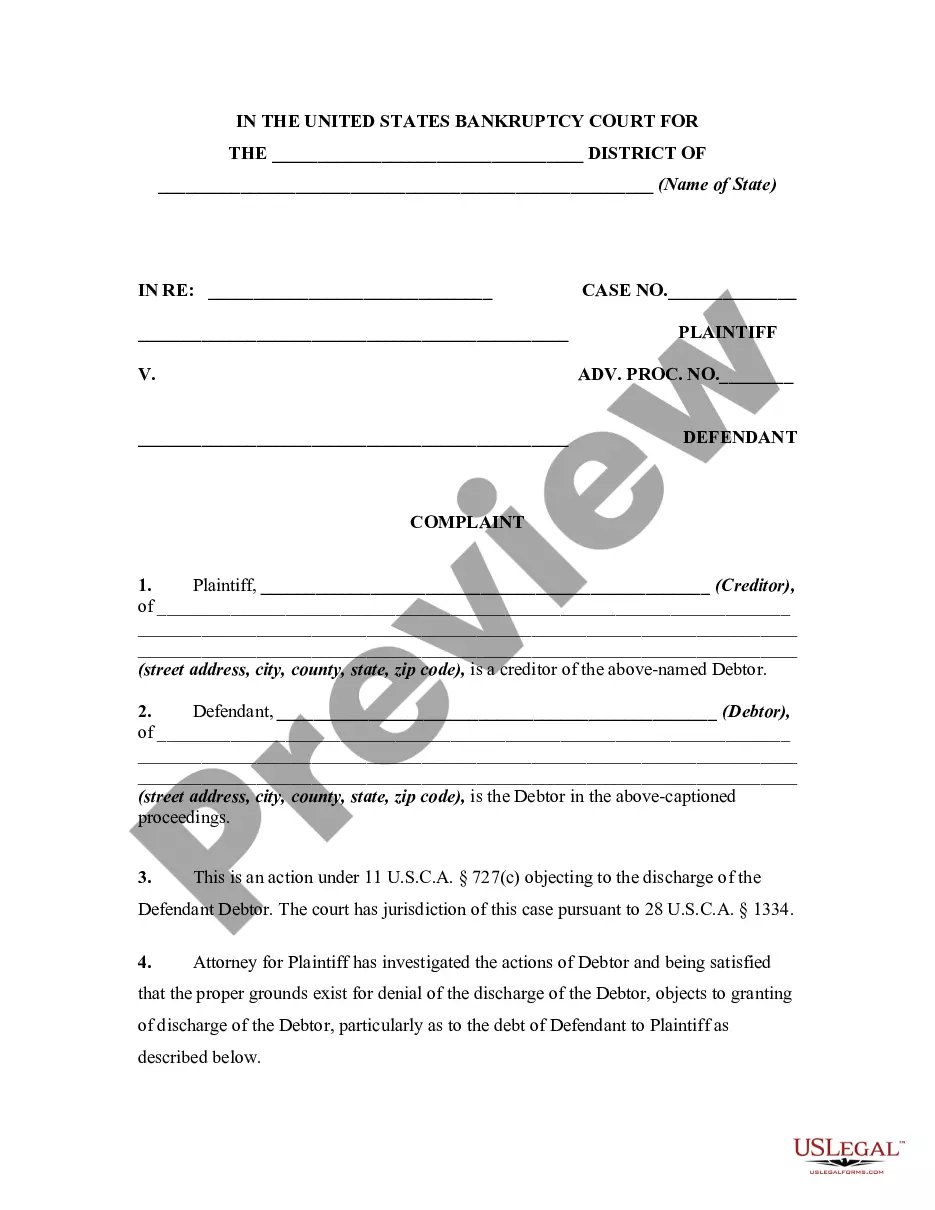

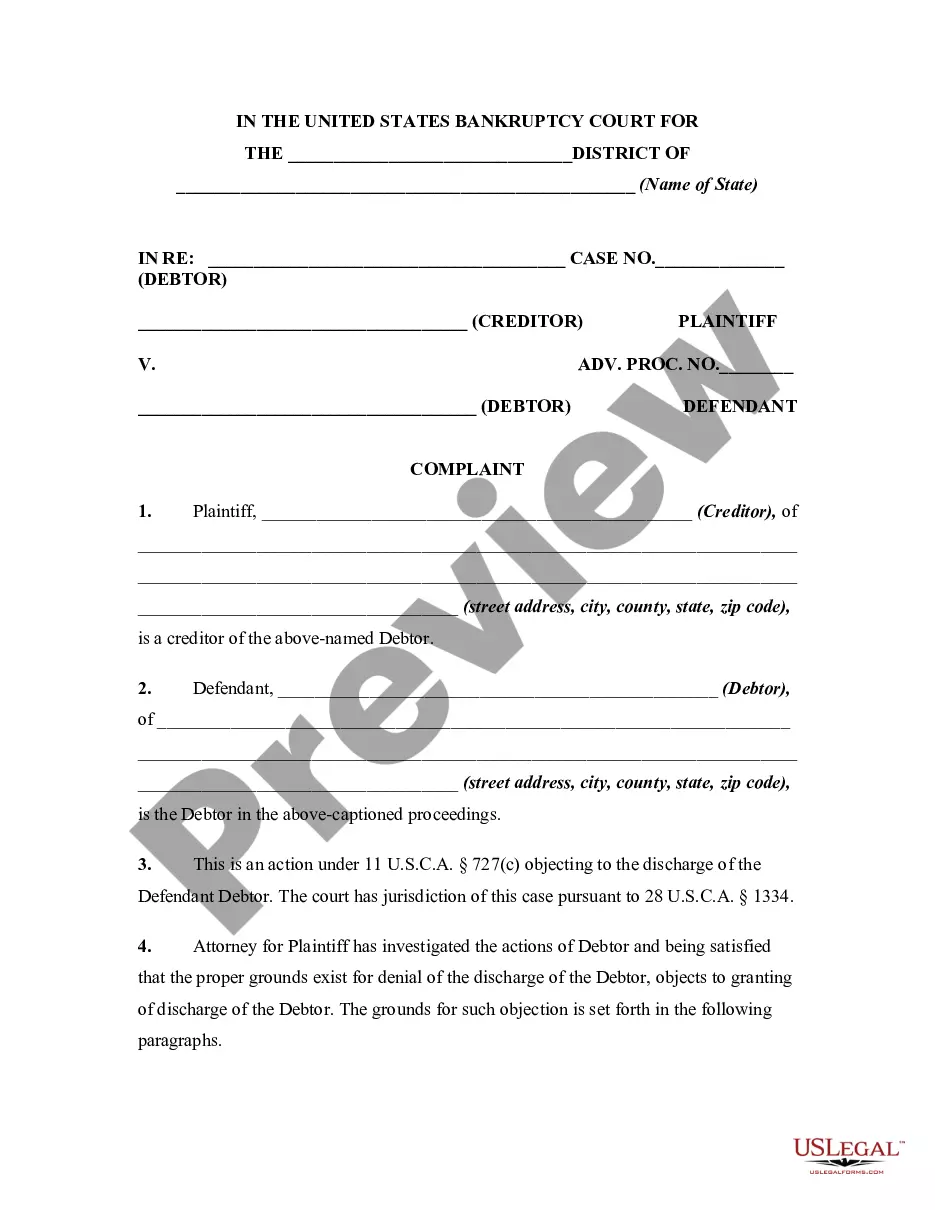

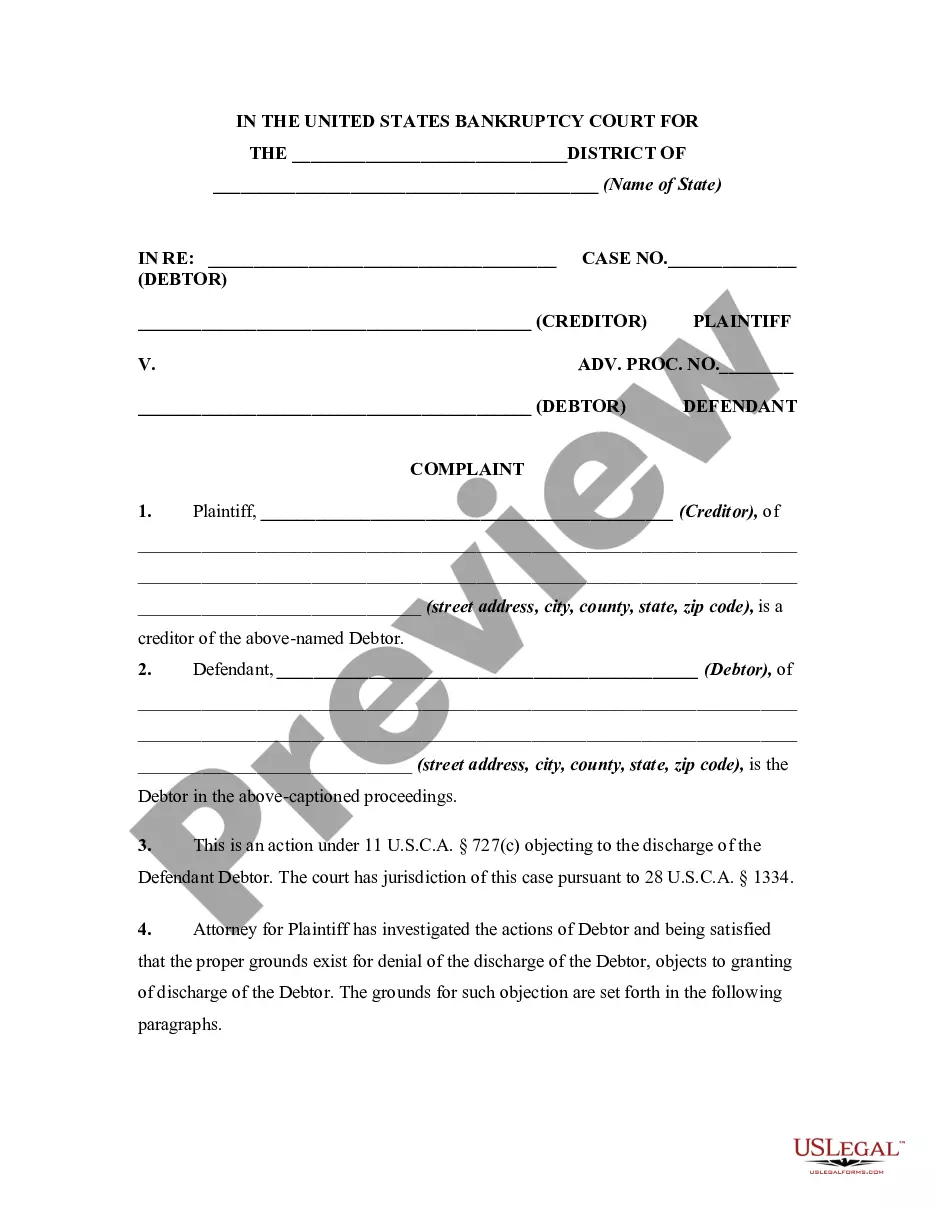

Discharge Date For Bankruptcy

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Complaint Objecting To Discharge In Bankruptcy Proceedings For Concealment By Debtor And Omitting From Schedules Fraudulently Transferred Property?

- Log in to your account on US Legal Forms. If you’re a new user, create an account to get started.

- Use the Preview feature to review the form description. Verify it matches your requirements according to your jurisdiction.

- If needed, utilize the Search tab to look for additional templates that might better suit your situation.

- Once you've found the right form, click on the Buy Now button to select your preferred subscription plan.

- Complete your purchase by entering your payment details or using your PayPal account.

- Download the completed form to your device and access it anytime through the My Forms menu in your profile.

By following these easy steps, you’ll be able to efficiently navigate the US Legal Forms library. The service offers an extensive collection of over 85,000 fillable and editable legal forms, empowering you to handle your legal needs with confidence.

Ready to streamline your legal document creation? Visit US Legal Forms today and take advantage of our comprehensive resource library!

Form popularity

FAQ

The 180-day rule in Chapter 7 refers to the period during which certain debts may not be discharged if they were incurred shortly before filing for bankruptcy. Essentially, if you obtain new debt within 180 days of your bankruptcy discharge date, you might still be responsible for that debt. This rule helps prevent individuals from abusing the bankruptcy system by incurring large debts shortly before seeking relief. Understanding this rule can guide you in managing your finances and debt obligations effectively.

A bankruptcy dismissal date occurs when a bankruptcy case is closed without a discharge granted to the debtor. This usually happens when the court dismisses the case due to issues such as failure to meet requirements or fraud. The dismissal date can significantly impact your finances, as it indicates that your debts remain enforceable. For assistance navigating these processes, consider using USLegalForms as a helpful resource.

To find a bankruptcy discharge date, you can check your bankruptcy paperwork or contact the court where you filed. It is also listed in the notice sent to creditors after your discharge is granted. Additionally, using USLegalForms can simplify this process, allowing you to access necessary documents efficiently. Knowing your discharge date is crucial for managing your credit and financial obligations.

The discharge date for Chapter 7 bankruptcy occurs roughly three to six months after filing for bankruptcy. This date signifies when the court formally releases you from liability for certain debts. Understanding your discharge date can help you manage your finances effectively and plan for your financial future. Once discharged, you can begin to rebuild your credit and regain financial independence.

Yes, the discharge date for bankruptcy does appear on your credit report. Typically, it stays on your record for about seven to ten years, depending on the type of bankruptcy you filed. This marks the conclusion of the bankruptcy process and can affect your credit score. However, having a discharge can provide relief from debt and give you a fresh start.

Declaring bankruptcy can lead to loss of certain assets, such as property and vehicles, depending on local laws and exemptions. You may also experience a negative impact on your credit score for several years. However, understanding the discharge date for bankruptcy can help you manage those losses and work toward a better financial future. Platforms like US Legal Forms can guide you through the process, ensuring you understand what to expect.

The discharge date for bankruptcy marks the moment your debts are wiped clean, while the dismissal date indicates that your bankruptcy case was closed without eliminating your debts. Knowing the discharge date for bankruptcy is crucial because it offers you a clean slate, whereas a dismissal usually leaves you with lingering obligations. Understanding these dates helps you take appropriate steps toward financial recovery.

When your bankruptcy is discharged, you receive a fresh start. Most of your debts get eliminated, and creditors cannot pursue you for repayment. It’s essential to know your discharge date for bankruptcy, as this event significantly impacts your financial future and allows you to begin rebuilding your credit.

Yes, you need to declare discharged bankruptcy in legal and financial situations. This declaration informs creditors that your obligations have been erased, protecting you from future claims related to those debts. Moreover, understanding your discharge date for bankruptcy is vital for your financial planning and rebuilding your credit.

The key difference lies in the outcome of each process. A discharge date for bankruptcy means your debts are eliminated under legal protection, while a dismissal ends your case without any relief from debt obligations. This distinction is important because a dismissal can impact your credit score and financial standing. To avoid confusion about these terms, consulting valuable resources like US Legal Forms can help you clarify your bankruptcy journey.