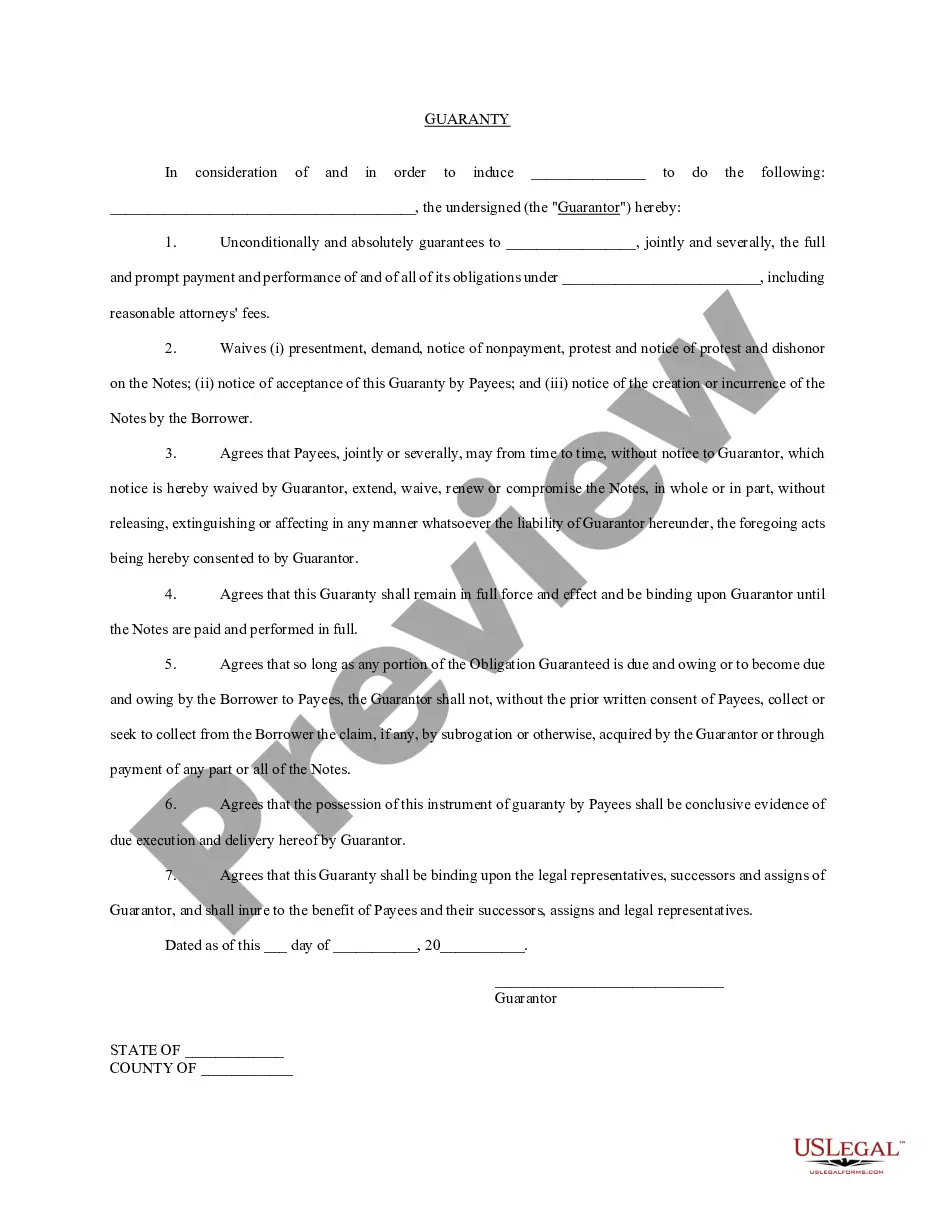

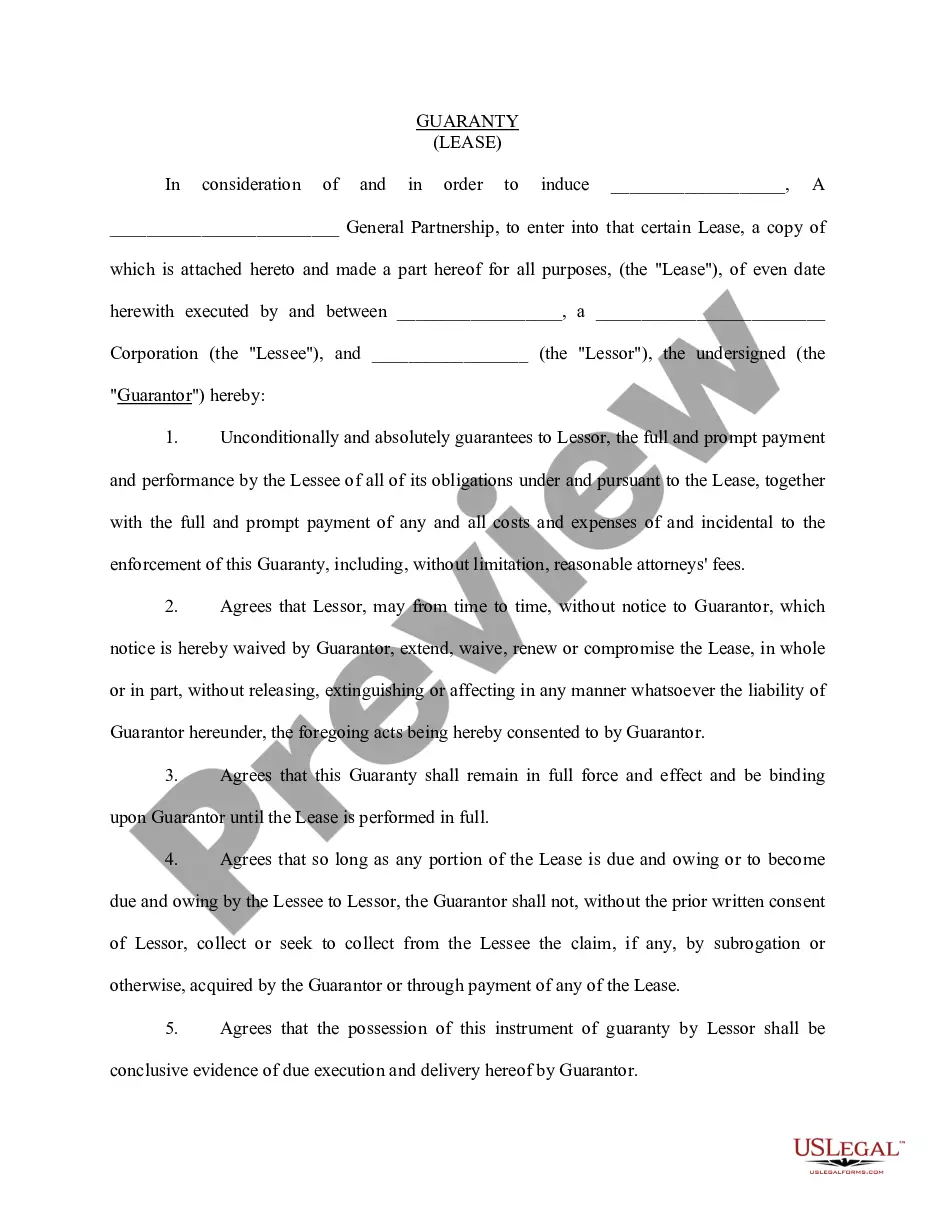

Promissory Individual Borrower With 100

Description

How to fill out Guaranty Of Promissory Note By Corporation - Individual Borrower?

The Promissory Individual Borrower With 100 displayed on this page is a versatile official template crafted by experienced attorneys in accordance with federal and local regulations.

For over 25 years, US Legal Forms has supplied individuals, enterprises, and legal practitioners with more than 85,000 authenticated, state-specific documents for any commercial and personal circumstances. It’s the fastest, easiest, and most dependable method to acquire the forms you require, as the service ensures the utmost level of data protection and anti-malware security.

Subscribe to US Legal Forms to have authenticated legal templates for all of life’s scenarios readily available.

- Search for the document you require and examine it. Browse through the file you looked for and preview it or review the form details to confirm it meets your needs. If it doesn’t, use the search feature to find the correct one. Click Buy Now once you have found the template you require.

- Create an account and Log In. Choose the pricing option that fits your needs and establish an account. Use PayPal or a credit card to make a swift payment. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the fillable template. Select the format you prefer for your Promissory Individual Borrower With 100 (PDF, DOCX, RTF) and download the sample onto your device.

- Fill out and sign the document. Print the template to complete it by hand. Alternatively, utilize an online multifunctional PDF editor to efficiently and accurately fill out and sign your form with a valid signature.

- Download your documents again. Use the same document again whenever necessary. Access the My documents section in your profile to redownload any previously acquired forms.

Form popularity

FAQ

Yes, 100 mortgages are still available, though they may come with specific qualifications. As a promissory individual borrower with 100, you should check with financial institutions that specialize in mortgage lending. They can provide insights into current offers and terms. Utilizing resources from US Legal Forms can help you better understand mortgage options available to you.

While it is possible to borrow against your home equity, most lenders typically allow borrowing up to 80-90% of your equity. As a promissory individual borrower with 100, it is essential to assess your financial situation and ensure you can manage the repayments. Consider consulting a financial advisor to explore the best options for leveraging your home equity. Platforms like US Legal Forms can provide you with the documentation needed for such borrowing.

The maximum amount on a promissory note can vary based on the lender's policies and the borrower's creditworthiness. For a promissory individual borrower with 100, the limit is often determined by personal circumstances. It is crucial to understand the terms and conditions of the note, ensuring it meets your financial needs. Utilizing platforms like US Legal Forms can help you draft a compliant and effective promissory note.

When dealing with a personal promissory note, notarization is not strictly required. However, having the document notarized can add an extra layer of security and legality, especially for a promissory individual borrower with 100. Notarization helps verify the identities of the parties involved and ensures that they are signing the document voluntarily. For those looking to create a robust legal document, US Legal Forms provides templates and guidance to ensure your promissory note meets all necessary standards.

A promissory note does not always need to be notarized to be considered legal, but notarization can add an extra layer of protection. This process verifies the identities of the signers, making it more difficult to dispute the agreement later. If you are a promissory individual borrower with 100, it is wise to consider notarization for added security. To ensure compliance with your state’s requirements, consult resources like US Legal Forms.

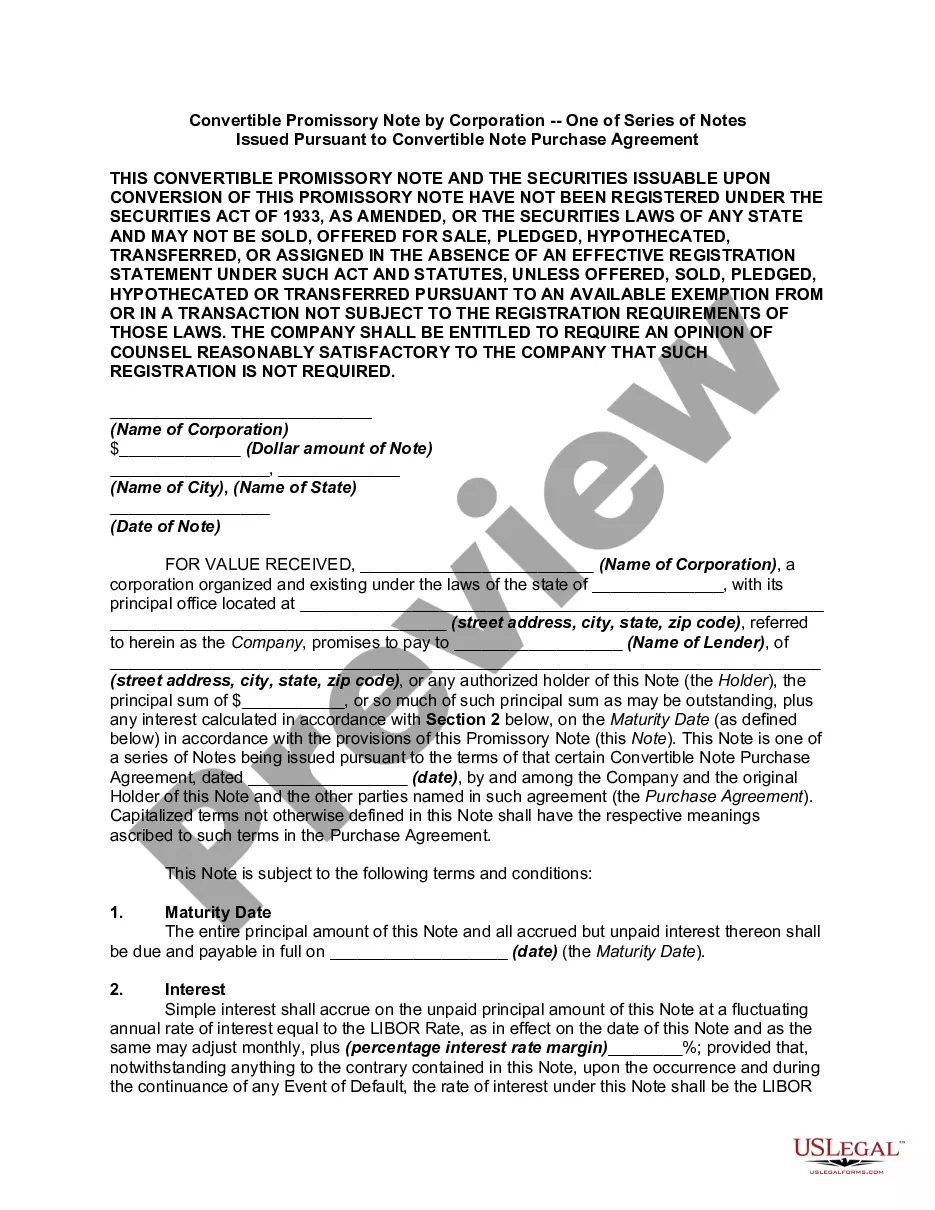

Although potentially issued by financial institutions, other organizations or individuals can use promissory notes to confirm the agreed terms of a loan.

Promissory Notes Are Useful Legal Tools Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

The process takes approximately 30 minutes to complete. To sign the MPN: Open "Master Promissory Note (MPN)" at studentaid.gov. Select the type of Direct Loan MPN that corresponds to your loan and log in with your FSA ID. Progress through the entire MPN process until you complete all sections.

A promissory note is a written agreement between one party (you, the borrower) to pay back the loan issued by another party (often a bank or other financial institution). Anyone lending money (like home sellers, credit unions, mortgage lenders and banks, for instance) can issue a promissory note.