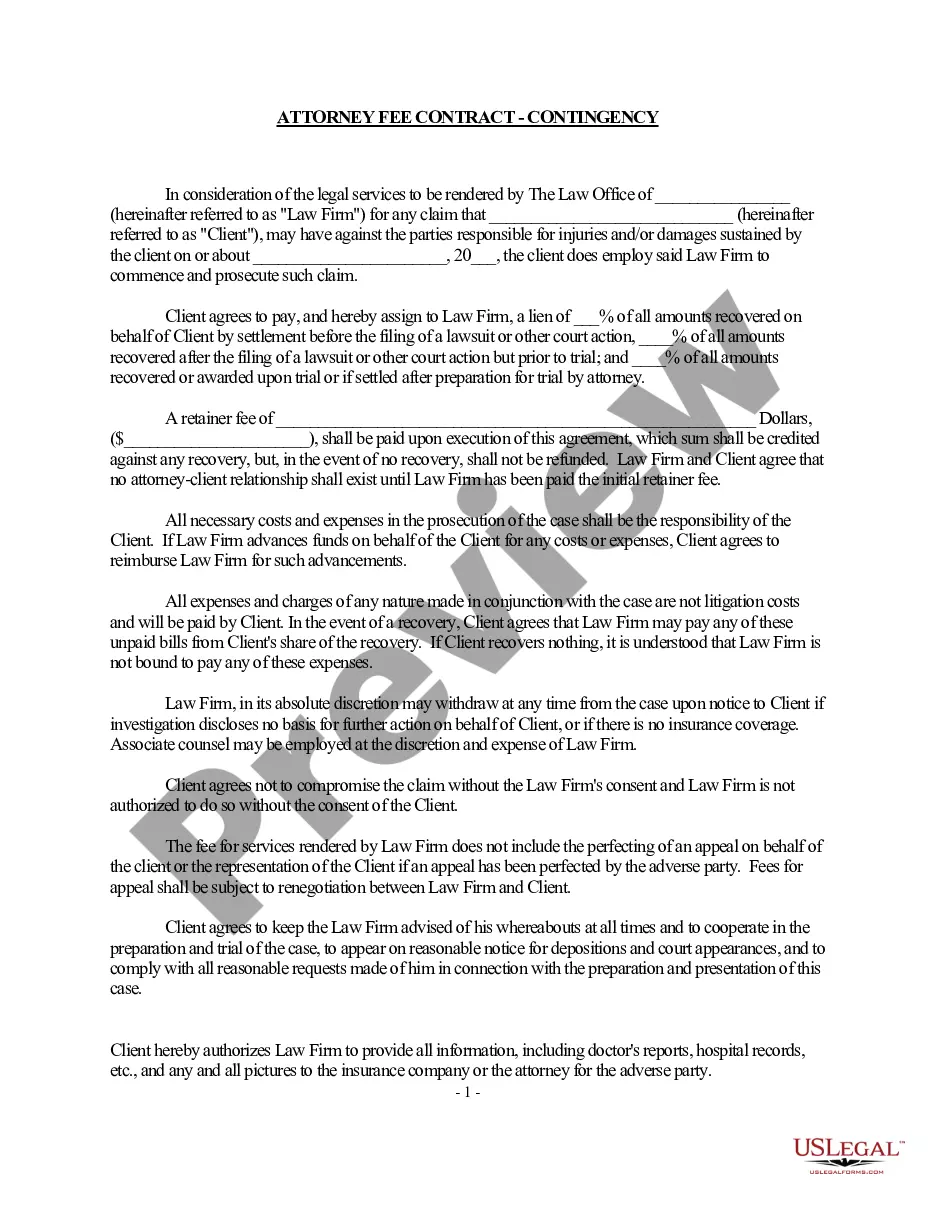

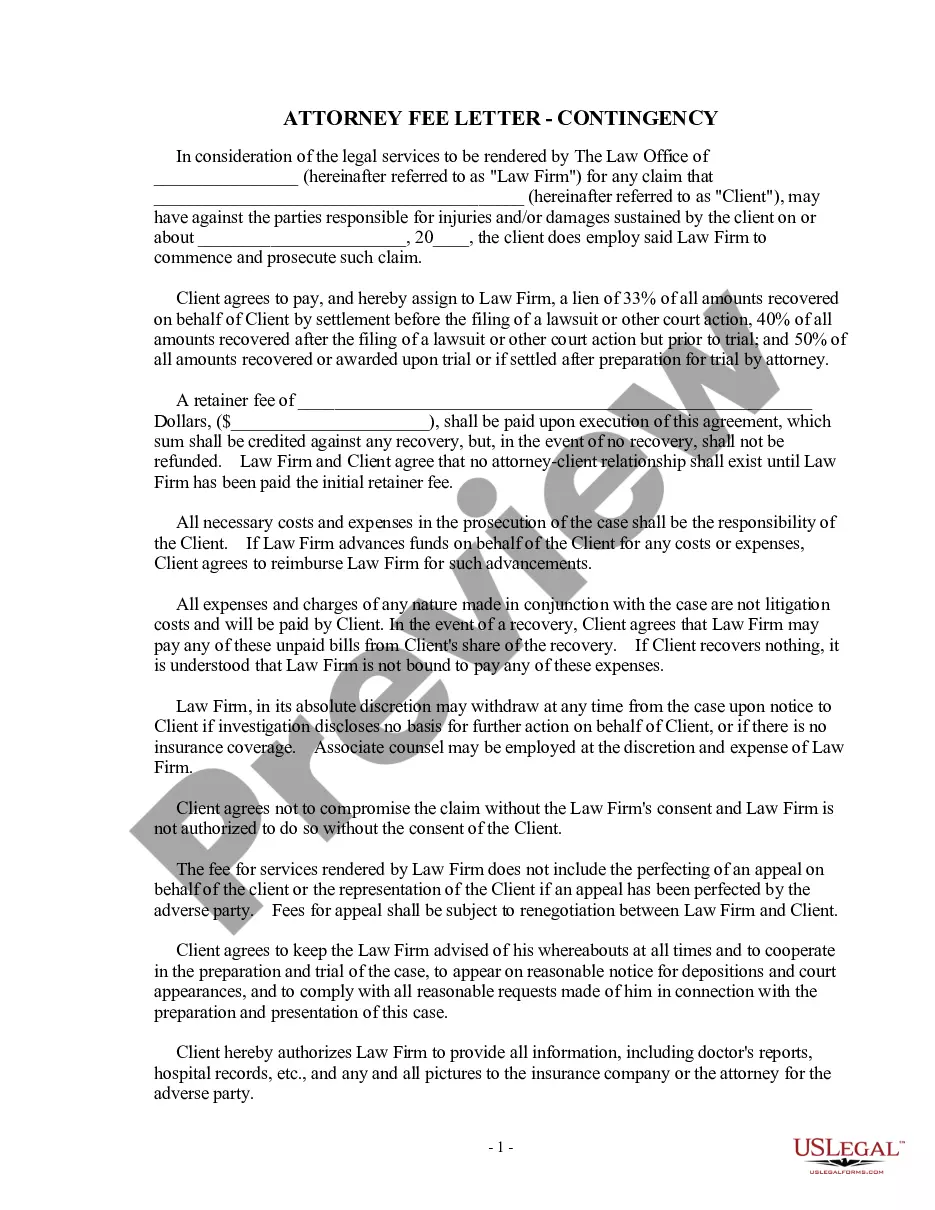

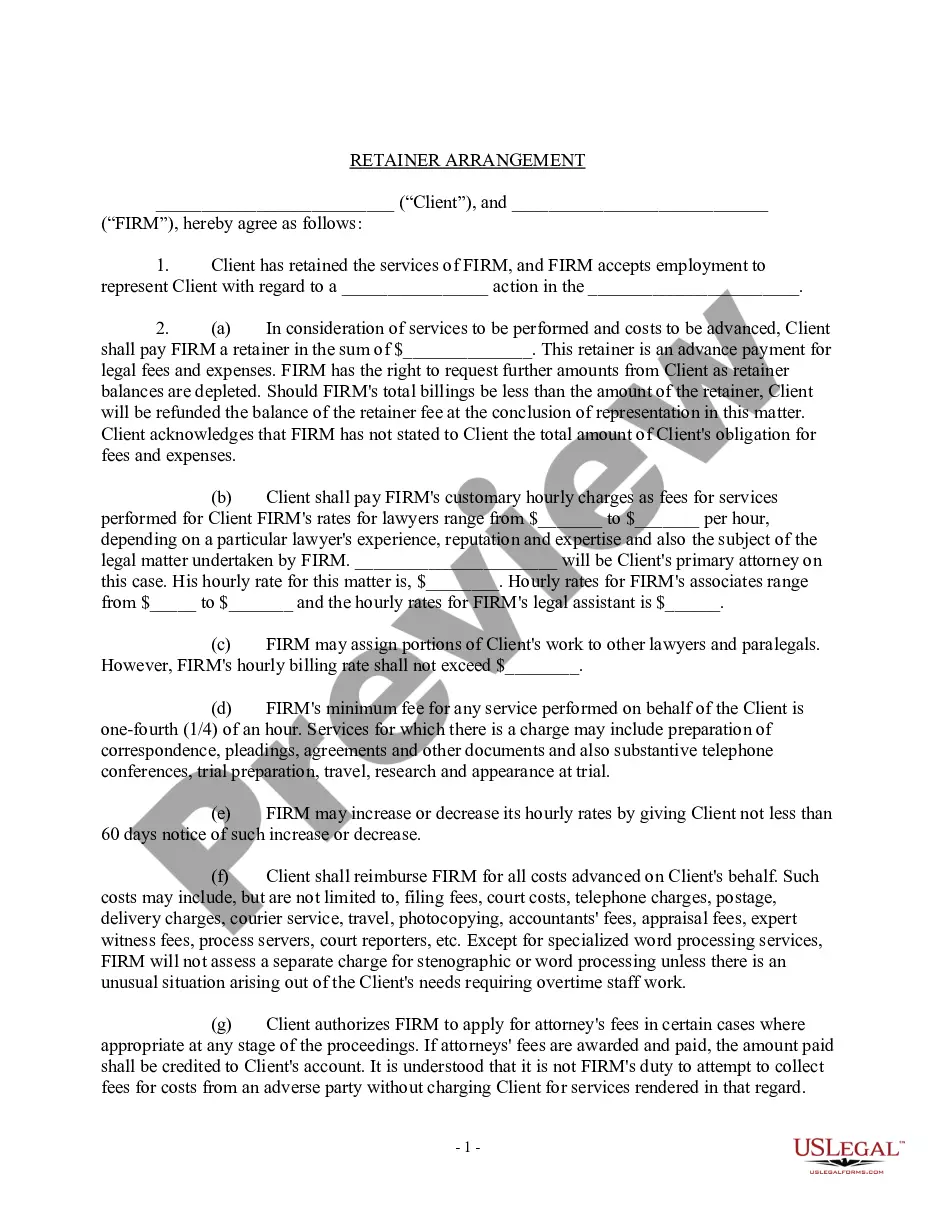

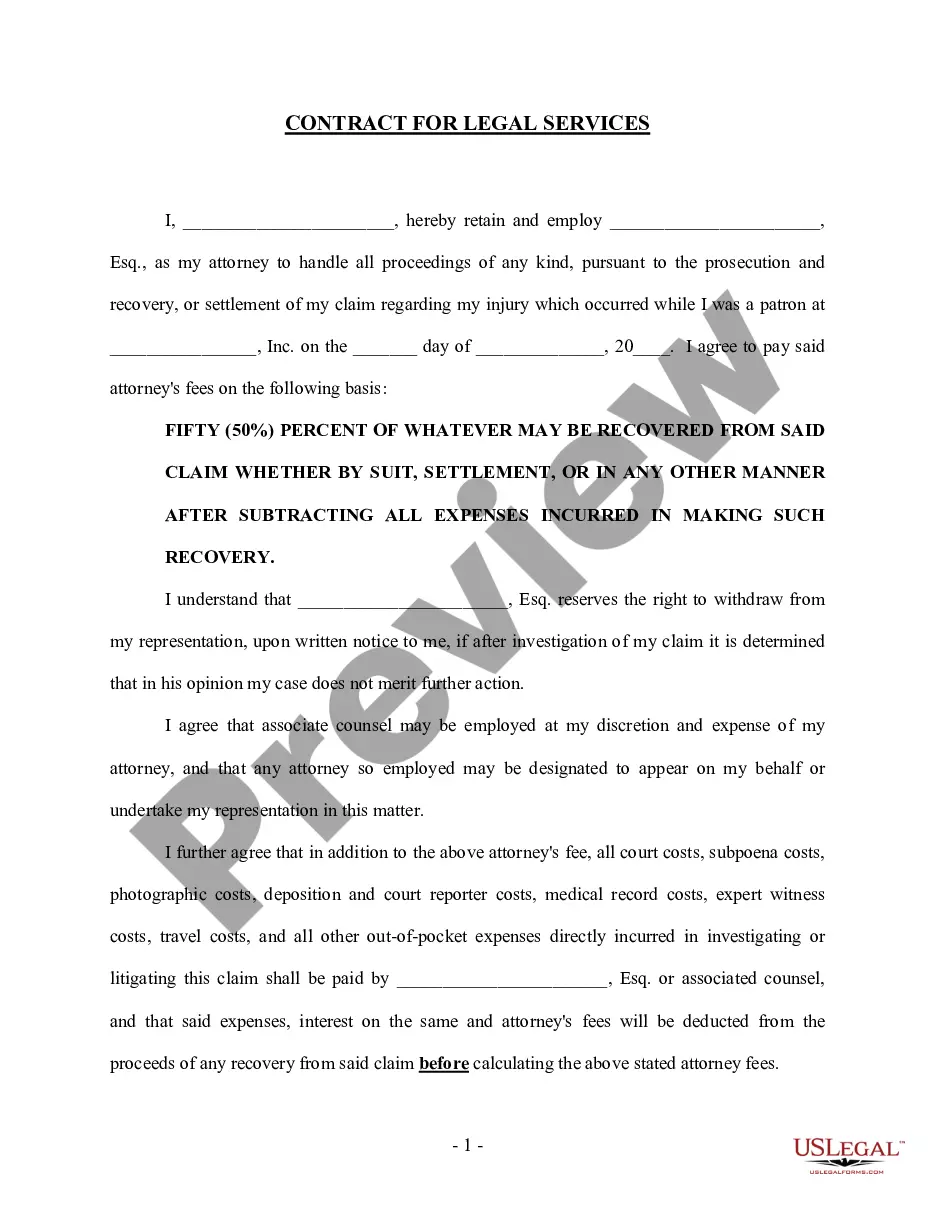

Contingency Fee For Erc In Massachusetts

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Contingent fees are also permitted for interest and penalty reviews and for services rendered in connection with a judicial proceeding arising under the Internal Revenue Code.

Contingent fees are also permitted for interest and penalty reviews and for services rendered in connection with a judicial proceeding arising under the Internal Revenue Code.

Going forward, the only way to apply for the ERC is to file an amended Form 941X (Quarterly Federal Payroll Tax Return) for the quarters during which the company was an eligible employer.

The Massachusetts Department of Revenue announced withholding tables for the fiscal year beginning January 1, 2024. The new withholding method includes a surtax on earnings of $1,053,750 or more. While income under $1,053,750 is taxed at 5%, annual income above $1,053,750 will be taxed at 9%.

The following categories of sales or types of transactions are generally exempted from the sales/use tax: Food & clothing. Periodicals. Admission tickets. Utilities and heating fuel. Telephone services to residential users. Shipping and Transportation services. Personal or professional services. Casual and isolated sales.

Social Security benefits are not included in Massachusetts income. For federal purposes, these benefits may be included in federal gross income depending on income thresholds. Pension Income is generally included in both Massachusetts and federal income.

The ERC tax credit does not count towards income tax in Massachusetts. Businesses who earn over the amount they owed in taxes for that calendar year will receive the rest as a refund. This refunded amount will not be taxed on that year's tax return if your business is located in the Commonwealth of Massachusetts.

On Form 1120S, businesses can report the ERC by including it as a credit on Line 13f (“Credits”) of Schedule K, Form 1120S. Ensure accurate documentation of qualified wages and related expenses to support the credit claim.

Because the ERC is considered an income-related grant under IAS 20, an entity may elect to present the income in one of two ways: (1) gross as a grant or other income item, or (2) net as a deduction from the expense category in which the reporting entity reports employment taxes (typically employee compensation).

The State Board rules do not allow commissions or contingent fees if the CPA performs, for the client, "...a compilation of a financial statement accompanied by a report..." The AICPA rules prohibit commissions or contingent fees if the CPA performs, for the client, "... a compilation of a financial statement when the ...