Consignment Contract Sample With Revenue Sharing In Harris

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

When goods sent on consignment are sold by the consignee, the account to be debited is in the books of consignor.

The consignor will make a journal entry for the goods received. The journal entry for the consignment accounting will have a credit and a debit. It is recorded as a debit for the consignment inventory, and a credit for the store's inventory. The consignee does not make an entry.

A consignment stock arrangement is one where a seller of goods (the consignor) consigns a stock of goods to a buyer (the consignee) and in doing so retains ownership of those goods pending the moment when they are taken/appropriated for use by the buyer.

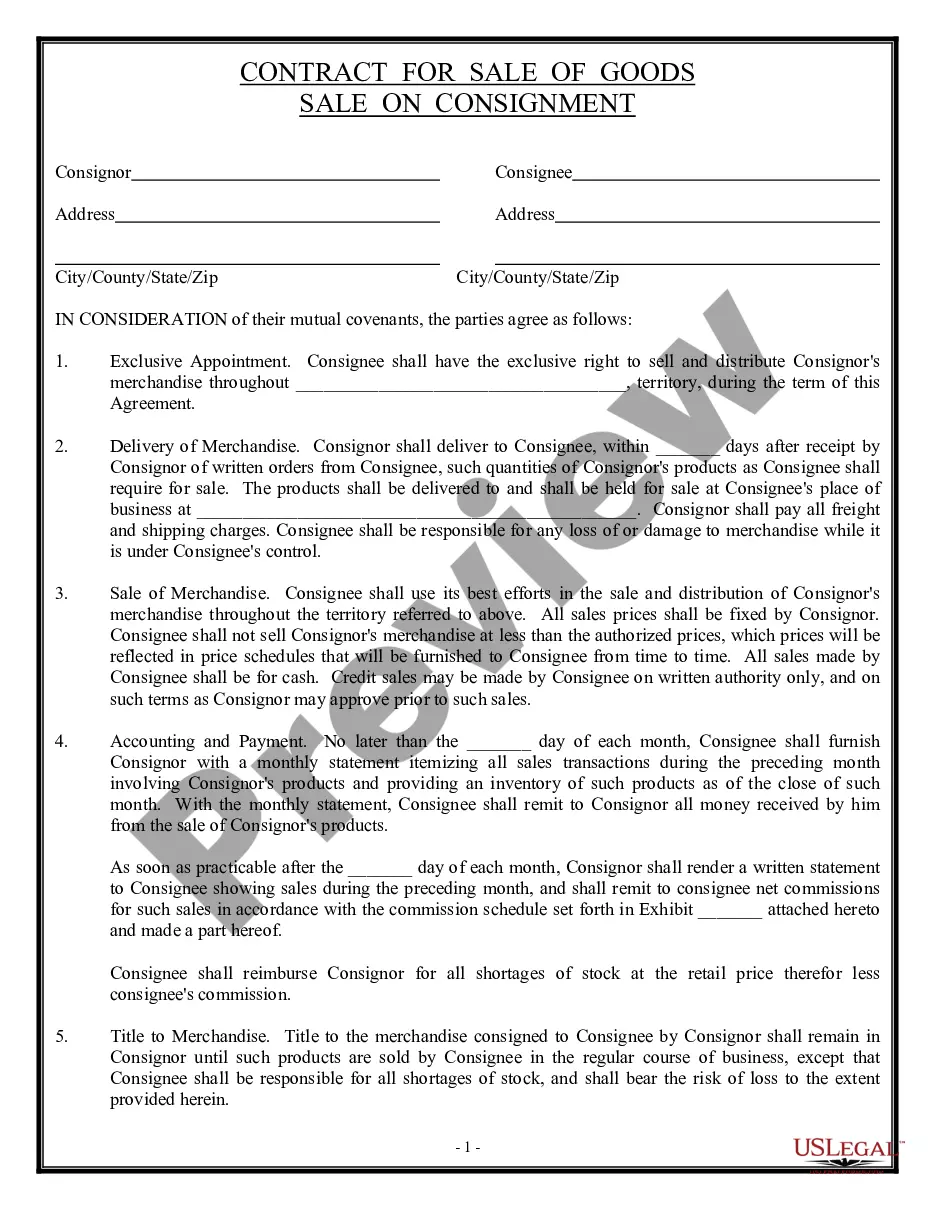

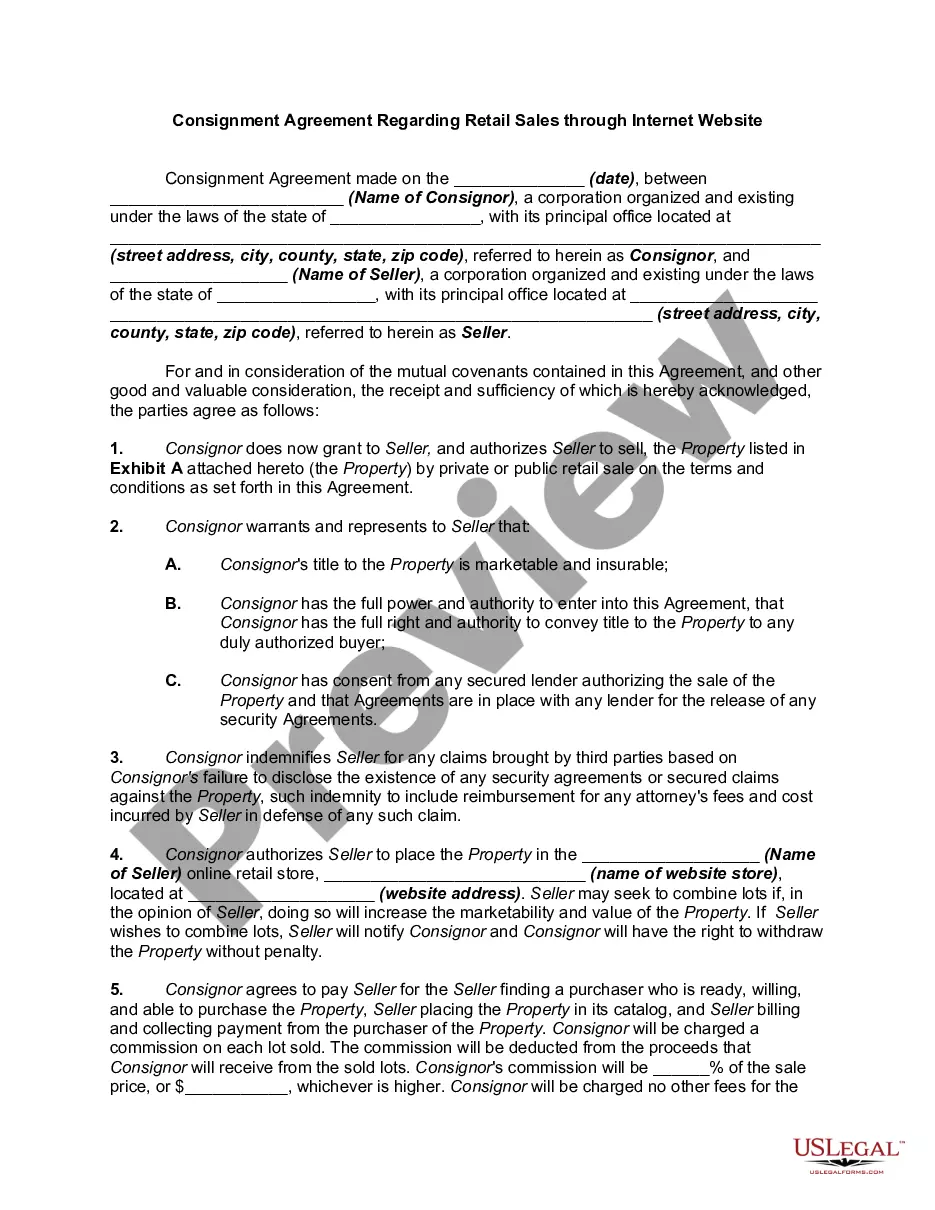

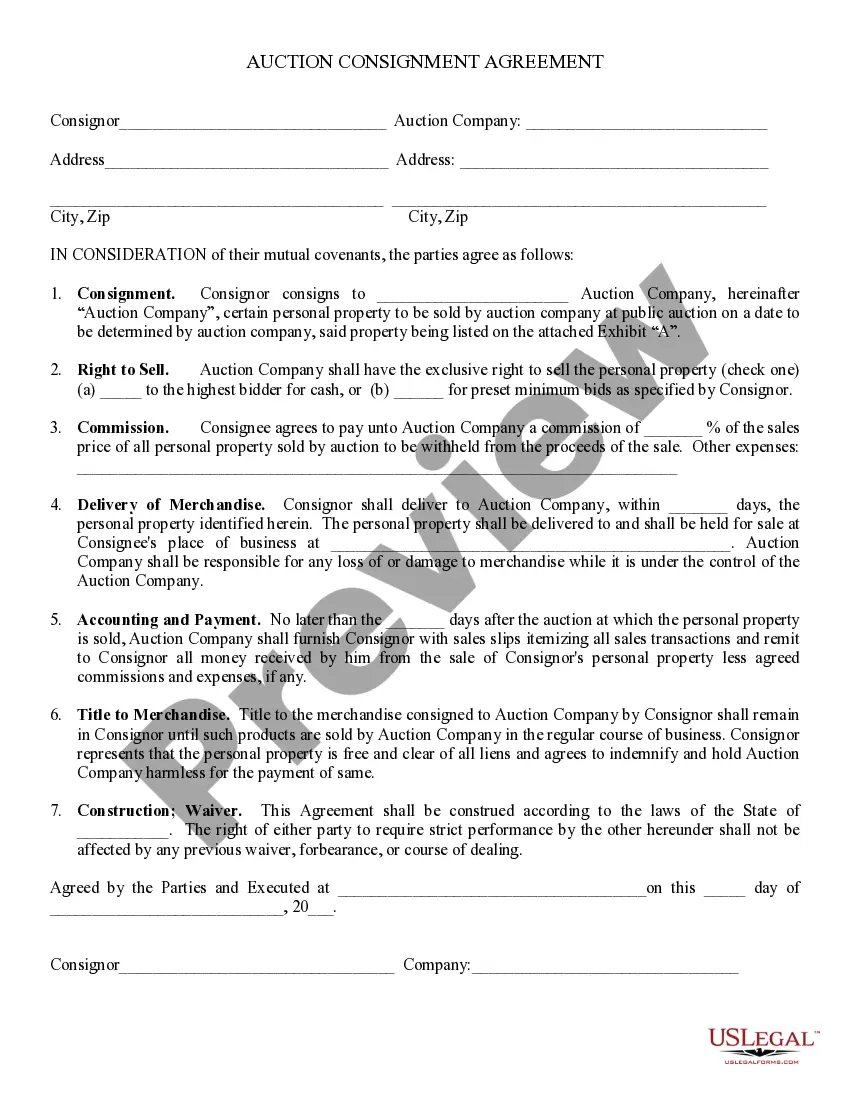

In a consignment agreement, a consignor supplies goods to a consignee, who sells them on the consignor's behalf. The consignee earns a commission from each sale and sends the remaining sales revenue to the consignor. The consignor retains ownership of the goods until they are sold.

Consignment is a type of contract in which the consignor delivers the goods to the consignee for sale . The consignee takes care of the goods and sells them. Until the goods are sold, the consignor does not lose ownership of the goods.

Please provide full description of goods, number of packages, gross weight and consignment dimensions. Customer reference. You can enter any internal reference code that you would like to be printed on the invoice, with a maximum of 24 characters. Delivery address. Dutiable shipment details.

This kind of arrangement is called Consignment. Definition. The contract or an agreement of sending several goods by the producers or manufacturers of a place to their agents for the sale is known as a consignment. Types of Consignment. Outward Consignment. Inward Consignment. Consignment Processing. Sale. Features of a Sale.

A consignment agreement, to be used where the seller (consignor) wishes to place goods on consignment before they are resold or used by the buyer (consignee). Goods will be stored at a facility or warehouse, under the control of the consignor, the consignee, or a third party.

A consignor does not recognize revenue when the goods are transferred to a consignee. Rather, the consignor would only recognize revenue when the goods are sold by the consignee to a 3rd party (i.e. customer).