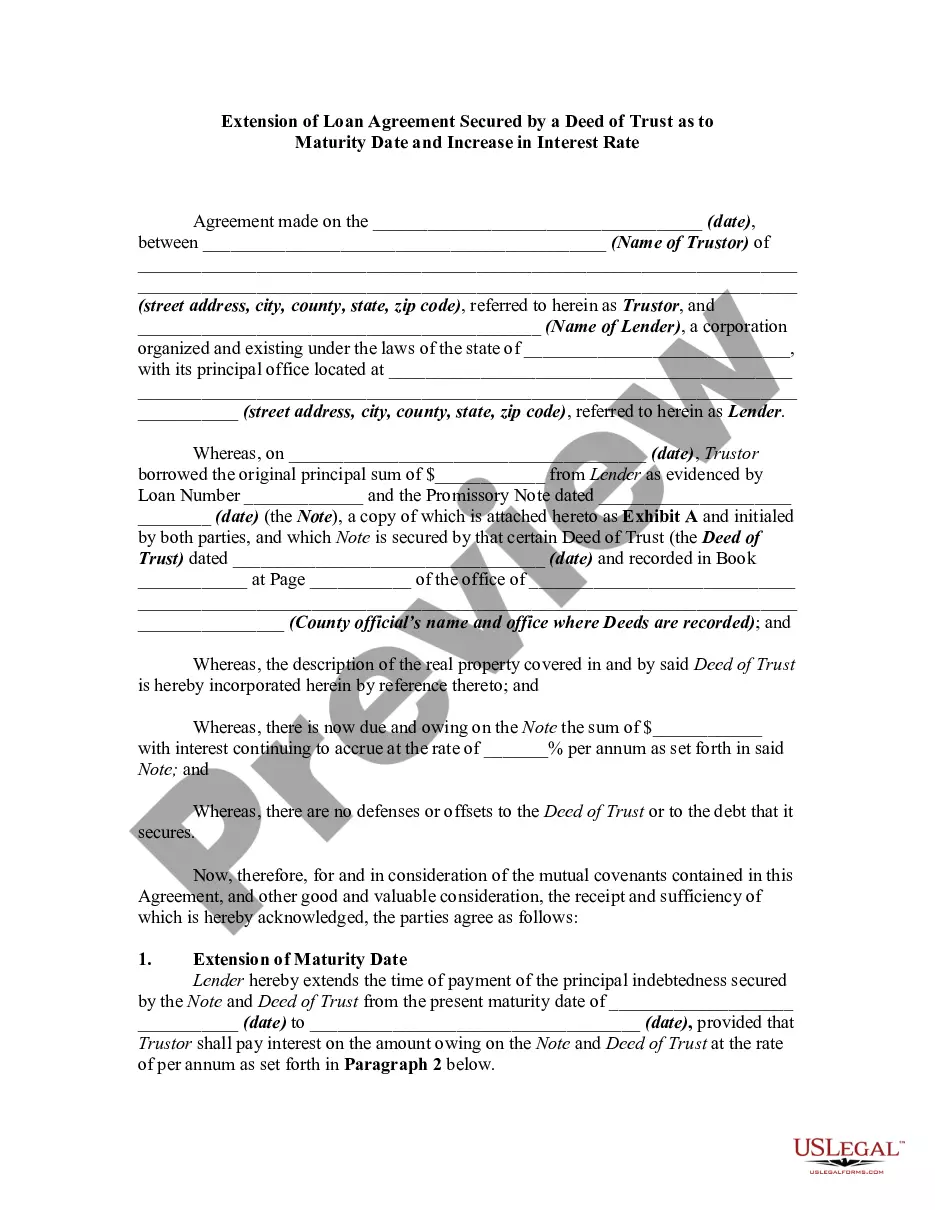

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

Handling legal documents and processes may be a lengthy addition to your routine.

Debt Managed With Interest and similar forms generally require you to search for them and comprehend the best method to fill them out correctly.

Thus, whether you are managing financial, legal, or personal affairs, utilizing a comprehensive and user-friendly online compilation of forms when necessary will significantly assist you.

US Legal Forms is the leading online platform for legal documents, featuring over 85,000 state-specific forms and various tools that will aid you in completing your paperwork swiftly.

Simply Log In to your account, search for Debt Managed With Interest, and download it immediately from the My documents section. You may also access previously saved documents.

- Explore the collection of relevant documents available to you with just one click.

- US Legal Forms provides you with state- and county-specific documents available for download at any time.

- Safeguard your document management procedures with a high-quality service that allows you to prepare any document in minutes without additional or concealed fees.

Form popularity

FAQ

There are several reasons why you might not qualify for debt consolidation, including a low credit score, insufficient income, or being in default on existing debts. Sometimes, if your debt covered with interest is too high relative to your income, this can also hinder your chances. It’s important to evaluate your financial situation and consider speaking with an expert at uslegalforms to explore various solutions that could work for you.

Most lenders prefer a credit score of at least 600 when considering debt consolidation loans. However, higher credit scores can lead to better interest rates and terms. If your debt covered with interest appears manageable and you show potential for repayment, the right lender, such as those available through uslegalforms, can guide you in securing favorable consolidation options.

Yes, you can accrue interest on your debt. Most loans and credit cards calculate interest on the outstanding balance, which means that the total amount owed can increase over time, particularly if you miss payments or only make the minimum payment. Understanding how debt covered with interest works is crucial, as it will help you make informed decisions about managing your finances and avoiding accumulating unnecessary debt.

To qualify for debt consolidation, you typically need to have a steady income, existing debt that you want to consolidate, and a good understanding of your financial situation. Debt covered with interest can often be managed more effectively through consolidation, as it combines multiple debts into a single monthly payment. Additionally, lenders look for responsible financial habits, so maintaining a consistent payment history can be beneficial.

You can write off interest on debt as long as the debt was incurred for business or investment purposes. This deductible interest falls under debt covered with interest, allowing you to lower your taxable income. Proper documentation must be maintained to support these deductions. For an organized approach to managing your deductions, consider using USLegalForms' solutions.

Yes, you can typically write off interest on bad debt, provided that you meet specific IRS criteria. This allows you to deduct the interest that you can no longer collect from your debtor, which is considered debt covered with interest. Ensure that you retain proper documentation to substantiate your claim. If you need guidance on this, USLegalForms provides resources to assist with your tax-related questions.

Interest coverage is a crucial factor in assessing your financial stability. A high interest coverage ratio indicates that you can comfortably meet your interest obligations, which is a positive sign for your financial health. Conversely, a low ratio may suggest difficulties in managing debt. Therefore, understanding interest coverage is vital when dealing with debt covered with interest.

Interest coverage measures a borrower's ability to meet interest payments on outstanding debt. For example, if your earnings are sufficient to cover interest payments several times over, you demonstrate strong financial health. This ratio helps creditors assess the risk involved in lending to you. Remember, understanding interest coverage is important when looking at debt covered with interest.

Yes, many types of debt come with interest charges. Lenders typically apply interest to loans, credit cards, and mortgages, which means you owe more than the principal amount borrowed. Understanding how interest works can help you manage your financial obligations effectively. With debt covered with interest, being aware of repayment terms is crucial.

The formula for calculating interest on a debt is simple: Interest = Principal x Rate x Time. Here, the principal refers to the original amount owed, the rate is the interest percentage, and the time could be in years. Using this formula can help you determine how much interest will accumulate on your debt covered with interest. Accurate calculations can help you plan your finances better.