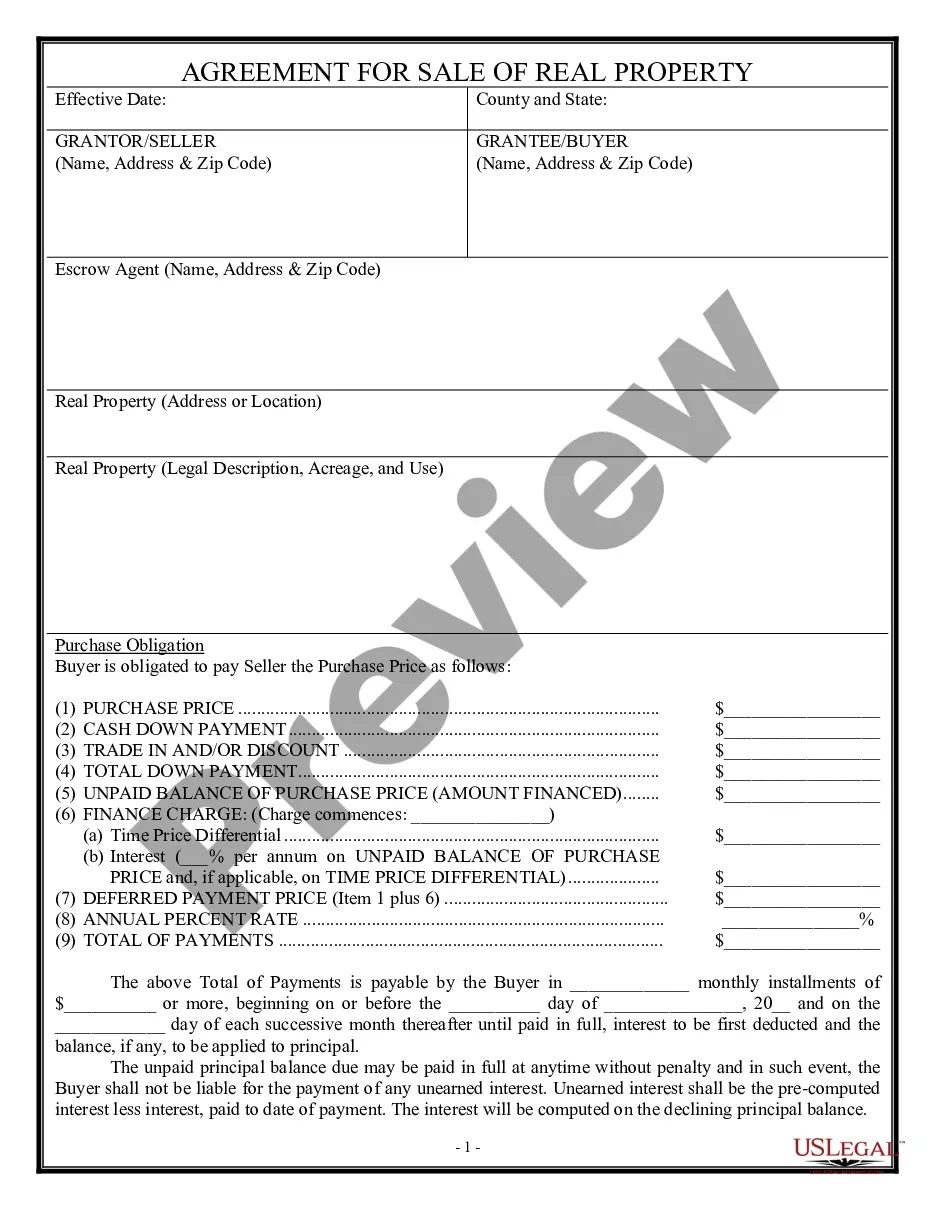

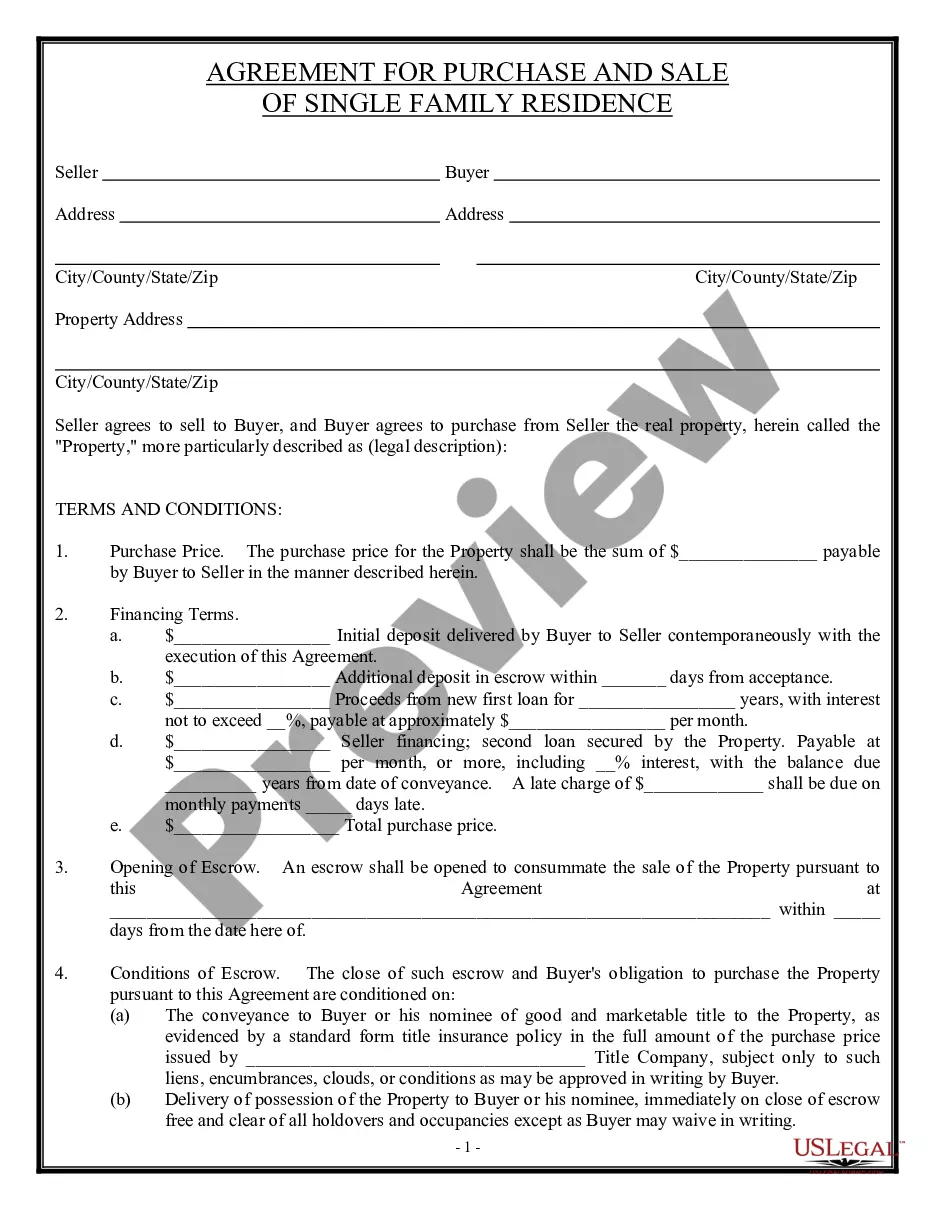

Closing Property Title With Mortgage In Kings

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The lender holds the actual legal title on the property while the borrower will hold equitable title. The lender holds title to the property in the name of the borrower through a document called a Deed of Trust.

The seller's attorney will give the original deed to the buyer's attorney at closing. That original then gets recorded at the clerk's office of the local municipality. The clerk's office scans and records the document into the land records and then sends it to the buyer or their attorney.

When you have a mortgage on your home, title is in your name so YOU are the legal owner of record.

The title (or property title) is not a document, but a concept that says you have the rights to use that property. So when you buy a property, you will receive the deed, a document that proves you have ownership. That deed is an official document that says you have title to the real estate.

A transfer of equity can be a good way to add or remove a name from your mortgage without remortgaging. However, there are some risks involved, so it's important to understand all the steps before getting started. If you're considering a transfer of equity, you may be able to avoid paying stamp duty land tax (SDLT).

Methods for Getting Out of a Mortgage Three of the most common methods of walking away from a mortgage are a short sale, a voluntary foreclosure, and an involuntary foreclosure. A short sale occurs when the borrower sells a property for less than the amount due on the mortgage.

Yes, a mortgage offer can be revoked by the provider at any time after it's been issued. Make sure you thoroughly read all the information you receive with your mortgage offer, as there should be a section detailing the circumstances in which it may be withdrawn.

A joint mortgage can be transferred to one person, providing your lender agrees to it - they will need to assess your income and expenditure to see if you meet their affordability requirements.

Risks for buyers Higher interest rates – Although wraparound mortgages are easier to obtain, they often come with a higher interest rate. Higher rates lead to bigger monthly payments, which can put a strain on your finances.

During the Wraparound process, a team of people who are relevant to the life of the child or youth (e.g., family members, members of the family's social support network, service providers, and agency representatives) collaboratively develop an individualized plan of care, implement this plan, monitor the efficacy of ...