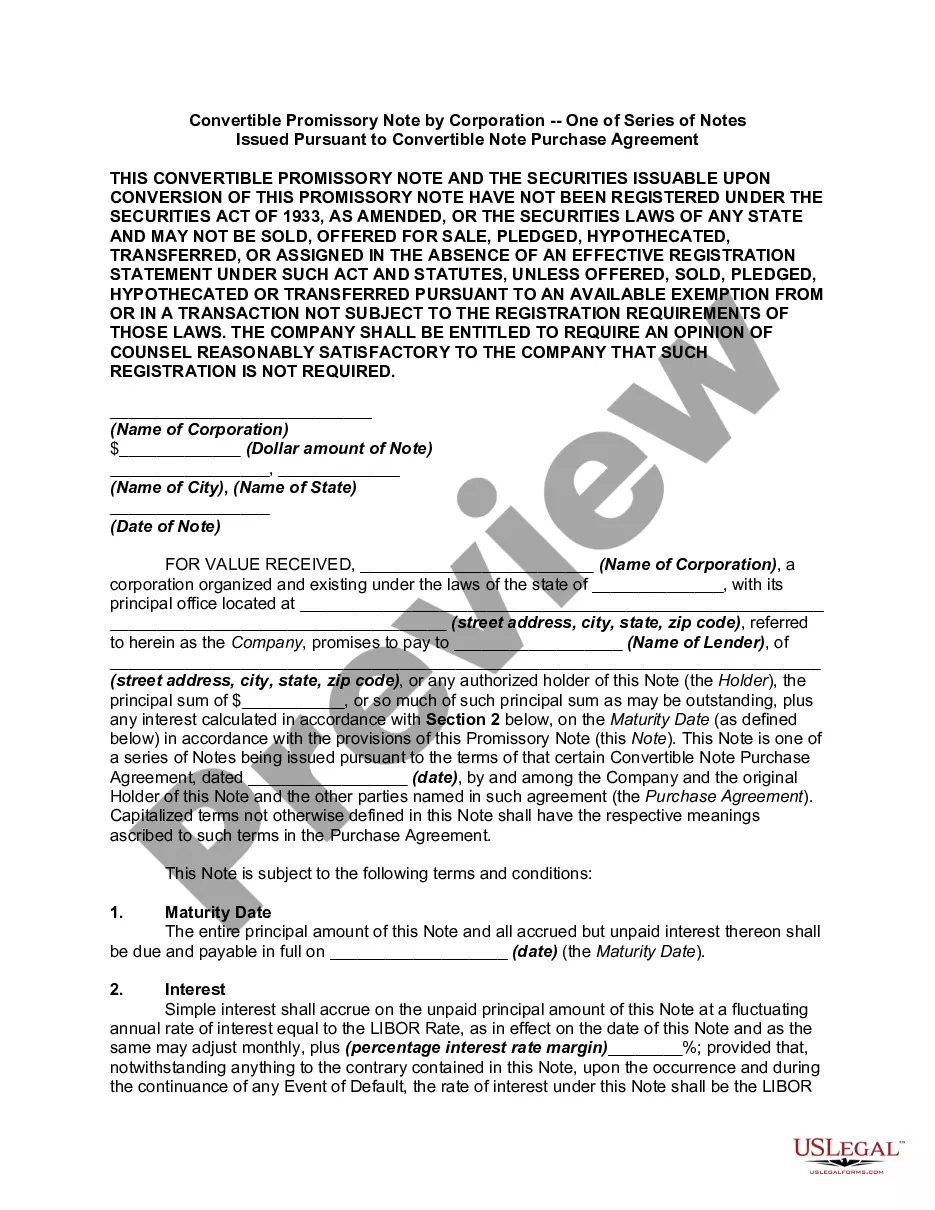

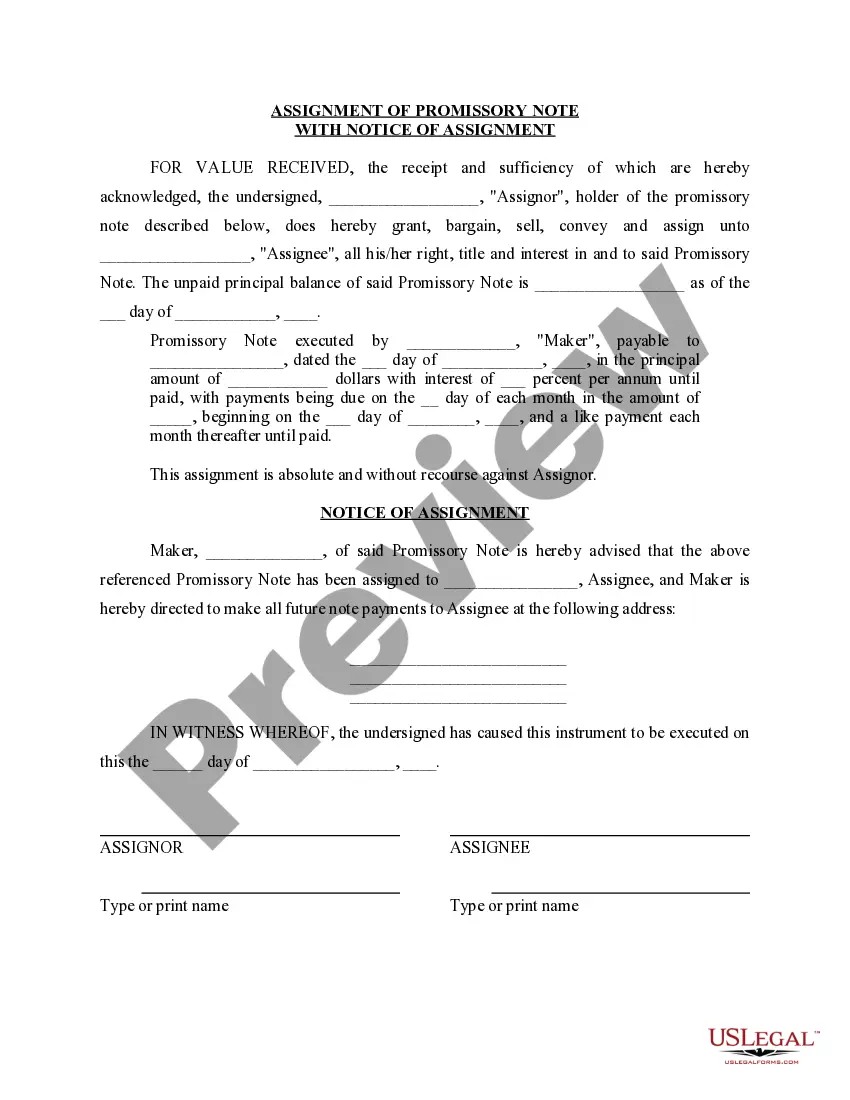

Promissory Note Secured By Real Property

Description

How to fill out Multistate Promissory Note - Secured?

Whether for business purposes or for individual matters, everyone has to manage legal situations at some point in their life. Filling out legal papers requires careful attention, beginning from selecting the proper form template. For instance, if you select a wrong edition of a Promissory Note Secured By Real Property, it will be turned down when you submit it. It is therefore important to have a reliable source of legal files like US Legal Forms.

If you need to obtain a Promissory Note Secured By Real Property template, follow these easy steps:

- Get the template you need using the search field or catalog navigation.

- Examine the form’s information to ensure it fits your situation, state, and county.

- Click on the form’s preview to examine it.

- If it is the incorrect document, get back to the search function to find the Promissory Note Secured By Real Property sample you need.

- Download the file if it meets your needs.

- If you have a US Legal Forms account, click Log in to access previously saved files in My Forms.

- In the event you don’t have an account yet, you may obtain the form by clicking Buy now.

- Pick the appropriate pricing option.

- Finish the account registration form.

- Select your payment method: you can use a credit card or PayPal account.

- Pick the file format you want and download the Promissory Note Secured By Real Property.

- When it is downloaded, you are able to fill out the form by using editing applications or print it and finish it manually.

With a substantial US Legal Forms catalog at hand, you never have to spend time searching for the appropriate template across the web. Take advantage of the library’s straightforward navigation to find the right template for any occasion.

Form popularity

FAQ

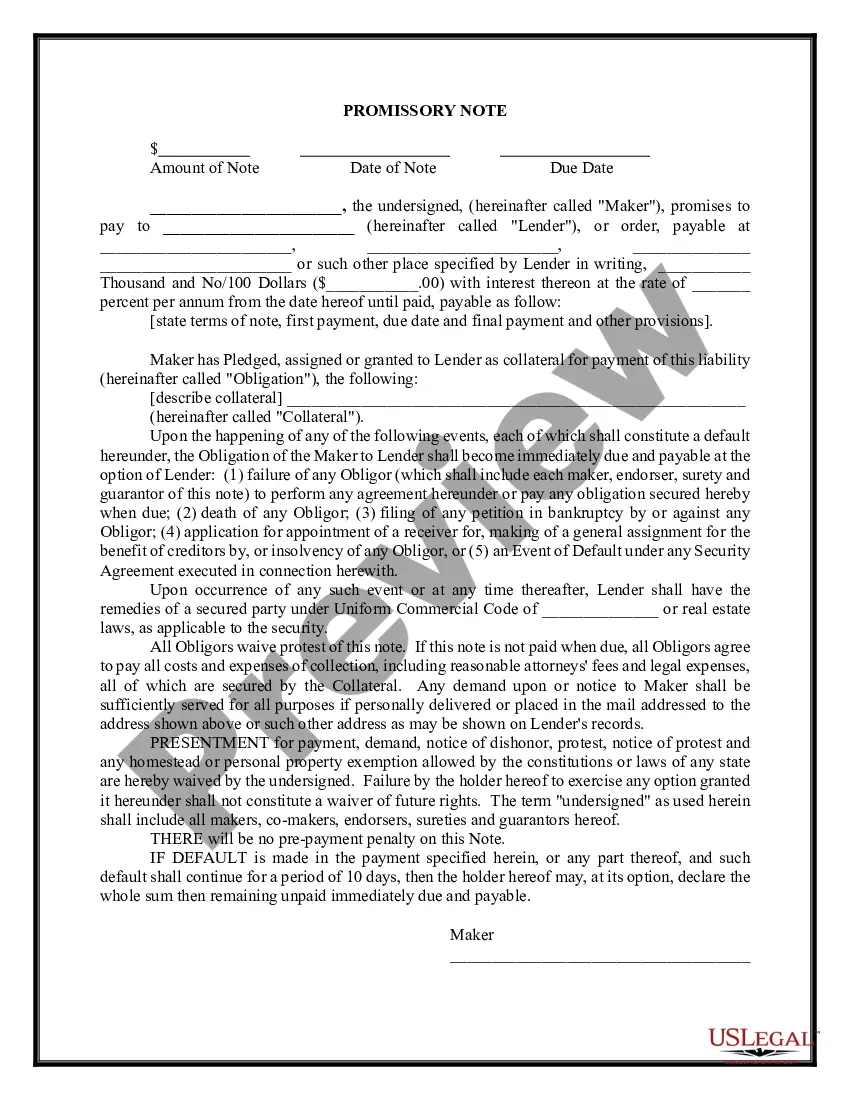

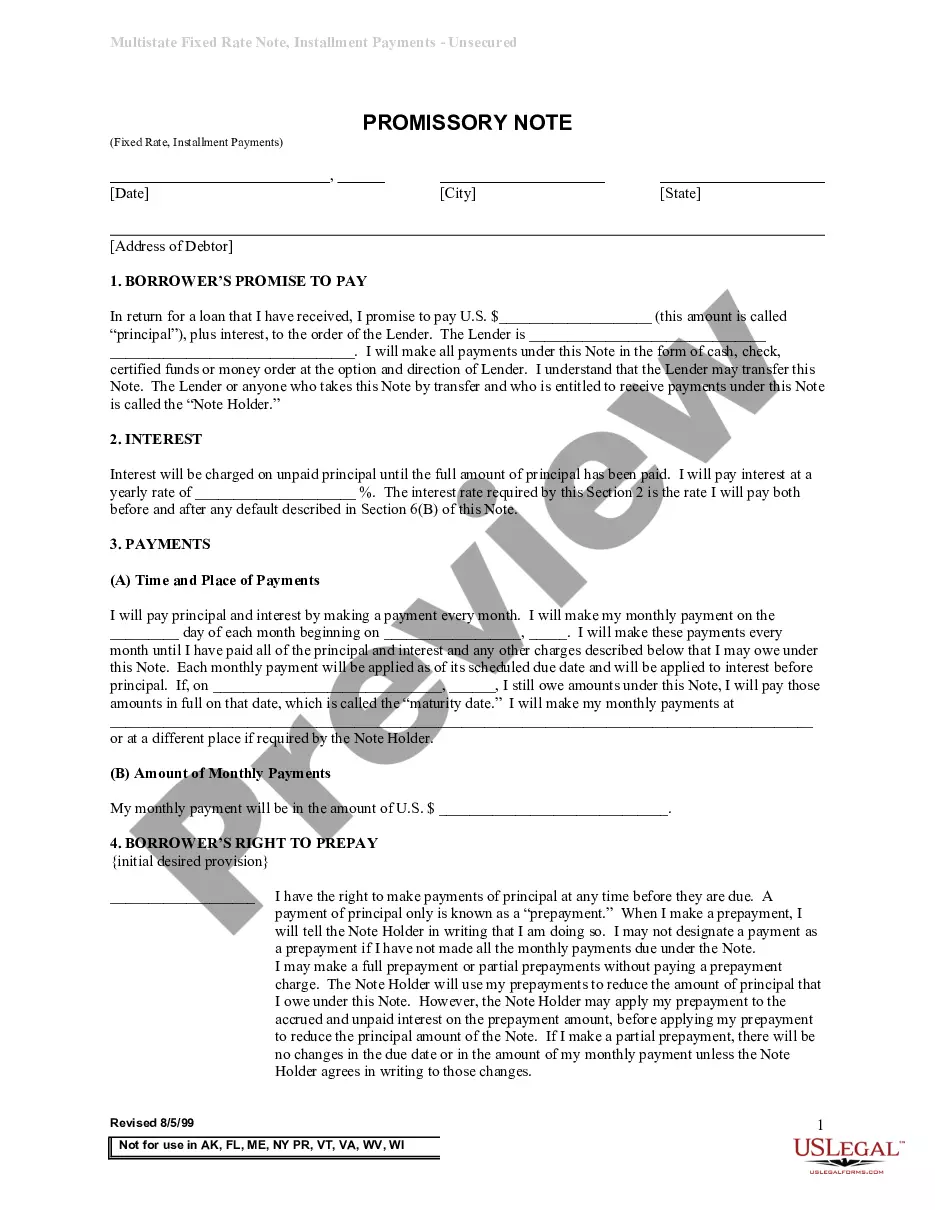

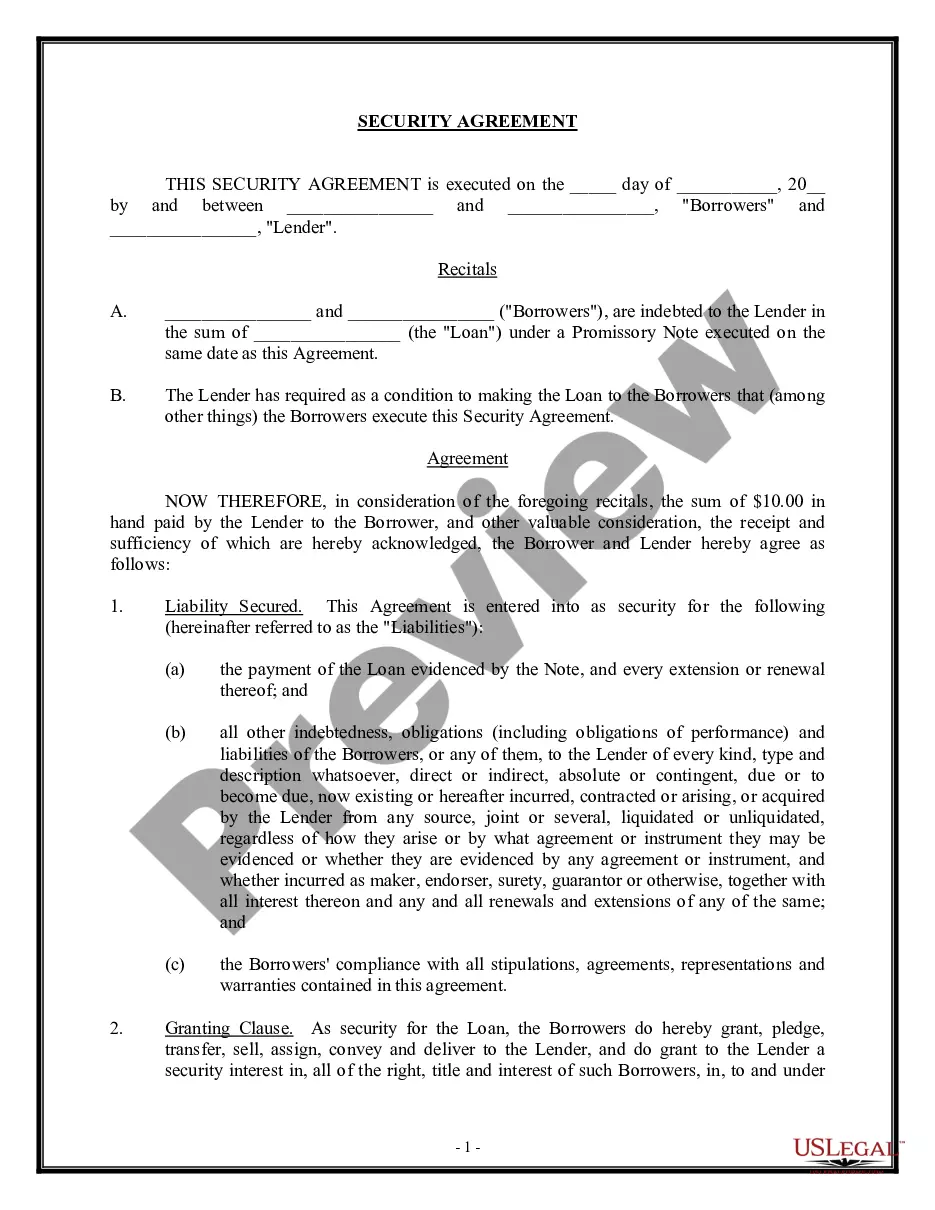

Borrower's promise to pay is secured by a mortgage, deed of trust or similar security instrument that is dated the same date as this Note and called the ?Security Instrument.? The Security Instrument protects the Lender from losses, which might result if Borrower defaults under this Note.

Secured promissory notes By assuring that the property attached to the note is of sufficient value to cover the amount of the loan, the payee thus has a guarantee of being repaid. The property that secures a note is called collateral, which can be either real estate or personal property.

A secured note is guaranteed by an interest in an asset that is worth at least the amount of the note. If you have a mortgage or an automobile loan, you are the borrower in a secured note. In the case of a mortgage, you hold a secured note with your home pledged as collateral.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner didn't make their loan payments. Your lender will keep the original promissory note until your loan is paid off.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner didn't make their loan payments. Your lender will keep the original promissory note until your loan is paid off.