Promissory Individual Borrower For Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Guaranty Of Promissory Note By Corporation - Individual Borrower?

The Promissory Individual Borrower For Mortgage displayed on this page is a reusable formal template crafted by professional attorneys in accordance with federal and state laws.

For over 25 years, US Legal Forms has supplied individuals, businesses, and lawyers with more than 85,000 confirmed, state-specific forms for any business or personal occasion. It’s the quickest, easiest, and most reliable method to acquire the documents you require, as the service ensures bank-level data security and anti-malware safeguards.

Fill out and sign the documents. Print the template to complete it manually. Alternatively, use an online multifunctional PDF editor to quickly and accurately fill out and sign your form with a valid signature. Download your documents one more time. Use the same document again whenever necessary. Open the My documents tab in your profile to redownload any previously obtained forms. Subscribe to US Legal Forms to have verified legal templates for all of life’s situations at your fingertips.

- Browse for the document you require and review it.

- Examine the file you searched and preview it or read the form description to confirm it meets your needs. If it doesn't, use the search feature to find the correct one. Click Buy Now once you have found the template you need.

- Select and Log In.

- Choose the pricing plan that best fits you and sign up for an account. Utilize PayPal or a credit card to make a quick payment. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the fillable template.

- Select the format you prefer for your Promissory Individual Borrower For Mortgage (PDF, Word, RTF) and download the sample to your device.

Form popularity

FAQ

Yes, an individual can give someone a mortgage. This process involves the individual acting as a lender to the promissory individual borrower for mortgage. It is crucial to document this agreement properly to protect both parties' interests. Using platforms like uslegalforms can simplify the creation of the necessary documents, ensuring compliance with legal requirements.

Yes, a private individual can provide a mortgage to a promissory individual borrower for mortgage. This arrangement is often referred to as a private mortgage, and it can be a viable option for those who may not qualify for traditional financing. However, it is important to draft a clear and legally binding agreement to protect both parties involved. Using platforms like US Legal Forms can help you create the necessary documents to ensure a smooth transaction.

Banks are not obligated to accept a promissory note from a promissory individual borrower for mortgage. Each financial institution has its own policies regarding the acceptance of such notes. Factors that influence acceptance include the borrower's creditworthiness, the note's terms, and the bank's lending criteria. It is essential to consult with your bank to understand their specific requirements.

When you sign a promissory note as a promissory individual borrower for mortgage, you commit to repaying the borrowed amount. If you default on this obligation, you may face serious financial consequences, including damage to your credit score and potential legal action. Additionally, lenders may pursue the collateral you provided, which can lead to loss of property. It is crucial to fully understand the terms and implications before signing.

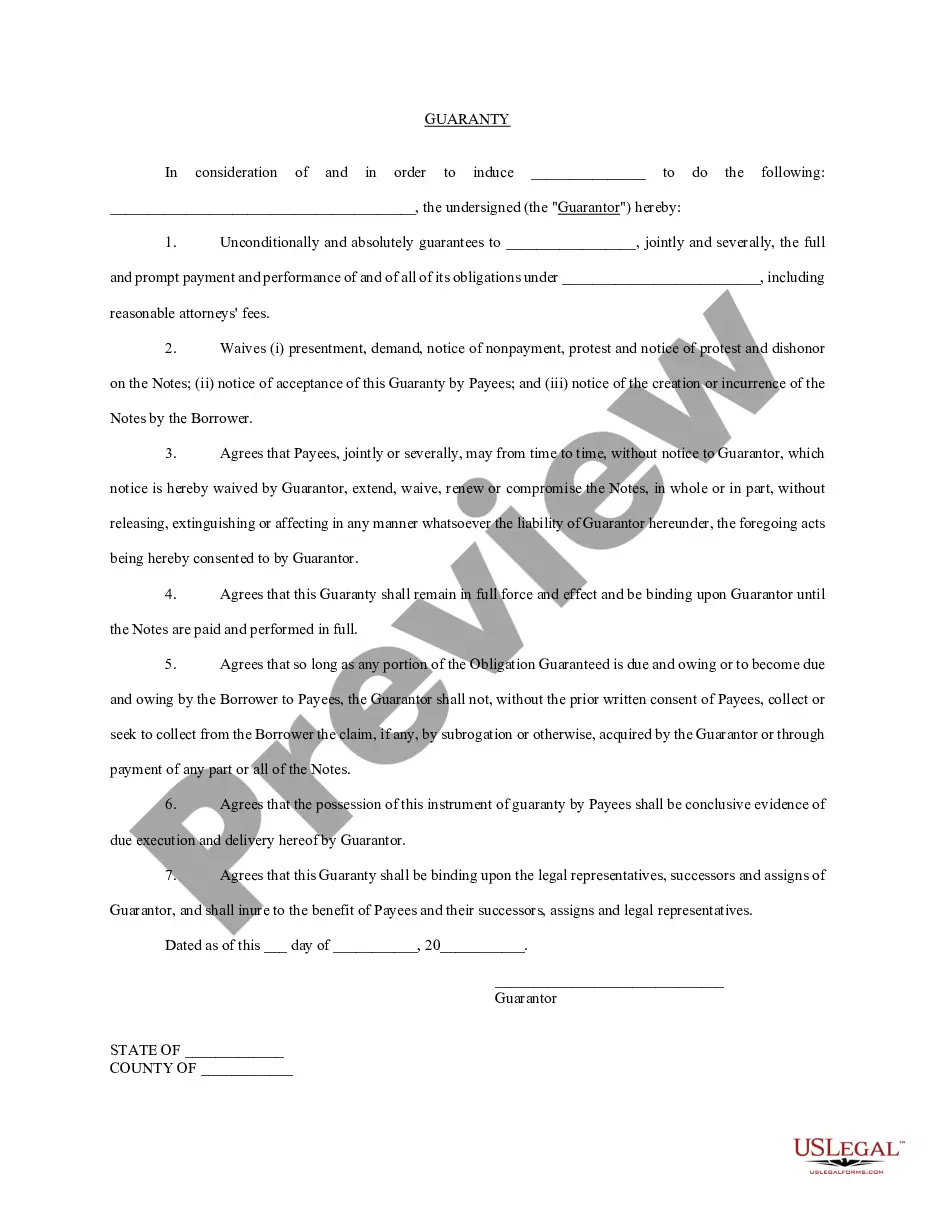

Typically, there are two parties to a promissory note: The promisor, also called the note's maker or issuer, promises to repay the amount borrowed. The promisee or payee is the person who gave the loan.

The promissory note is issued by the lender and is signed by the borrower (but not the lender). It is considered a contract, and signing it legally obligates the borrower to pay back the amount borrowed, plus any interest, as defined in the promissory note.

The promissory note creates the loan obligation. The promissory note is a contract separate from the mortgage that's basically an IOU. Signing a promissory note means you're liable for repaying the loan. It contains the terms for repayment.

In a promissory note, the person who makes the promise to pay is called as Promisor.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.