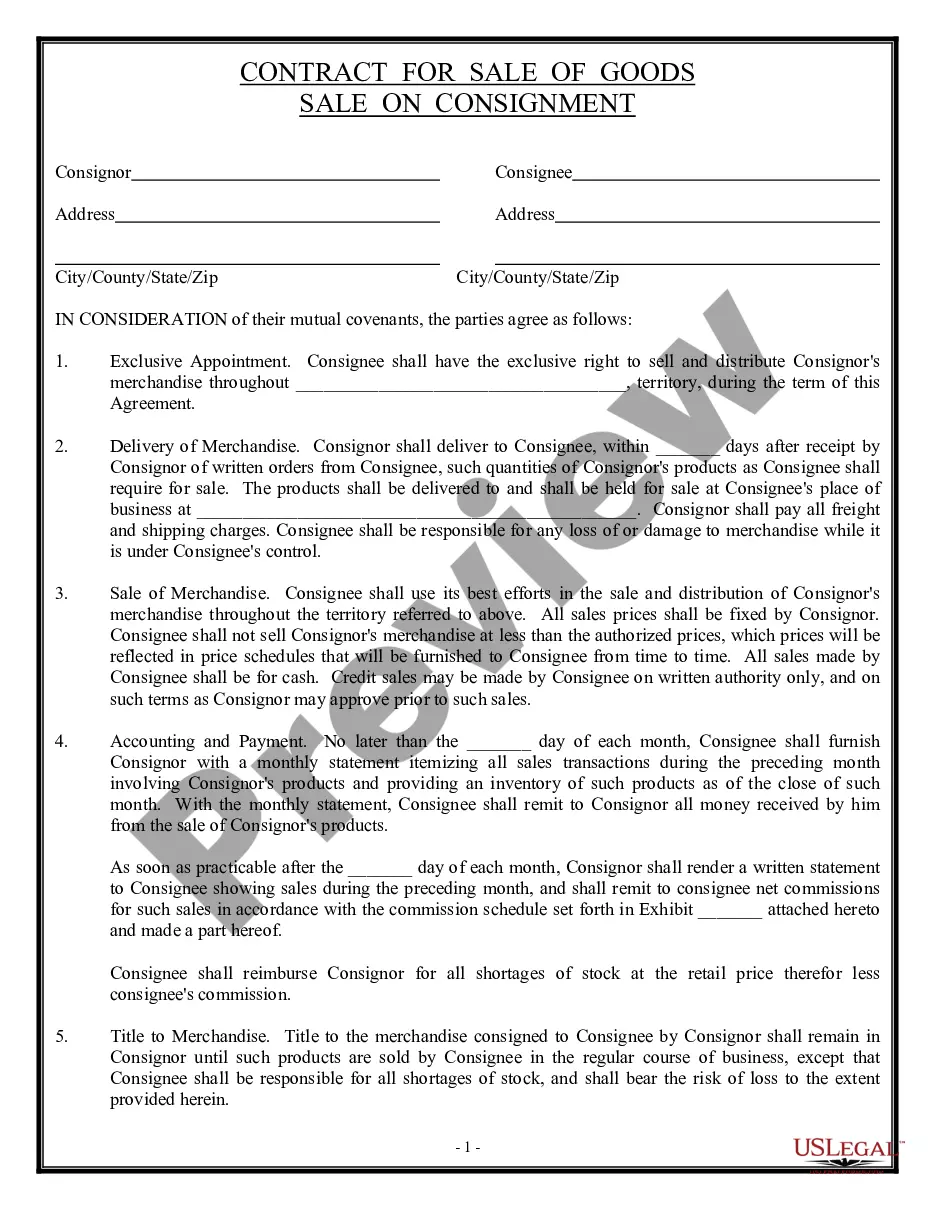

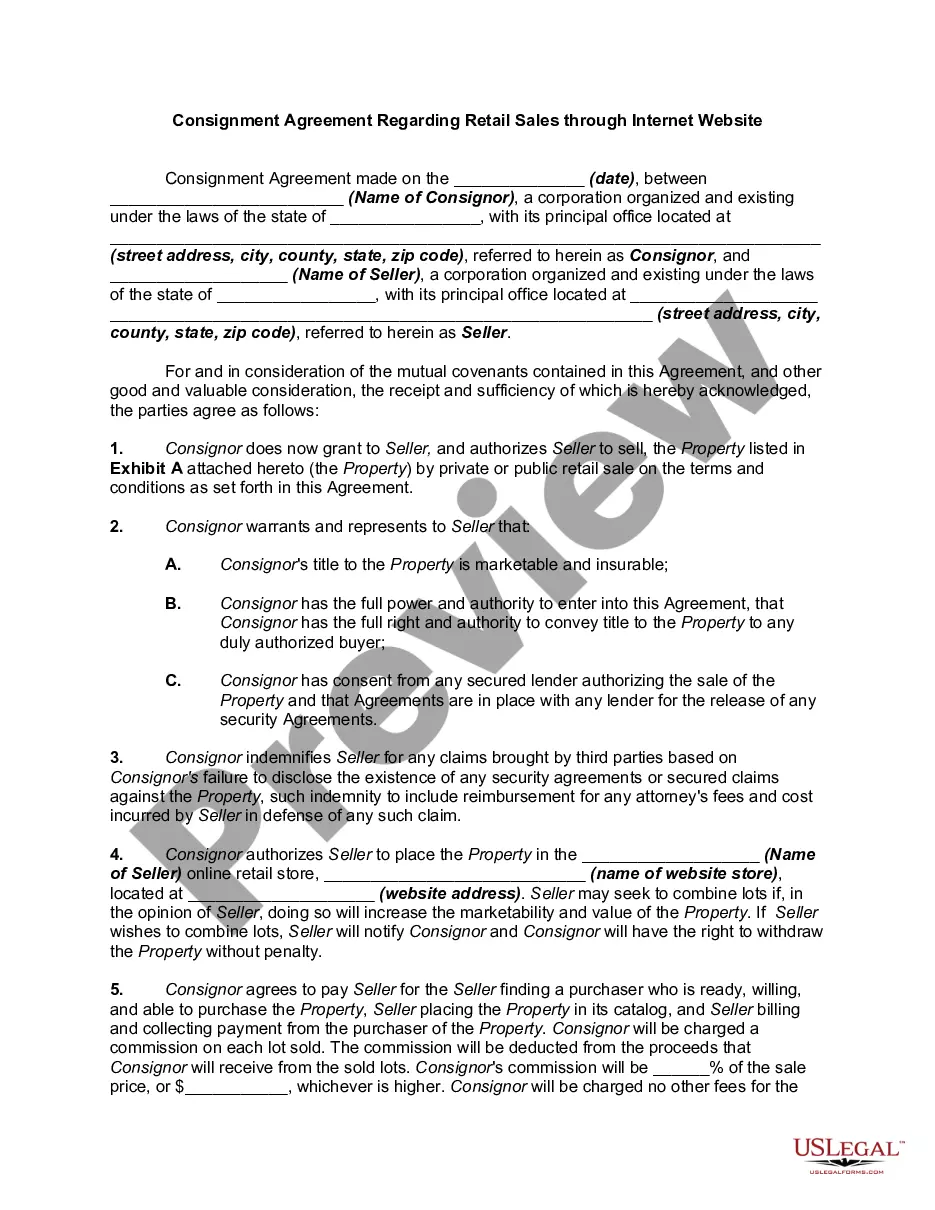

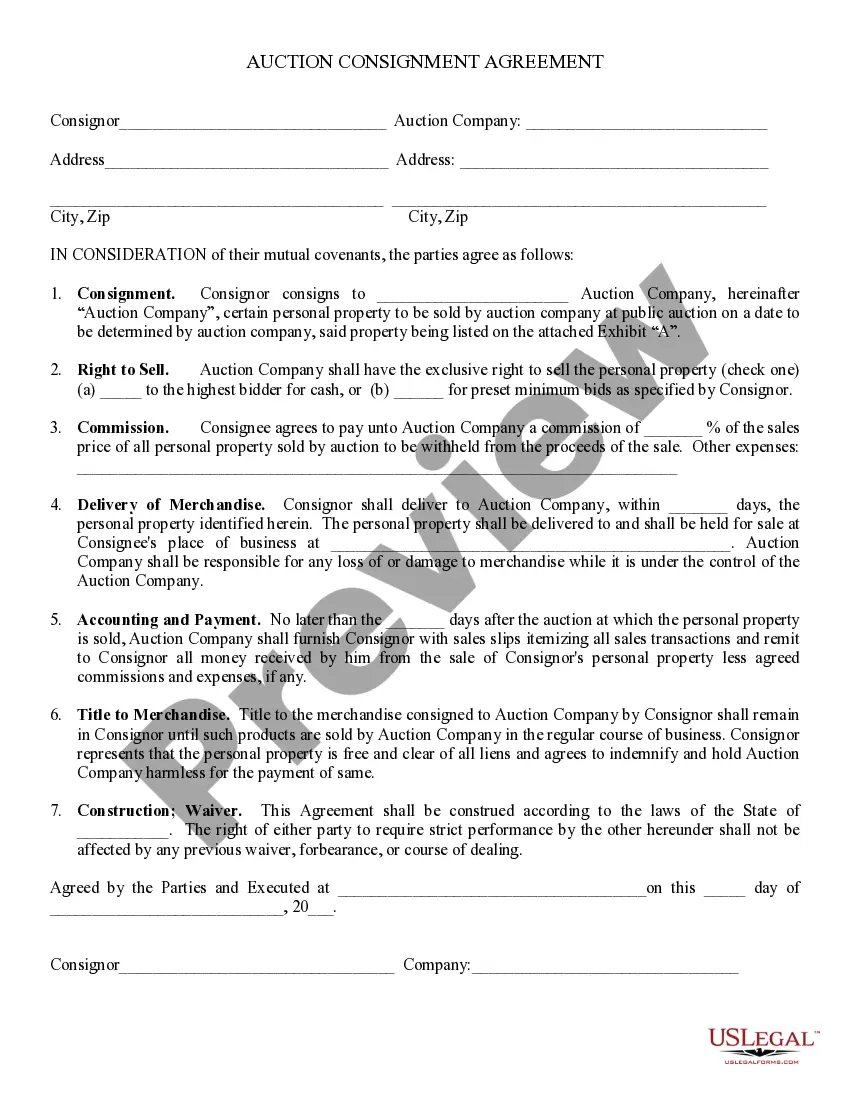

Consignment Form Template For Food In Tarrant

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Business personal property accounts for 9.8 percent of the total market value of all property in the state, and 10.5 percent of all school taxable property in the state. exemption if they are in the state on a temporary basis.

All real and tangible personal property in Texas is taxable in proportion to its appraised value unless the Texas Constitution authorizes an exemption. Texas law provides a variety of property tax exemptions for qualifying property owners.

Personal property tax in Texas is imposed on income producing tangible personal property. The local county appraisal district uses the Texas personal property tax to fund county services. All income producing tangible personal property is taxable for county appraisal district purposes.

Per Section 22.01(a) of the Texas Property Tax Code, taxable personal property includes assets used for the production of income, such as inventories, machinery, equipment, vehicles, furniture and supplies used in the business.

Texas's property tax also applies to tangible personal property (furniture, machinery, supplies, inventories, etc.)

Texas sales and use tax exempts tangible personal property that becomes an ingredient or component of an item manufactured for sale, as well as taxable services performed on a manufactured product to make it more marketable.