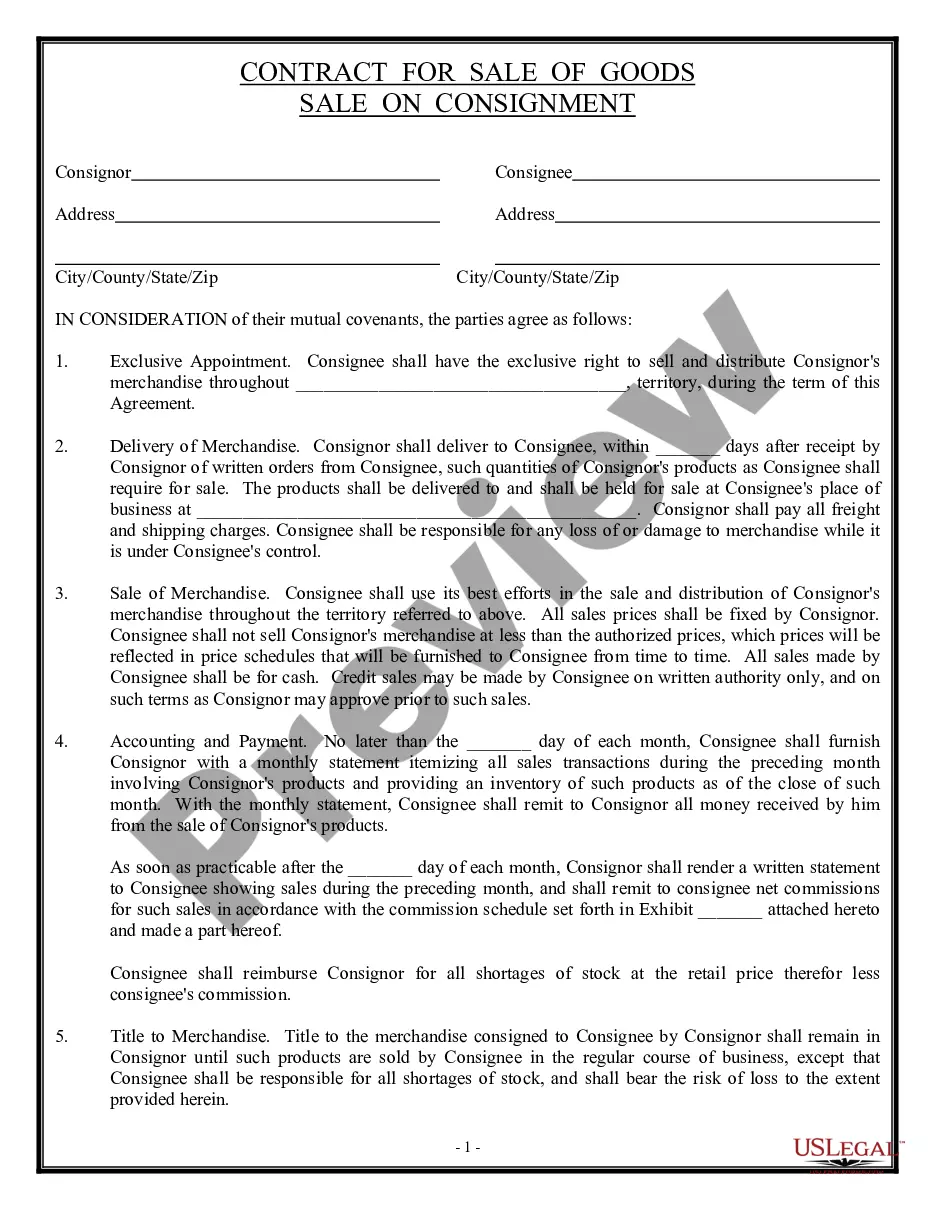

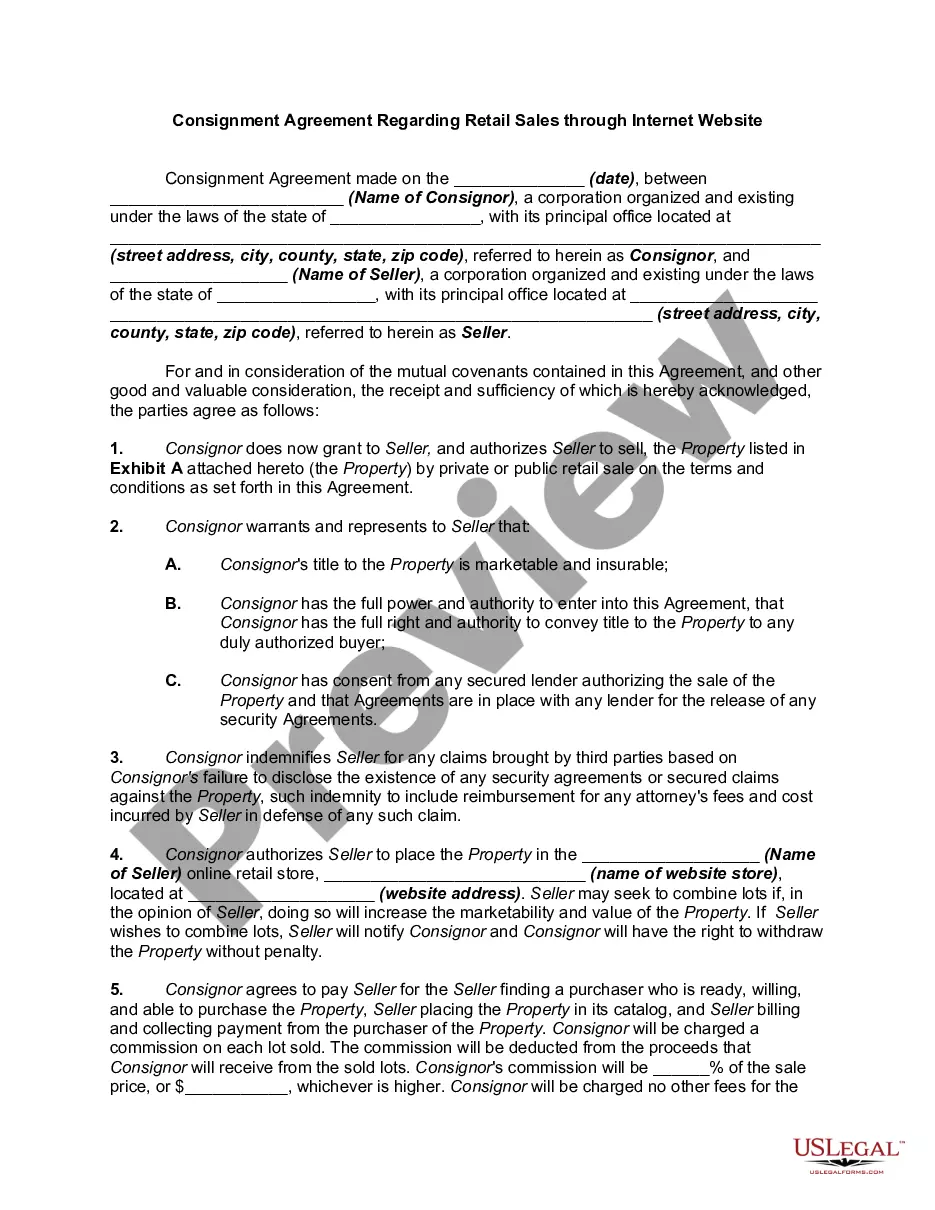

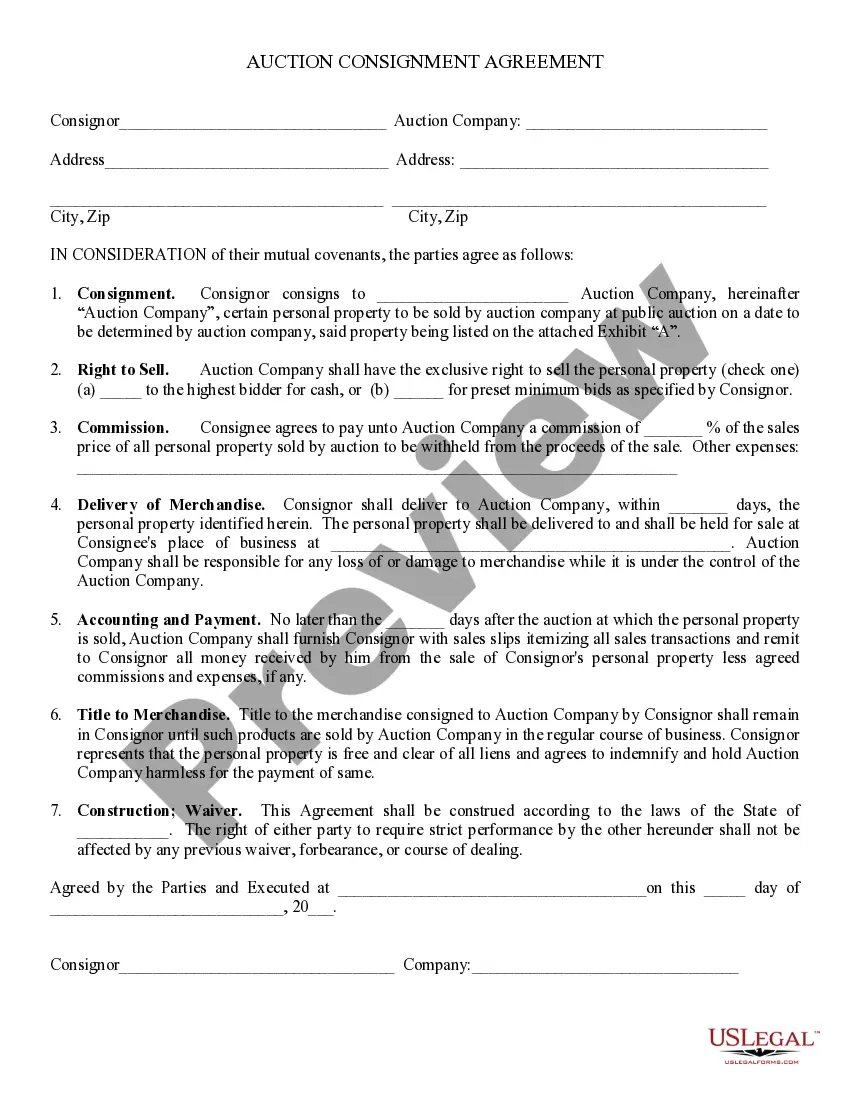

Consignment Account Example In Kings

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Now that you know what consignment is, here's how to calculate consignment inventory. Step 1: Establish a Listing of Your Inventory of Consignment Products. Step 2: Subtract the Seller's or Shipper's Portion of the Consignment Product Sold. Step 3: Update the Inventory After the Sale.

The journal entry accounts for the sales and expenses of the consignment inventory. No entry is made by the consignee. It's important to note that the import duty of 200 is debited to the consignment inventory account.

Consignment stock refers to inventory that a vendor sends to a retailer for sale. The retailer takes responsibility for selling the goods and when they do, the retailer pays the vendor for the inventory.

The one who delegates their products to be sold by the retailer is the consignor. The person who is entrusted with the responsibility of selling the products is the consignee and the products do not belong to them. The merchandise belongs to the consignor until it is sold.

A “Consignment Note”, also referred to as a loading list, is a critical document in freight forwarding and logistics. This document is issued by the consignor and contains all essential details of the goods being shipped to the consignee. It serves as proof of receipt when signed by the inland carrier.

The consignor prepares the consignment Account, the Goods Sent on Consignment Account and the Consignee's Account in his books, whereas the consignee prepares the Consignor's Account and the Commission Account in his books.

Ownership of the inventory is only transferred to the consignee upon sale to the end customer. At this time, the consignee recognizes revenue, and the consignor records the sale on the consignor's financial statements.

Consignment accounting is a type of business arrangement in which one person send goods to another person for sale on his behalf and the person who sends goods is called consignor and another person who receives the goods is called consignee, where consignee sells the goods on behalf of consignor on consideration of ...

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)