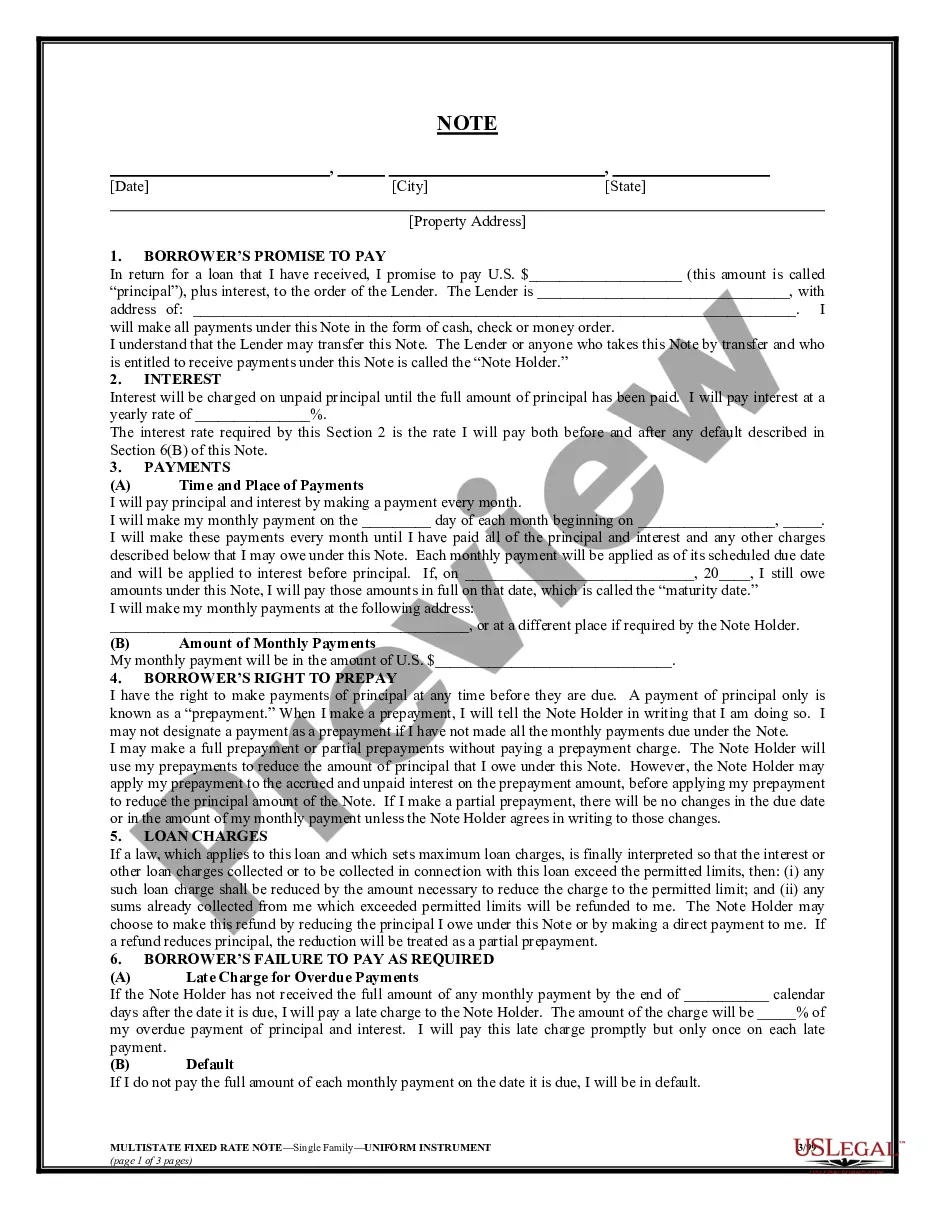

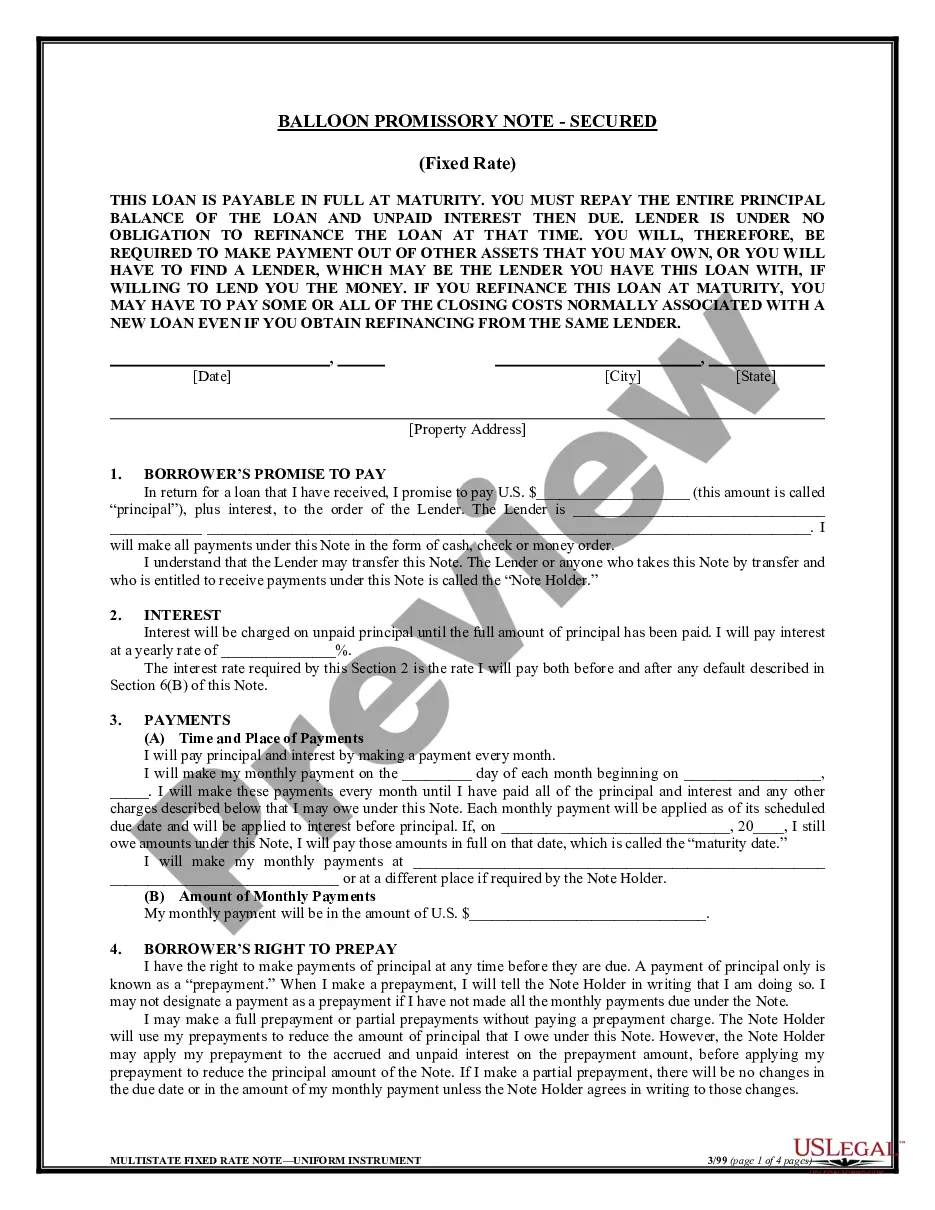

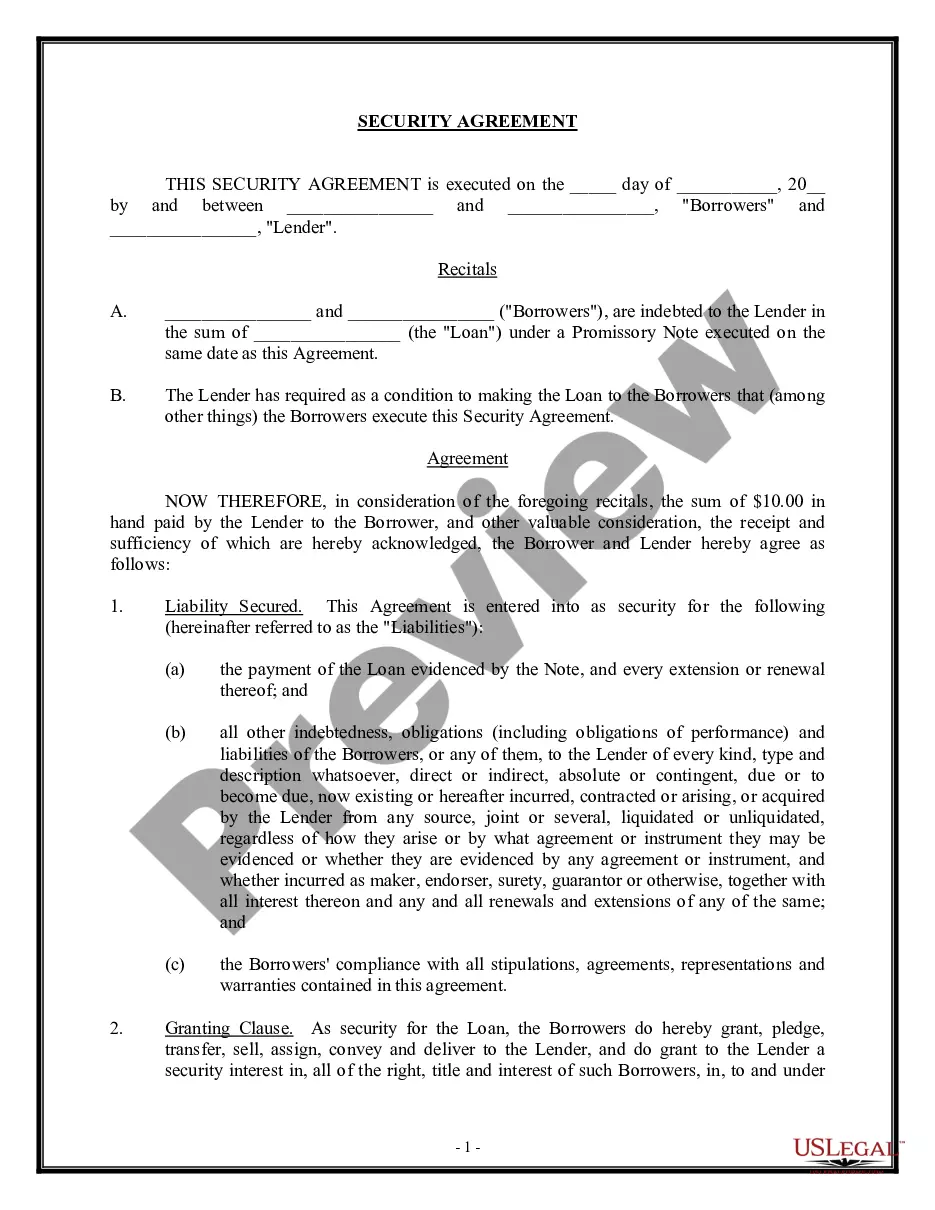

Secured Loan With House As Collateral

Description

How to fill out Secured Promissory Note?

The Secured Loan With House As Collateral you observe on this page is a reusable formal outline created by professional attorneys in compliance with federal and local regulations.

For over 25 years, US Legal Forms has supplied individuals, organizations, and lawyers with more than 85,000 authenticated, state-specific documents for any business and personal scenario. It’s the quickest, easiest, and most dependable method to acquire the paperwork you require, as the service ensures the utmost level of data safety and anti-malware defense.

Choose the format you prefer for your Secured Loan With House As Collateral (PDF, Word, RTF) and save the sample on your device.

- Search for the document you require and review it.

- Browse through the sample you looked for and preview it or examine the form description to verify it meets your needs. If it doesn’t, utilize the search bar to find the right one. Click Buy Now once you have located the template you require.

- Register and Log In.

- Select the pricing plan that fits you and create an account. Use PayPal or a credit card to make an immediate payment. If you already possess an account, Log In and check your subscription to continue.

- Acquire the editable template.

Form popularity

FAQ

To use your house as collateral to buy another house, you typically take out a secured loan with house as collateral against your current property. This can provide you with the necessary funds for a down payment on your new home. It’s vital to evaluate your financial situation, as taking on additional debt can affect your mortgage applications. Consulting with a financial advisor and using resources like uslegalforms can help you navigate the process effectively.

The $100,000 loophole for family loans allows you to lend or borrow up to $100,000 from family members without facing gift tax implications. This can be particularly useful when considering a secured loan with house as collateral for family members looking to help each other financially. However, it’s crucial to document the loan properly to avoid any misunderstandings. Utilizing platforms like uslegalforms can simplify the process of drafting loan agreements.

The amount you can borrow using your home as collateral depends on the equity you have built in your property. Lenders typically allow you to borrow up to 80% of your home’s appraised value, minus any existing mortgage balance. This means if your home is worth $300,000 and you owe $100,000, you could potentially access $160,000. A secured loan with house as collateral can provide substantial funding options for your financial needs.

Yes, you can use your house as collateral for a secured loan with house as collateral. This type of loan allows lenders to offer you better interest rates since they have a guarantee. By putting your home on the line, you can access funds for various purposes, such as home improvement or debt consolidation. It's essential to understand the risks involved, as failing to repay the loan can lead to losing your home.

Your house (or other real estate) is a popular choice for collateral. The higher your home's value, the more likely lenders will offer lower interest rates. Lenders look at your home equity when assessing it, so if you've paid off your mortgage, it puts you in a good position to borrow a significant amount.

If you have owned your home for some time, or the market has allowed you to build equity, this can be a good option for collateral. You can also use a house you own outright as collateral on a second home or investment property. Or you can use an investment property as collateral for a primary residence.

As the name implies, home equity loans also use your house as collateral. These loans leverage the equity you've built over time. For instance, say you have $200,000 of your mortgage remaining on your home valued at $300,000. You can borrow about 80% ($80,000) against your equity and secure the debt with your house.

Collateral refers to an asset that a borrower offers as a guarantee for a loan or debt. For a mortgage (or a deed of trust, exclusively used in some states), the collateral is almost always the property you're buying with the loan. Obtaining the financing puts a lien on the property.

You can also use a house you own outright as collateral on a second home or investment property. Or you can use an investment property as collateral for a primary residence. Banks will look at real estate collateral favorably as property generally holds its value and would allow them to make back losses more readily.