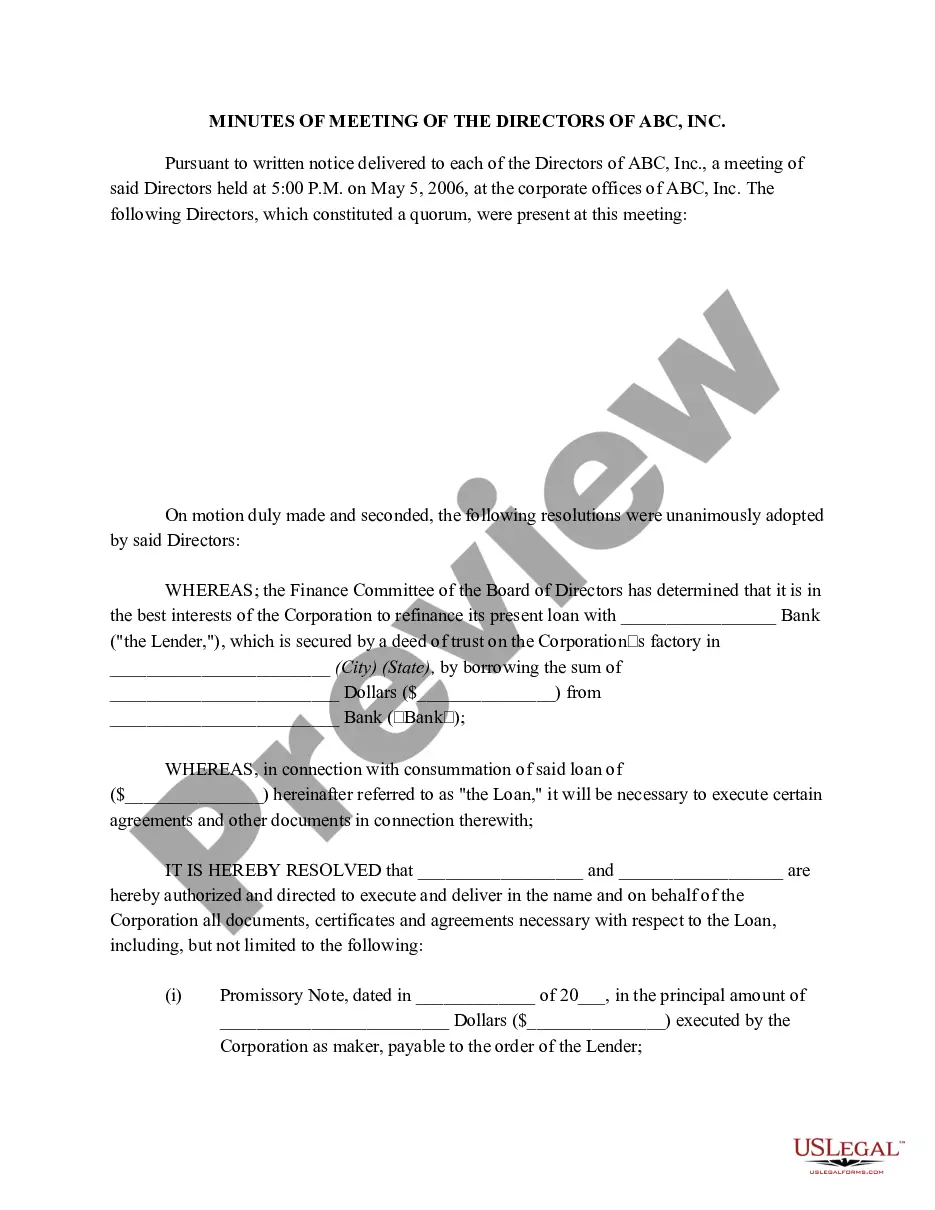

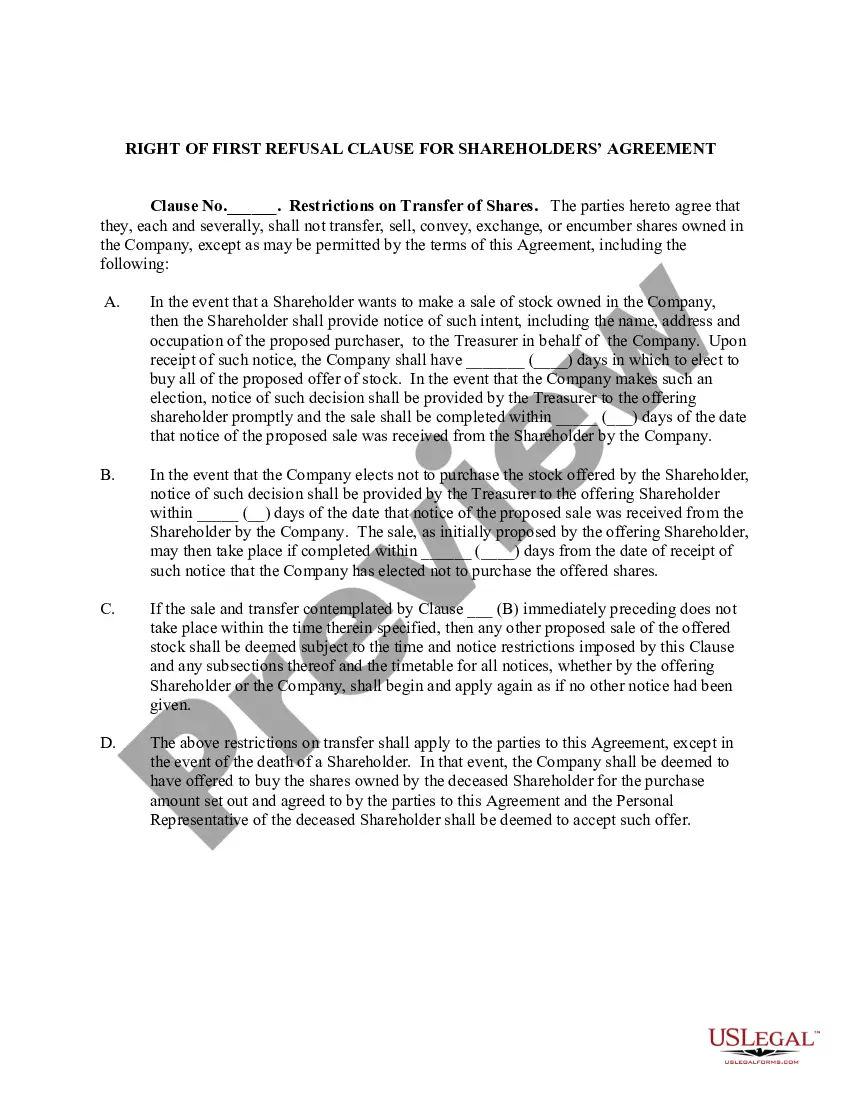

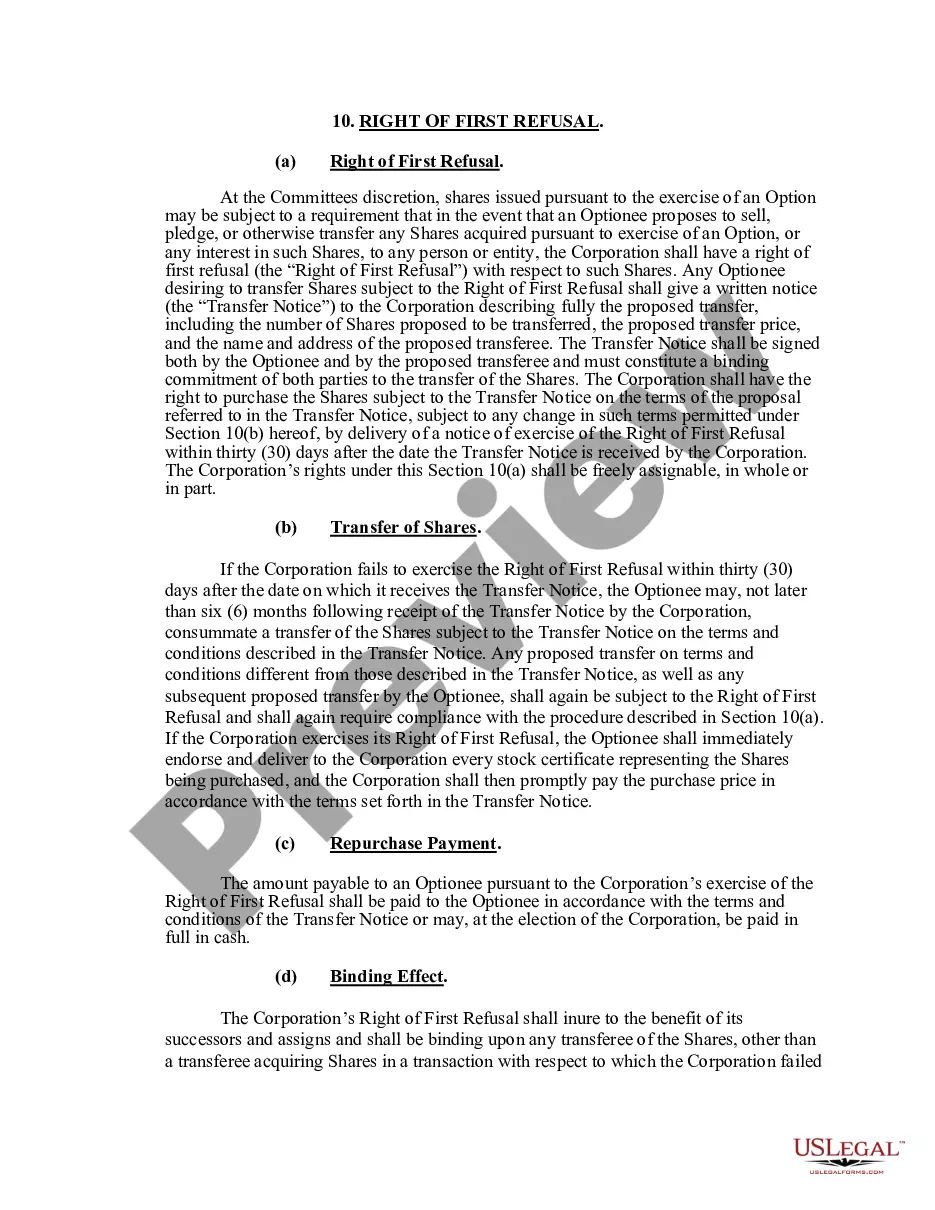

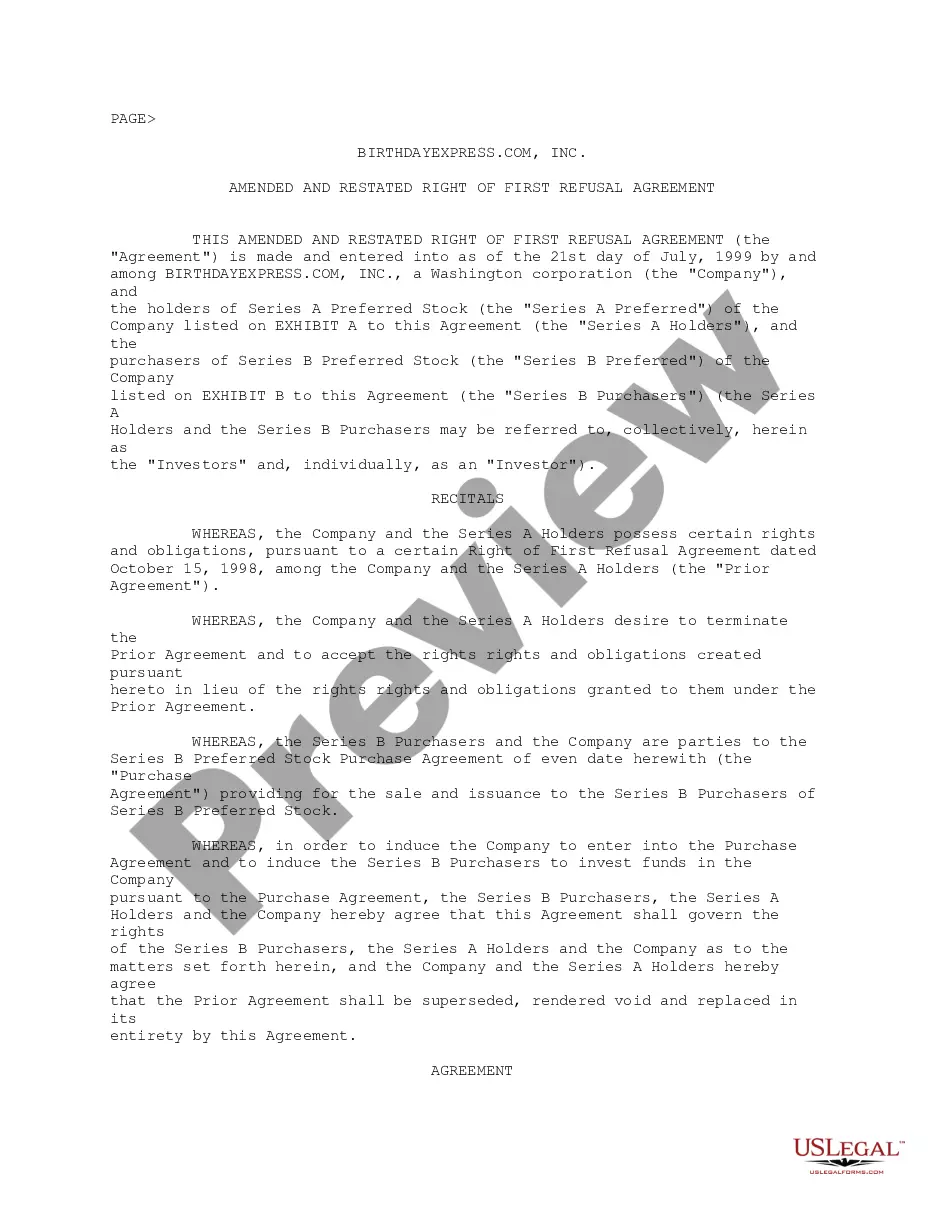

Corporate Refusal For 401 In California

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Are other forms of retirement income taxable in California? Retirement account income, including withdrawals from a 401(k) or IRA, is considered taxable income in California. So is all pension income, whether from a government pension or a private employer pension.

Are retirement accounts protected from theft? No, not always in the same way that credit cards and bank accounts are. Custodians usually pledge to return any funds that went missing. However, that assurance can come with conditions that aren't always easy to prove and meet.

California employers that meet certain requirements must offer a retirement plan by a specific date — either a plan through the state-sponsored CalSavers program, or by establishing their own qualified retirement plan: 401(a), 401(k), 403(a), 403(b), 408(k), or 408(p).

Protecting Private Retirement Plans From Creditors Under California Code of Civil Procedure § 704.115, assets held in private retirement plans are fully exempt from execution, both before and after distribution to the judgment debtor.

After June 2022, all employers in the state with at least five W-2 employees must provide a qualified retirement savings plan—such as a 401(a), 401(k), 403(a), 403(b), 408(k), 408(p), or 457(b), to their employees—or offer the state-run option.

Is CalSavers mandatory for employers to register? After June 2022, all employers in the state with at least five W-2 employees must provide a qualified retirement savings plan—such as a 401(a), 401(k), 403(a), 403(b), 408(k), 408(p), or 457(b), to their employees—or offer the state-run option.

In California, key bankruptcy exemptions include up to $600,000 in home equity, $3,325 in vehicle equity, protected retirement accounts, personal belongings, and public benefits such as Social Security. Exemptions help filers keep essential property while resolving debt through Chapter 7 or Chapter 13 bankruptcy.

Under California's community property divorce law, if a couple divorces, a judge will divide all property, assets and debts evenly – as close to a 50/50 split as possible. This means your ex-spouse could receive up to 50% of your 401(k) and pension plan.

California does not tax the IRA distributions, qualified pension, profit sharing, and stock bonus plans of a nonresident. California taxes compensation received by a nonresident for performance of services in California.

Dipping into a 401(k) or 403(b) before age 59 ½ usually results in a 10% penalty.