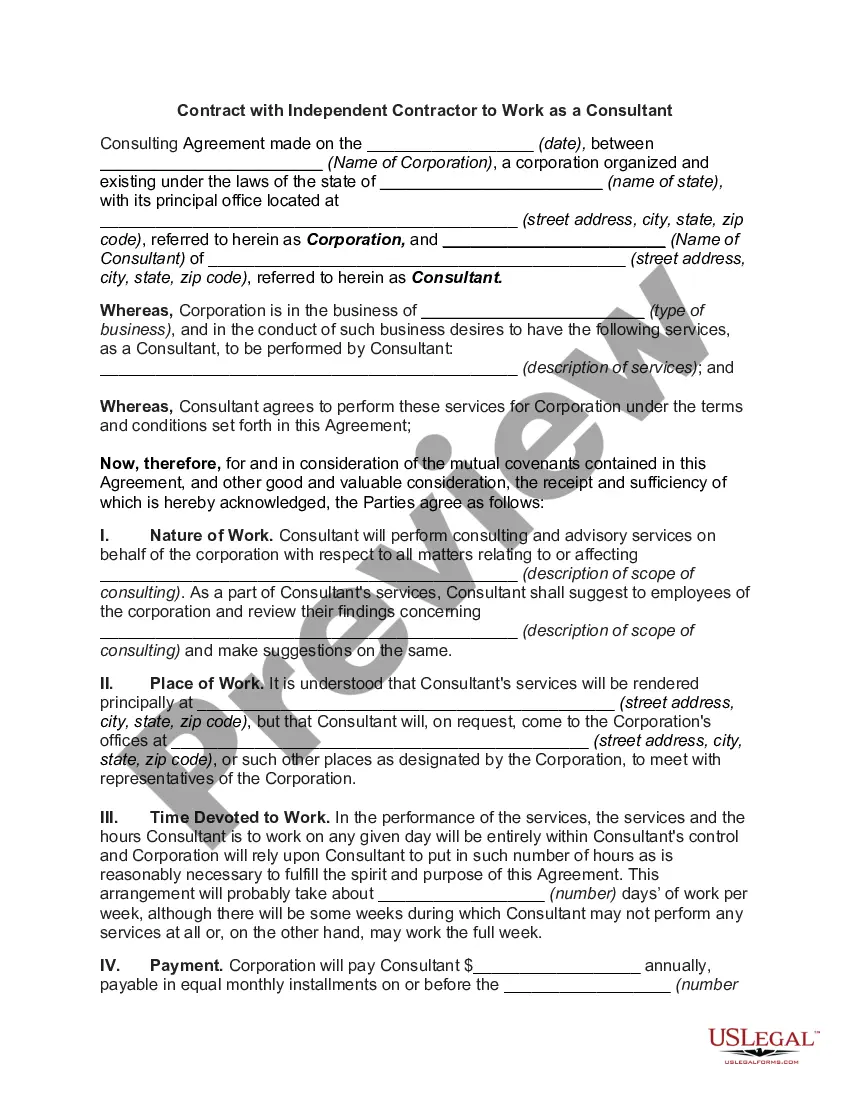

Consultant Contract Under Foreign Exchange In Utah

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

How to Get Your Utah Insurance License Complete an Insurance Exam Prep Course. Pass Your Utah Licensing Exam. Get Fingerprinted. Apply for a Utah Insurance License. Plan to Complete Required Insurance Continuing Education (CE) Credits.

Between the Life exam and the Accident & Health exam, the Life exam is easier, since Life insurance is more straightforward and less complicated than Health and Accident insurance. The best way to ensure you pass on the first try is to be well prepared. A pre-licensing prep course can help.

Public adjuster means a person required to be licensed under 31A-26-201 , opens in a new tab , who engages in insurance adjusting as a representative of insureds and claimants under insurance policies.

You must have obtained a general liability insurance certificate with minimum required coverage of $100,000 for each incident and $300,000 in total that covers and where DOPL is listed as certificate holder.

Other business insurance, like general liability, professional liability or a BOP, aren't required by the Utah law, but it's a good idea to have some type of coverage to protect from unexpected incidents. It's also common for a client or landlord to require business insurance before entering a contract or lease.

Yes! If the state discovers that you're working in an occupation without a required license, a host of bad things can happen: you'll undoubtedly be ordered to stop doing business, you might also be fined and, depending upon your occupation, failure to obtain a Utah business license could even constitute a crime.

You must have an UNEXPIRED general liability insurance certificate with minimum required coverage of $100,000 for each incident and $300,000 in total and where DOPL is listed as certificate holder.

Qualifier on current or previous Utah Contractor License for at least 2 years. Construction Management Degree (2 or 4 year Degree) Licensed Utah Professional Engineer. Passed NASCLA Examination for Commercial General Building Contractors.

General liability and builders risk are two of the most common insurance coverages that a construction business may need to obtain. One reason is that clients frequently require a contractor to have both builders risk and general liability policies in place, especially for large jobs.