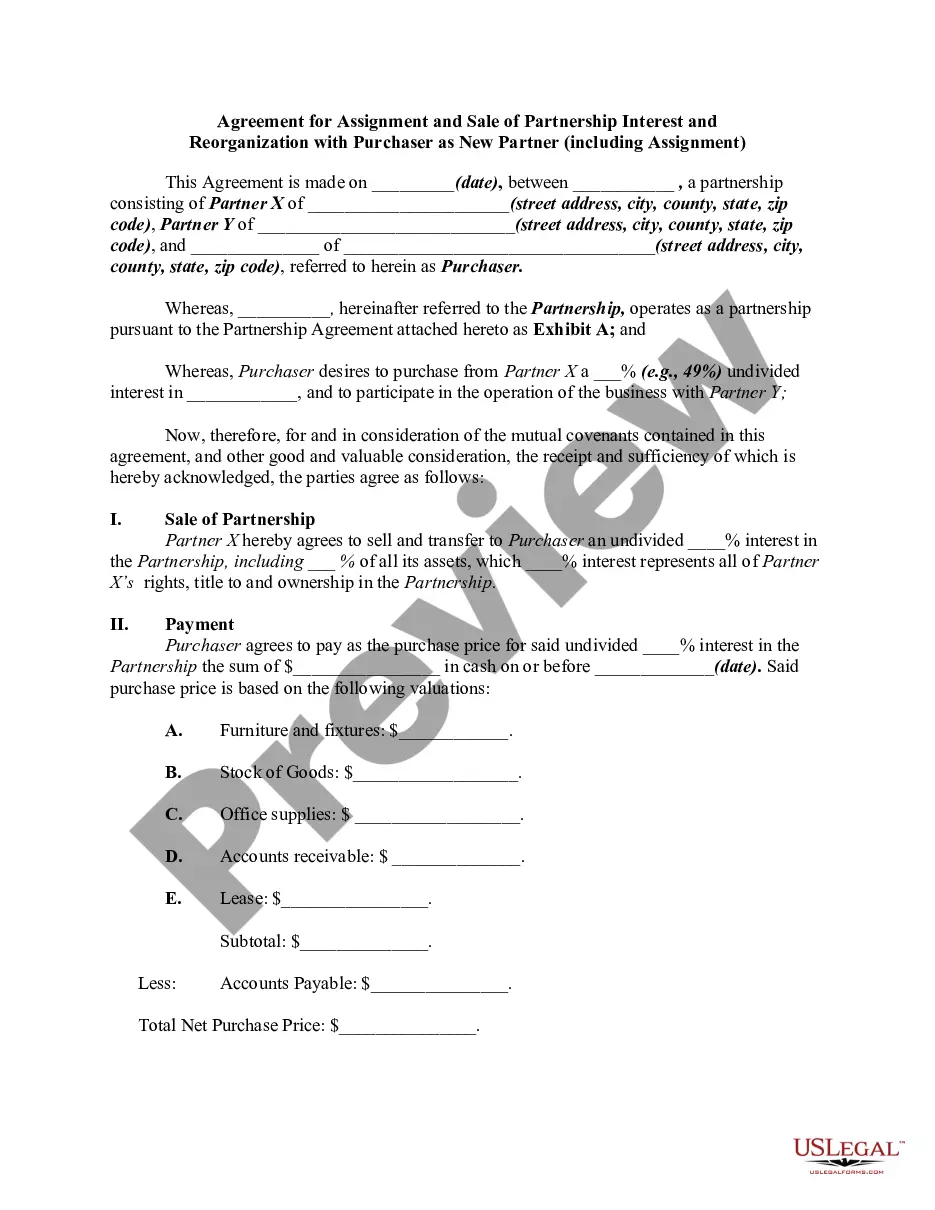

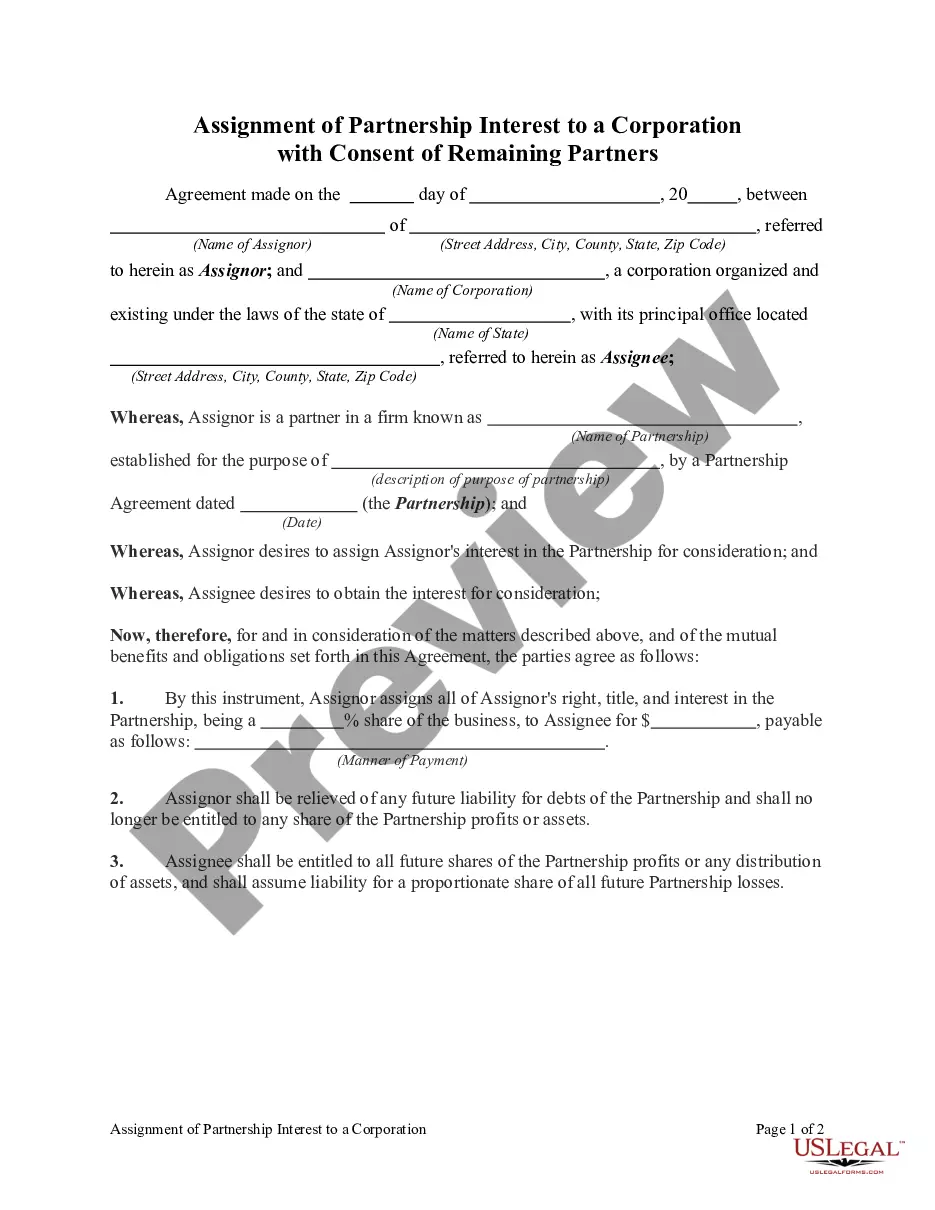

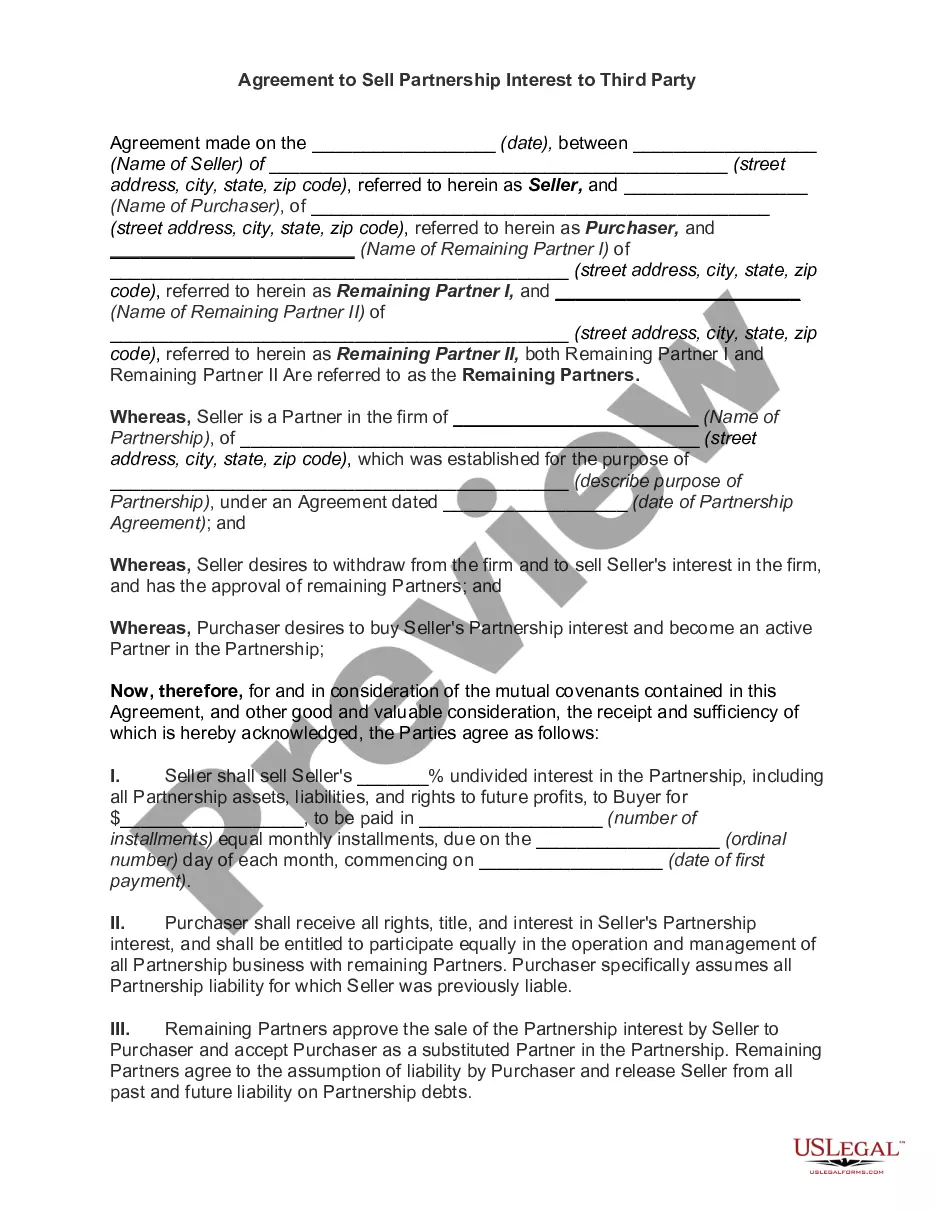

Partnership Interest Forfeiture

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Yes, a partnership can be transferred, but it often requires the consent of all partners involved. The transfer of partnership interest is not as straightforward as simply selling shares of stock, as it may lead to partnership interest forfeiture if not handled properly. It's crucial to refer to the partnership agreement for specific terms regarding transfers. For guidance through this process, consider using UsLegalForms, where you can find resources tailored to handle partnership agreements.

To report a transfer of partnership interest, you need to fill out IRS Form 1065 and attach K-1 forms for each partner involved. Include detailed information about the transfer, including the date, parties involved, and any changes in ownership percentages. Accurate reporting prevents potential partnership interest forfeiture and keeps your records in good standing.

Yes, gifting an interest in a partnership is possible under IRS rules, but you must follow specific legal procedures. Gifts of partnership interests may incur gift tax implications depending on the value of the interest. Make informed decisions to prevent issues that could result in partnership interest forfeiture.

You can transfer partnership interest, but the transfer typically requires consent from other partners depending on your partnership agreement. This transfer can happen through sale, gift, or inheritance. Ensure you complete all legal documentation to avoid complications that could lead to partnership interest forfeiture.

Abandoning a partnership interest requires notifying the other partners in writing of your intent to relinquish your stake. This act may lead to tax implications, as it can be seen as a sale at zero value. Consult with a tax advisor to understand any consequences, especially concerning partnership interest forfeiture.

Removing a partner from a partnership typically involves following the procedures outlined in your partnership agreement. Usually, this includes obtaining unanimous consent or offering the partner a buyout option. Failure to properly handle the removal could lead to disputes or potential partnership interest forfeiture.

Yes, you can exchange a partnership interest, often as a tax-deferred transaction under IRS Section 1031. This process allows partners to swap their interests without immediate tax consequences. However, be cautious, as improper exchanges may lead to partnership interest forfeiture, impacting your financial standing.

The loss on disposal of partnership interest refers to the financial impact a partner experiences when they sell or otherwise dispose of their ownership stake in a partnership. In situations involving partnership interest forfeiture, the partner may face a loss due to various factors such as market conditions or the value of the business at the time of disposal. Understanding this concept is crucial for partners as it impacts tax implications and overall financial planning. For partnership-related issues, consider using US Legal Forms to navigate the complexities of partnership interest forfeiture effectively.

To abandon an investment, you should formally communicate your decision to the relevant parties and ensure all necessary documents are properly completed. This process often includes understanding any financial implications or legal responsibilities tied to the investment. Knowing how to abandon an investment can help safeguard against unwanted partnership interest forfeiture.

When a partner withdraws their interest from the partnership, their ownership stake is typically reallocated among the remaining partners unless otherwise specified. This process might also involve settling any outstanding accounts and ensuring compliance with the partnership agreement. Understanding these procedures can prevent partnership interest forfeiture and facilitate a smooth transition.