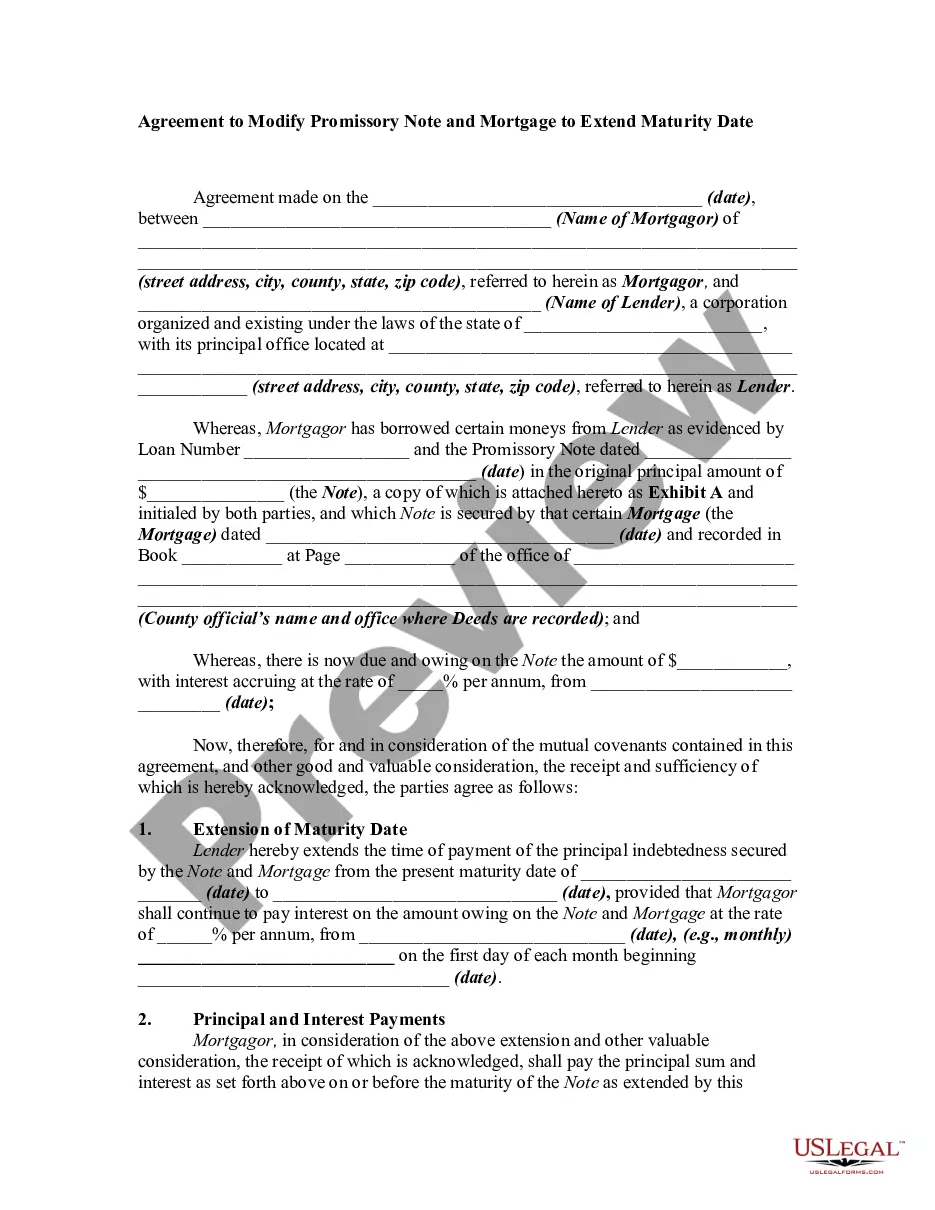

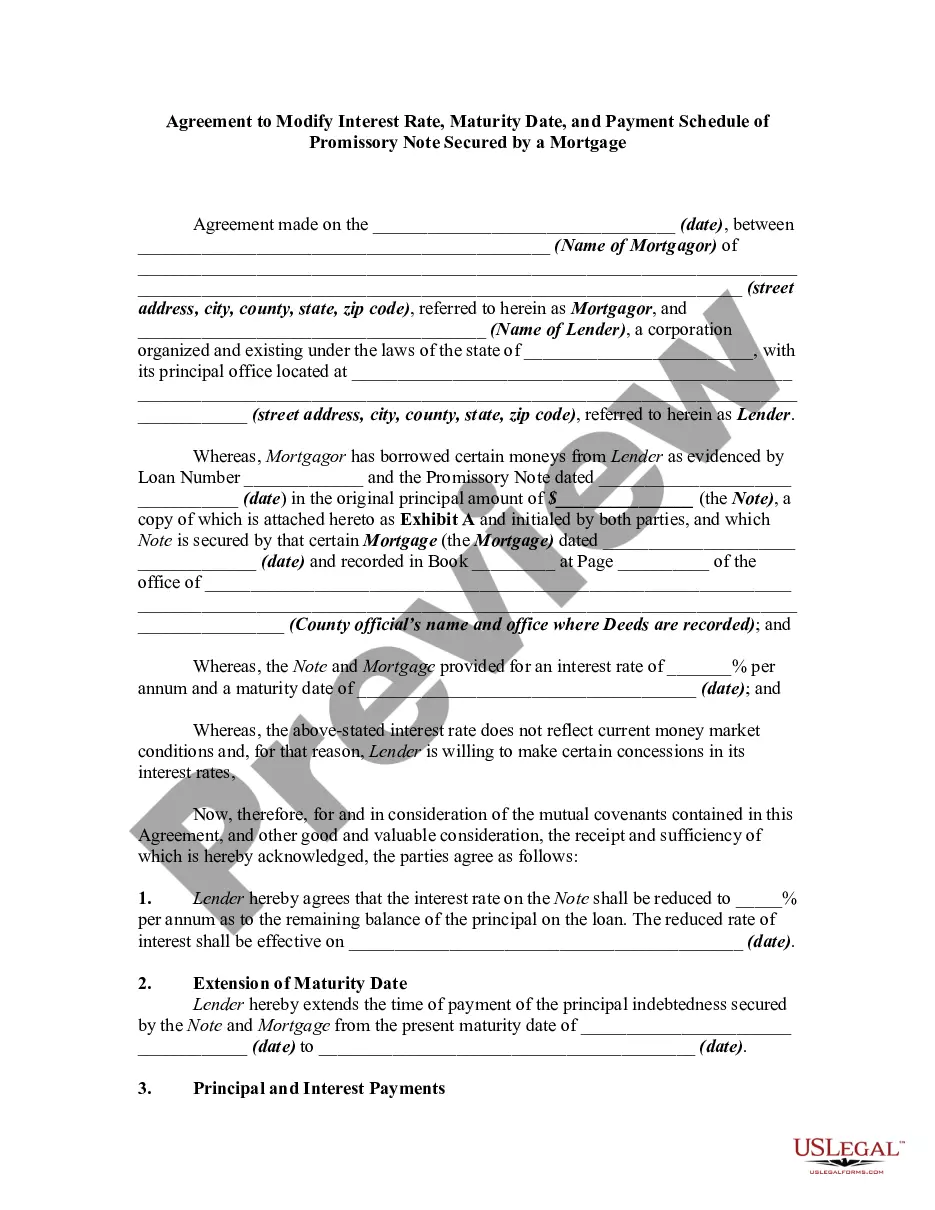

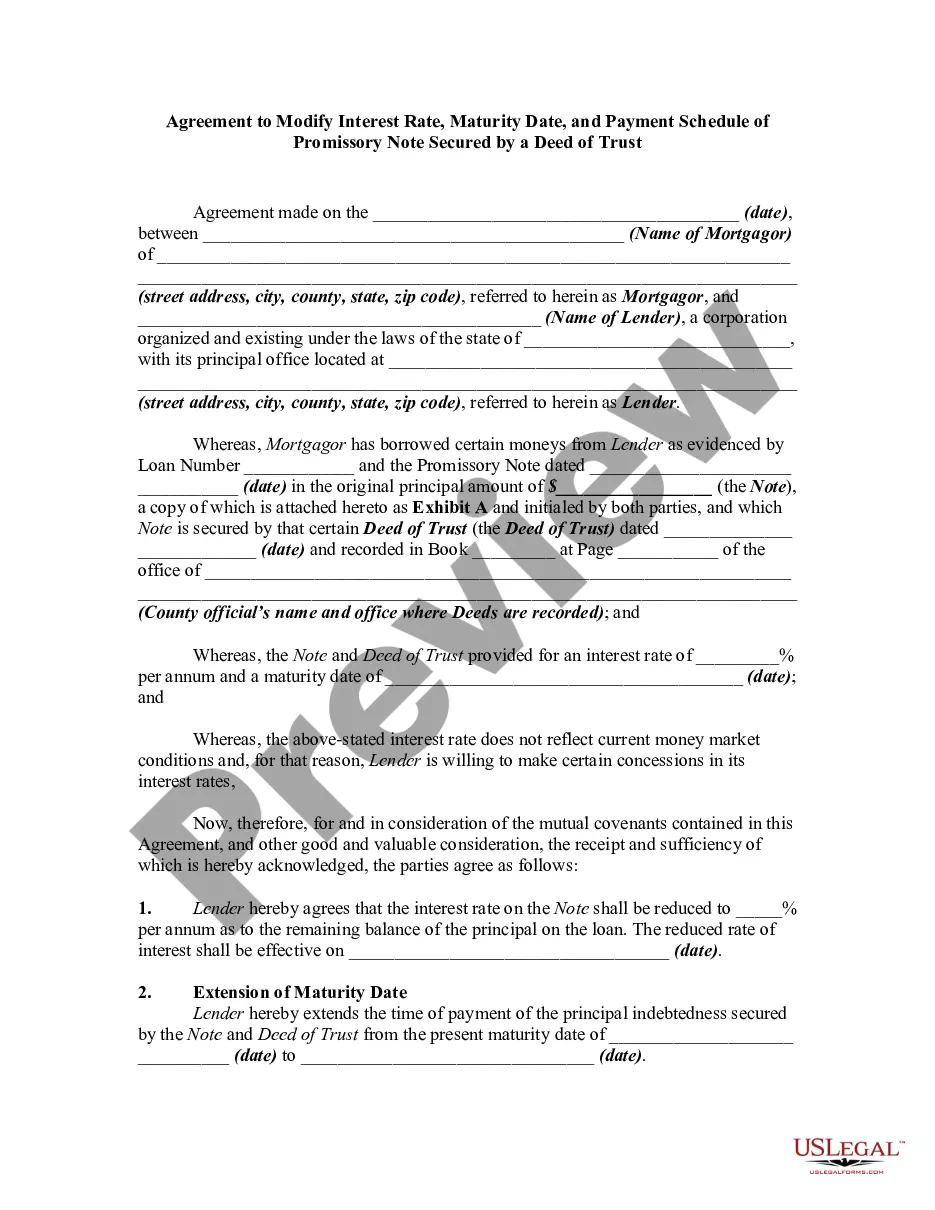

Modify By Mortgage Formula

Description

How to fill out Agreement To Modify Interest Rate On Promissory Note Secured By A Mortgage?

It's clear that you cannot become a legal authority instantly, nor can you acquire the ability to swiftly draft Modify By Mortgage Formula without a specialized background.

Drafting legal documents is a lengthy endeavor that demands specific education and expertise.

So why not entrust the drafting of the Modify By Mortgage Formula to the specialists.

Select Buy now. Once the payment is finalized, you can download the Modify By Mortgage Formula, fill it out, print it, and send or mail it to the specified individuals or entities.

You can access your documents again from the My documents tab at any moment. If you are a current client, you can simply Log In, locate, and download the template from the same tab.

- Start with our website to obtain the document you need in just minutes.

- Locate the form you require using the search bar at the top of the page.

- Preview it (if this option is available) and review the accompanying description to ascertain if Modify By Mortgage Formula is what you're seeking.

- Restart your search if you need another template.

- Create a free account and select a subscription option to acquire the form.

Form popularity

FAQ

To do a mortgage modification, begin by contacting your lender to discuss your options, explaining your current financial situation. You may need to provide documentation that supports your request, such as income statements and bank statements. After your lender reviews your application, they will inform you of the modification terms, which you can assess and negotiate as needed. Using uslegalforms can streamline this process and clarify necessary paperwork.

A common example of a mortgage modification is changing the interest rate on your existing mortgage to reduce monthly payments. For instance, if you secure a lower interest rate through negotiation, you can modify by mortgage formula to calculate your new payment. This adjustment helps make homeownership more affordable and manageable. You may want to consider using uslegalforms to understand the steps better.

To fill out a mortgage form, start by gathering necessary information such as your income, debts, and credit history. Next, carefully input this data into the required fields, ensuring accuracy and completeness. It helps to refer to a template or resources, like those provided by uslegalforms, to simplify the process. Finally, double-check your information before submitting the form to ensure everything is correct.

When you take a loan modification, you change the terms of your loan directly through your lender. Most lenders agree to modifications only if you're at immediate risk of foreclosure. A loan modification can also help you change the terms of your loan if your home loan is underwater.

One of the main factors a lender takes into consideration for loan modifications is the borrower's debt-to-income ratio. This is the ratio of gross monthly income (before taxes) to total mortgage payment. Lenders vary in the maximum debt ratios they'll accept, but are generally in the 36 percent to 45 percent range.

How To Calculate Your Mortgage Payment - YouTube YouTube Start of suggested clip End of suggested clip And all of this is going to be divided. By 1 minus 1 plus r over n raised to the negative NT.MoreAnd all of this is going to be divided. By 1 minus 1 plus r over n raised to the negative NT.

How do I calculate my debt-to-income ratio? To calculate your DTI, you add up all your monthly debt payments and divide them by your gross monthly income. Your gross monthly income is generally the amount of money you have earned before your taxes and other deductions are taken out.