Interest Only Promissory Note With Balloon Payment In Riverside

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

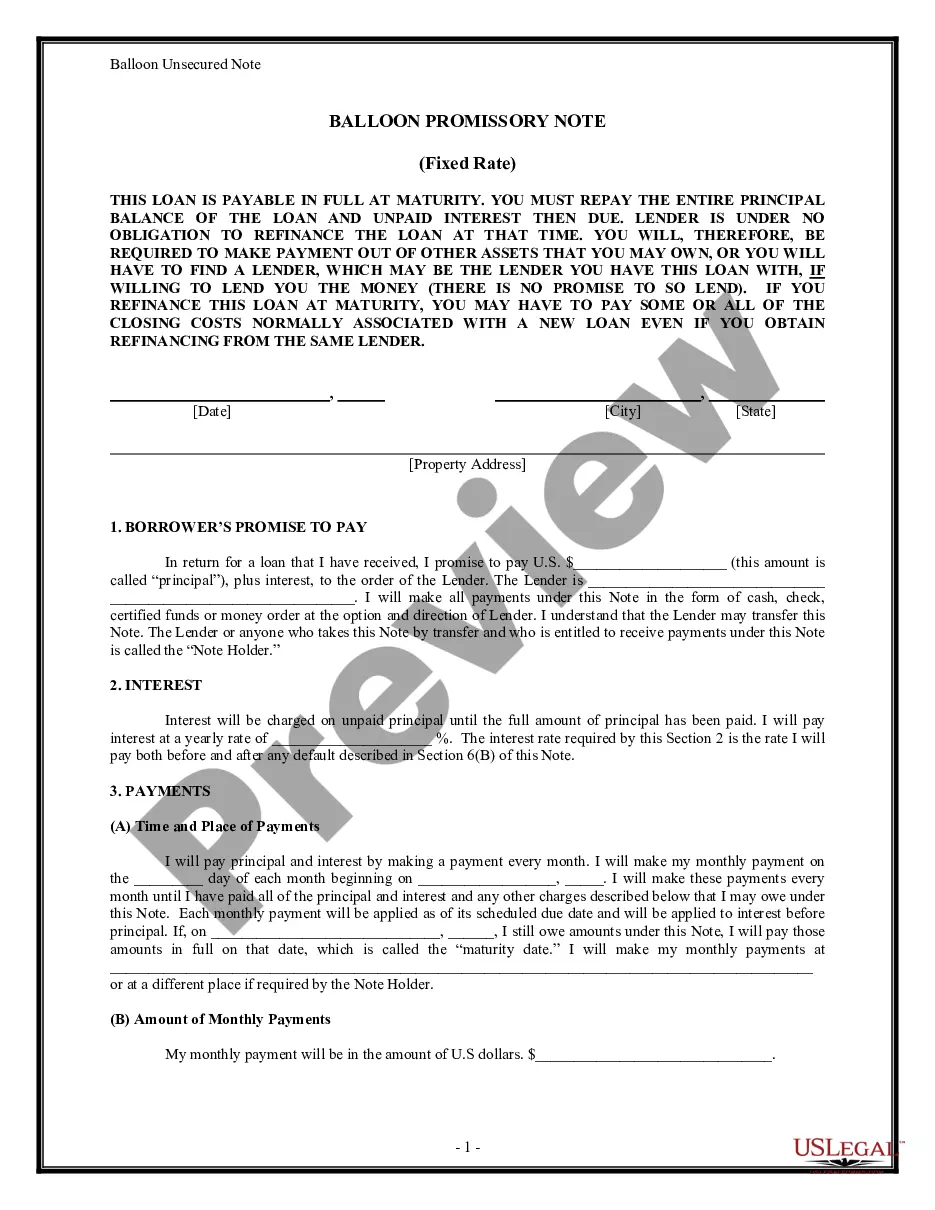

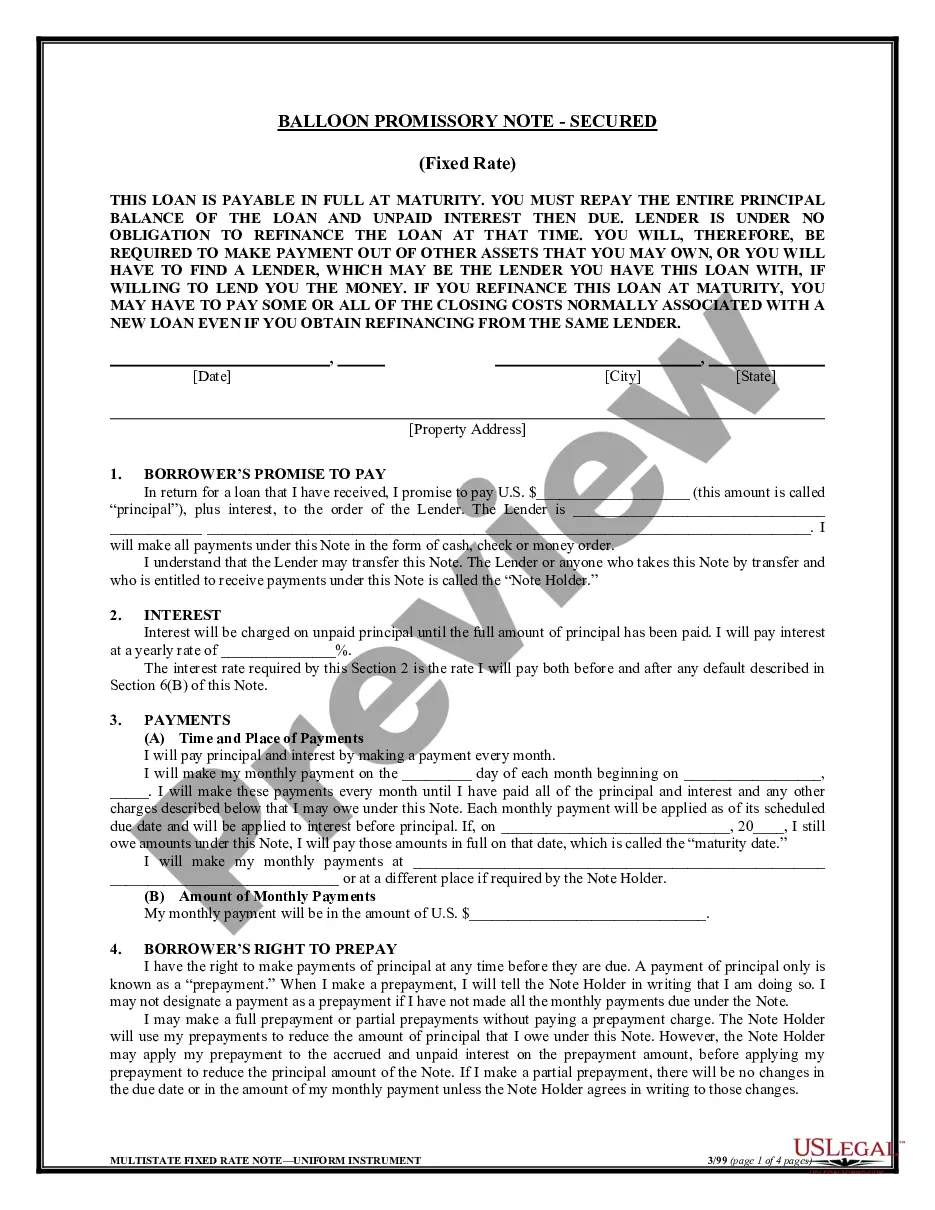

Interest-only mortgages are nonqualified mortgage (non-QM) loans, which means they come with features that the Consumer Financial Protection Bureau (CFPB) considers potentially risky. These include the interest-only period itself as well as, in some cases, a balloon payment.

The most significant risk of a balloon mortgage is foreclosure if the borrower can't make the balloon payment at the end of the term. Foreclosure can result in the loss of the home, emotional distress, and impact the borrower's credit negatively, generally for seven years.

There may or may not be a balloon payment at the end of an interest-only mortgage. It's more common for the monthly payments to increase after an initial, interest-only period of between five and 10 years.

The balloon amount is calculated based on the predicted future value of the vehicle at the end of the contract, known as the Guaranteed Minimum Future Value (GMFV). Balloon payments are often associated with PCP agreements but can also be applied to HP finance.

Promissory notes with balloon payments are a financing option you may be considering for your business. These types of loans may be secured by collateral or not, but they always end their repayment schedule with a big payment, known as the balloon payment.