Letter For Recovery Debt In King

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Verify the summons: Contact the court listed on the summons to confirm the case number and parties involved. If the court doesn't have a record of the case, or the information doesn't match the summons, it's likely .

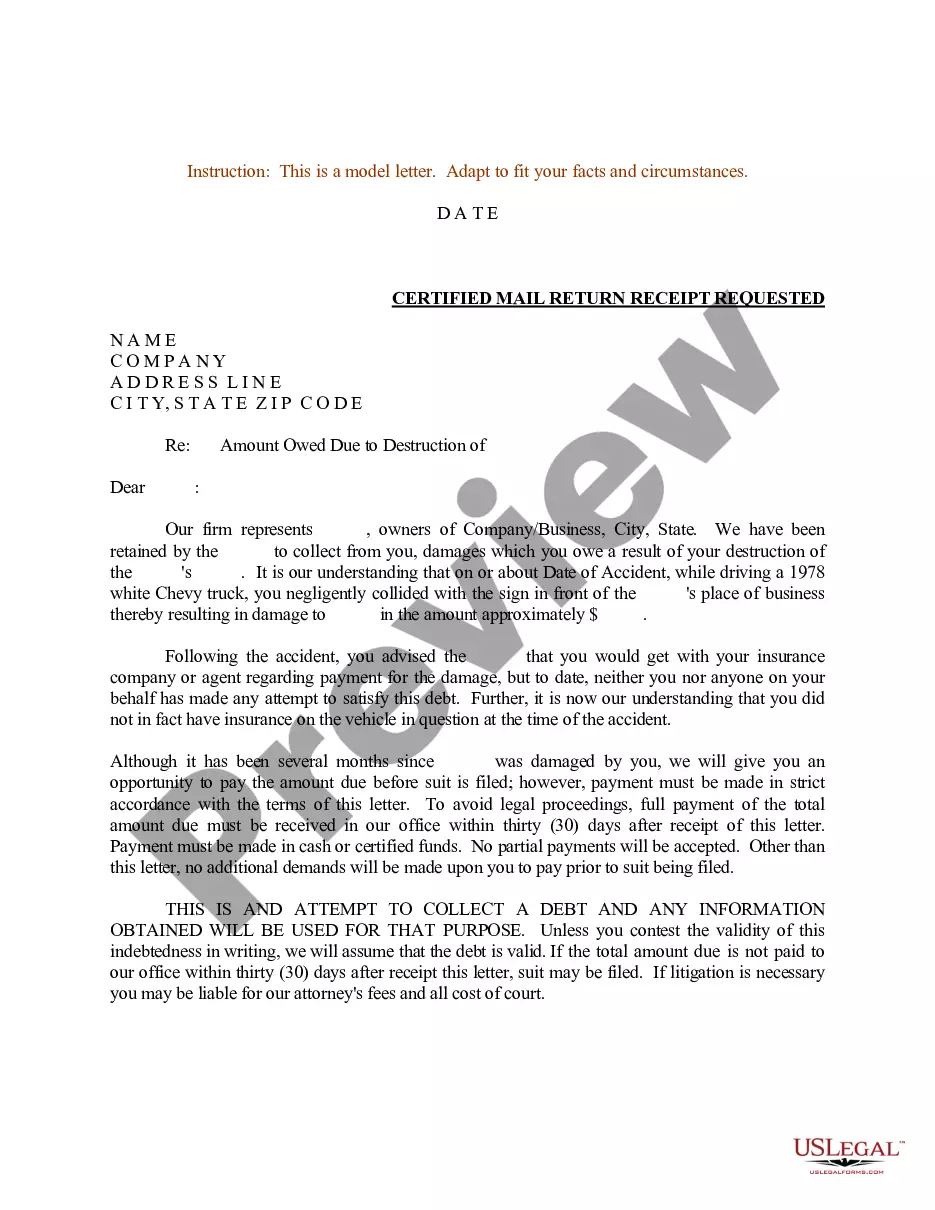

Place. Include the dollar amount of the debt owed the original due. Interest gained and/orMorePlace. Include the dollar amount of the debt owed the original due. Interest gained and/or additional fees accured. Sometimes there might be multiple sub accounts or amounts involved with a debtor.

How to write a debt collection letter: Step by step guide Step 1: Use a professional format. Step 2: Write a clear subject line (if sending via email) ... Step 3: Address the recipient. Step 4: State the purpose of the letter. Step 5: Provide detailed information on the debt. Step 6: Include payment instructions.

To verify a debt collector, ask them to provide: Their name. Company name. Company street address. Telephone number. Professional license number, if your state licenses debt collectors.

Letter of claim The letter should tell you the amount of the debt and whether interest is being added. If there was no written agreement, the letter should tell you who made the agreement, what was agreed, and when and where it was agreed.

Dear Creditor: Please provide me with verification of the debt which you state I owe. Please provide me with any records which are in your possession, including, but not limited to, all statements of each account, invoices, and any other documentation which I may have signed.

(3) An action upon any judgment shall not be brought after the expiration of 12 years from the date on which the judgment became enforceable and no arrears of interest in respect of any judgment debt shall be recovered after the expiration of 6 years from the date on which the interest became due.

Unfortunately, my circumstances are unlikely to improve in the foreseeable future and I have no assets to sell to help clear my debt. I am therefore asking you to consider writing off my debt as I can see no way of ever repaying it. If you are unable to agree to this, please explain your reasons.

Yes it does actually work. Collectors rarely actually validate the debt because most of the debts in fact are not valid. Some just back off because receiving a well worded debt validation letter means you have consulted the FDCPA (or at least a good debt/credit forum) and know what you're doing.

Federal law requires collection agencies to provide debt validation notices, so you don't need to request one. In some cases, a collector may provide the validation letter as its initial communication to you. If not, they must provide it within five days of their first communication, either in the mail or via email.