Form To Dissolve Trust With Hmrc

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

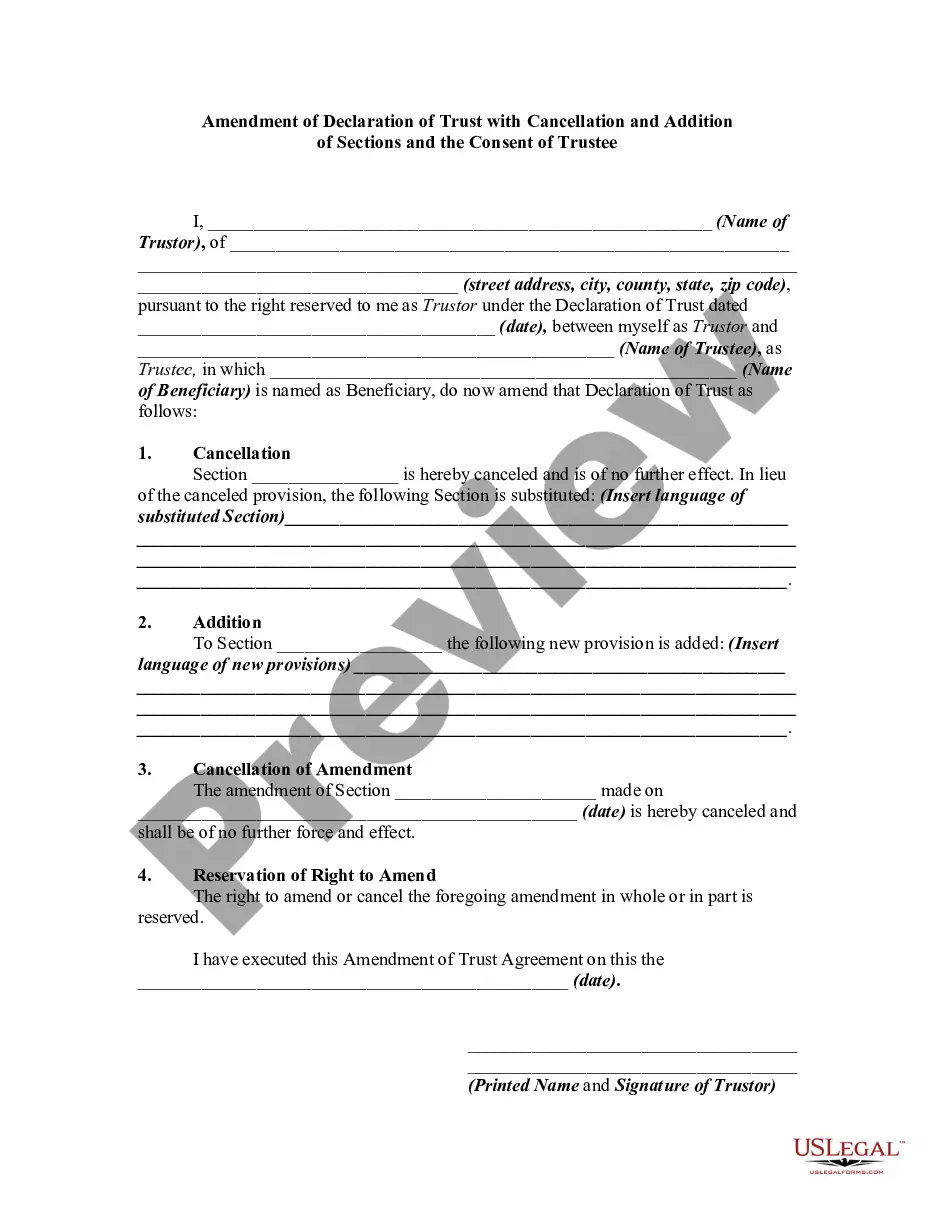

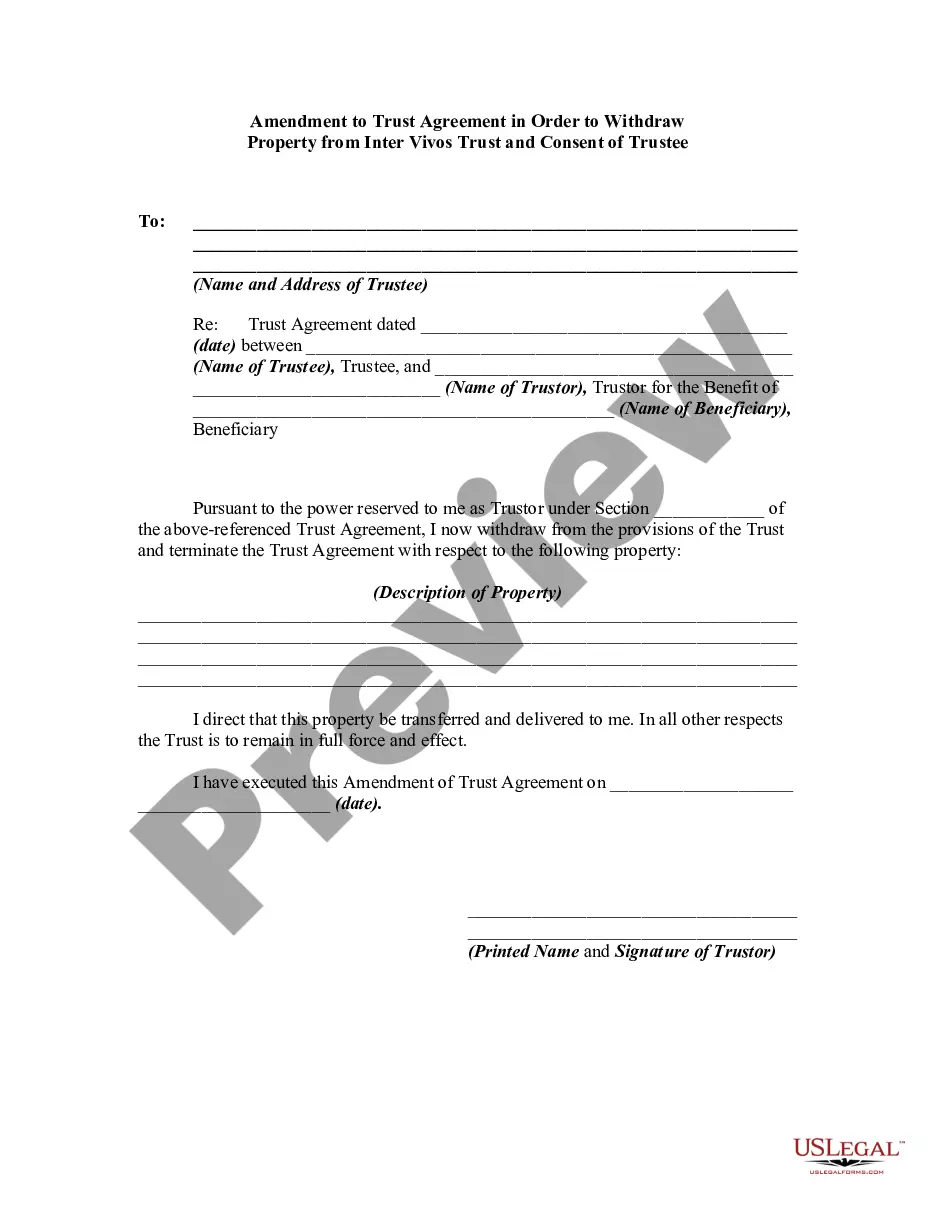

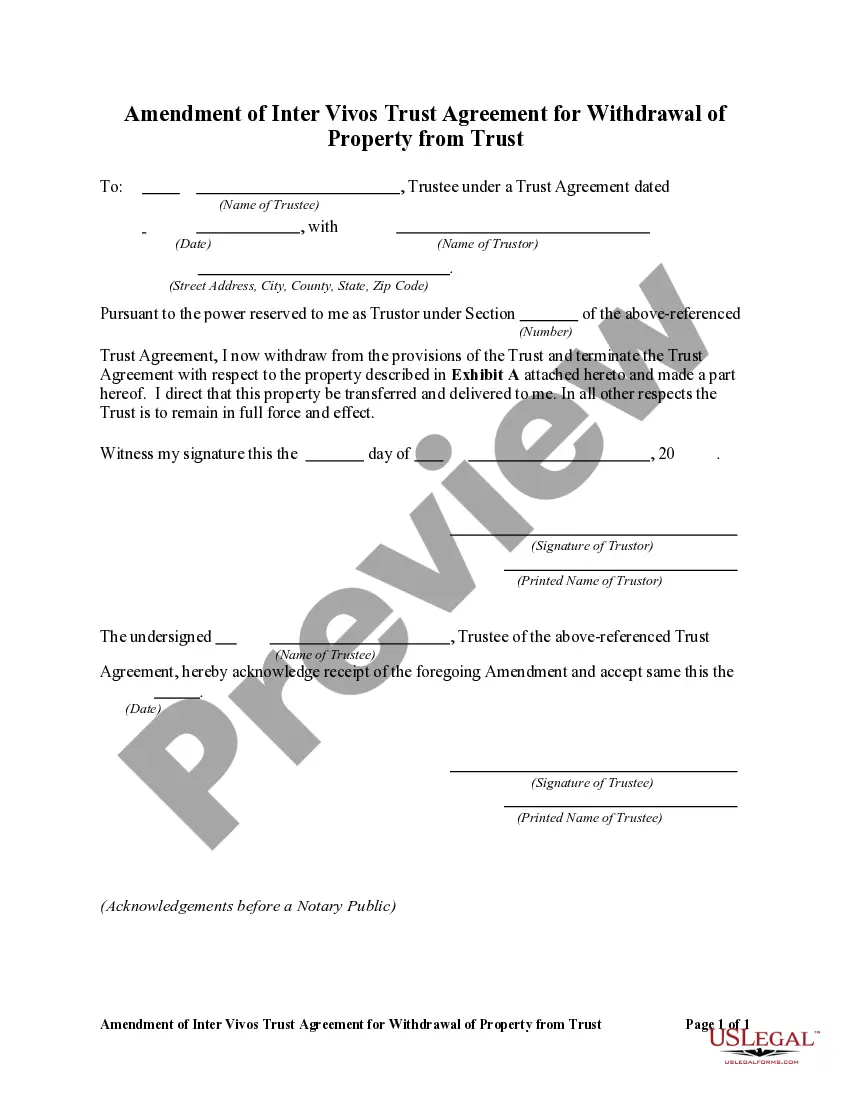

How to fill out Amendment Of Trust Agreement And Revocation Of Particular Provision?

Regardless of whether for commercial reasons or personal matters, everyone eventually encounters legal issues at some point in their life. Completing legal documents requires meticulous attention, starting from selecting the appropriate form template. For instance, if you opt for an incorrect version of a Form To Dissolve Trust With Hmrc, it will be rejected upon submission. Thus, it is crucial to have a reliable source of legal documents like US Legal Forms.

If you need to obtain a Form To Dissolve Trust With Hmrc template, adhere to these simple steps: Obtain the sample you require by using the search bar or catalog navigation. Review the form’s description to confirm it aligns with your situation, state, and locality. Click on the form’s preview to examine it. If it is the wrong document, return to the search feature to find the Form To Dissolve Trust With Hmrc sample you need. Download the template when it fits your requirements.

- If you have a US Legal Forms account, simply click Log in to access previously saved templates in My documents.

- If you do not possess an account yet, you can acquire the form by clicking Buy now.

- Choose the appropriate pricing option.

- Complete the account registration form.

- Select your payment method: use a credit card or PayPal account.

- Choose the file format you desire and download the Form To Dissolve Trust With Hmrc.

- Once it is downloaded, you can fill out the form using editing software or print it and complete it manually.

- With a vast US Legal Forms catalog available, you do not have to waste time searching for the right sample across the internet.

- Utilize the library’s user-friendly navigation to find the correct form for any circumstance.

Form popularity

FAQ

You can tell HMRC you're leaving through your Self Assessment tax return. Complete the 'resident' section (form SA109) and send it by post. You cannot use HMRC 's online services to tell them you're leaving the UK.

The transferee must have been a beneficiary of the trust when the property was acquired and became an asset of the trust (i.e. the relevant time). There must be no consideration for the transfer and the transfer of property from trustee to beneficiary must not be part of a sale or other arrangement.

Distribute trust assets outright The grantor can opt to have the beneficiaries receive trust property directly without any restrictions. The trustee can write the beneficiary a check, give them cash, and transfer real estate by drawing up a new deed or selling the house and giving them the proceeds.

Terminating an irrevocable trust can have significant tax consequences, triggering a combination of income, capital gains and estate taxes. Hence, understandingthese implications along with exploring alternative solutions is critical before deciding to dissolve a trust.

The trust deed may stipulate that a simple resolution will suffice for winding up the trust, but more commonly a new deed is necessary to close the trust and distribute the trust assets. The deed should be drawn up by a solicitor and signatures must be witnessed.