Consumer Reporting Agency Under Fcra In Wake

Description

Form popularity

FAQ

The FCRA's requirements for adverse action notices apply only to consumer transactions and are designed to alert consumers that negative information was the basis for the adverse action.

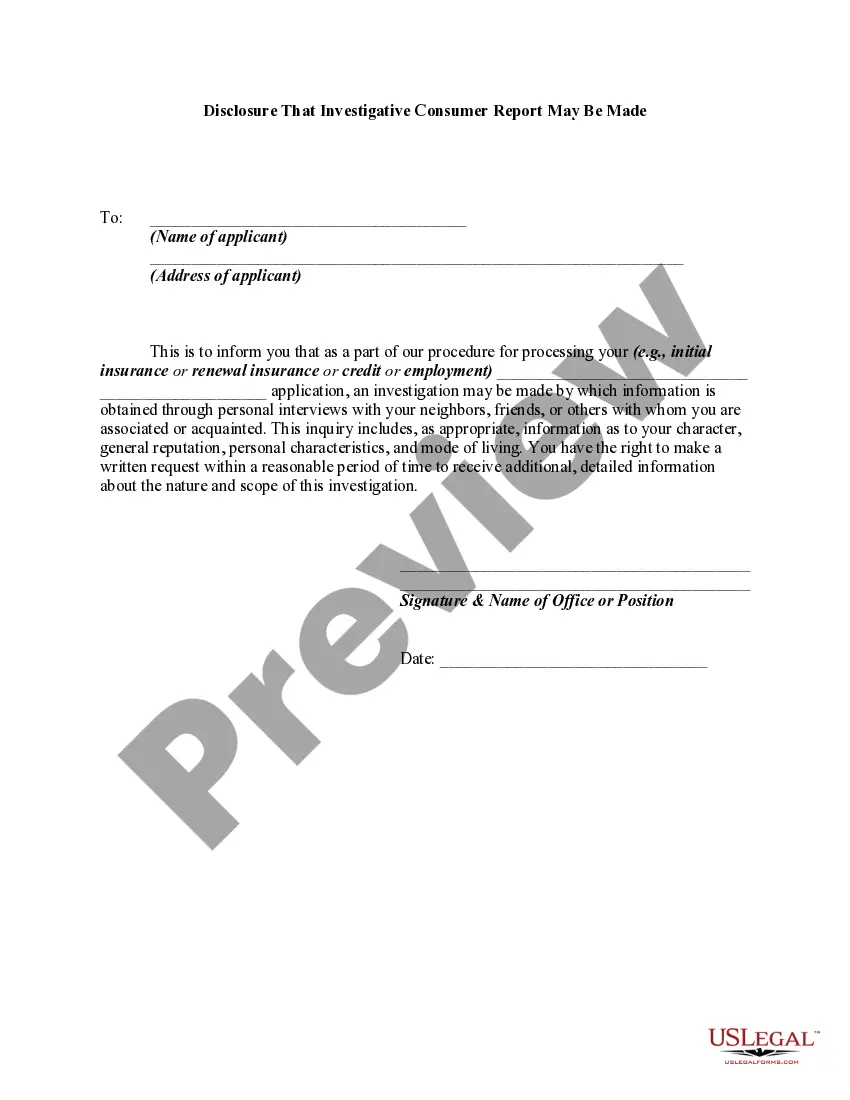

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

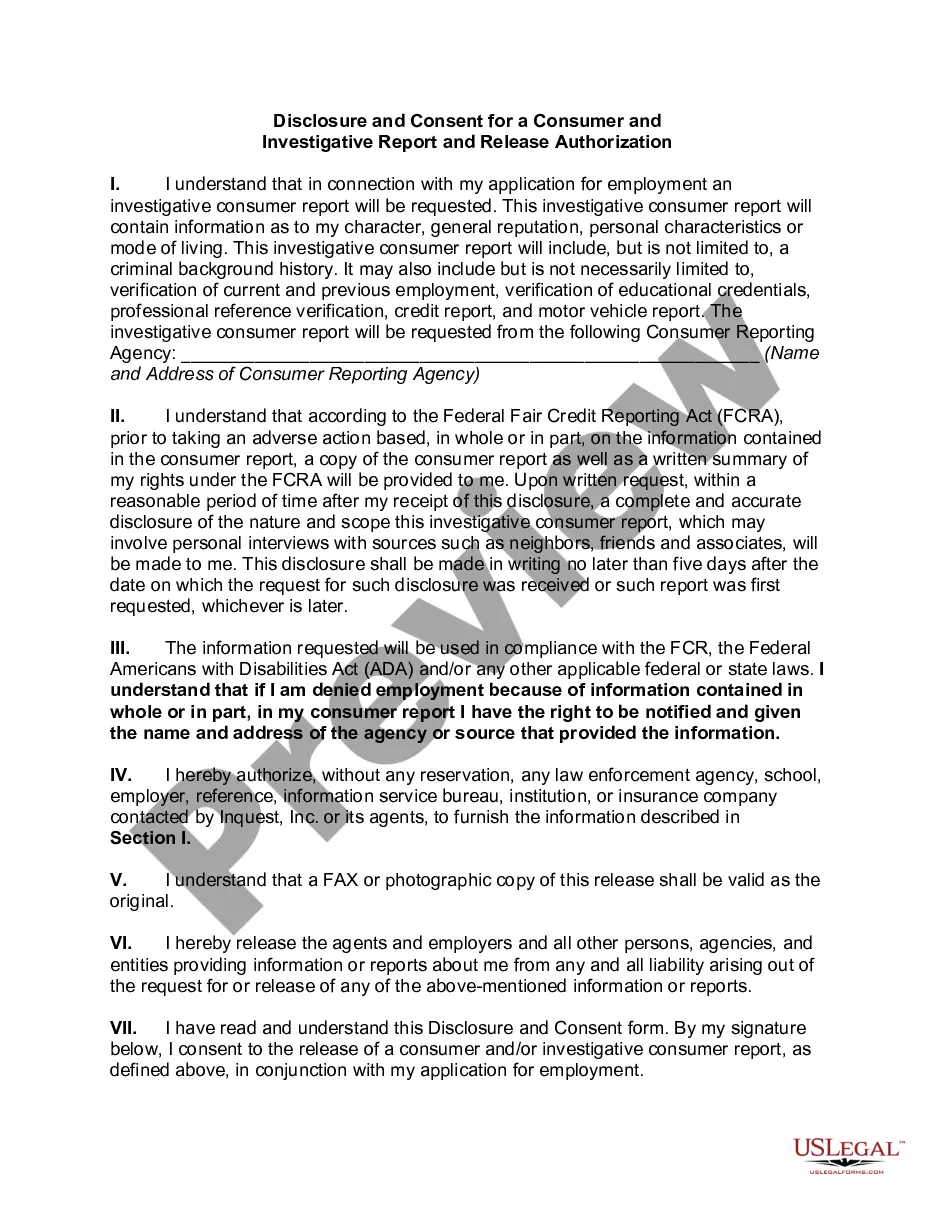

Background screening reports are “consumer reports” under the FCRA when they serve as a factor in determining a person's eligibility for employment, credit, insurance, housing, or other purposes and they include information “bearing on a consumer's credit worthiness, credit standing, credit capacity, character, general ...

The compliance requirements for the credit reporting agencies include the following: Establish FCRA Policies. Review FCRA Provisions & Applicability. Establish Smooth Consumer Consent Acquisition Processes. Ensure Reports Are Used Only for Permissible Purposes. Provide Adverse Action Notices.

Consumer reporting companies collect information and provide reports to other companies about you. These companies use these reports to inform decisions about providing you with credit, employment, residential rental housing, insurance, and in other decision-making situations.

A creditor must provide notice if it has: Taken adverse action on a completed credit application; Taken adverse action on an incomplete credit application; Taken adverse action on an existing credit account; or.

Under Section 609(a) of FCRA, all consumer reporting agencies must clearly and accurately disclose to a consumer, upon request, “all information in the consumer's file at the time of request” and “the sources of the information.” Moreover, FCRA defines a consumer's file as “all of the information on that consumer ...