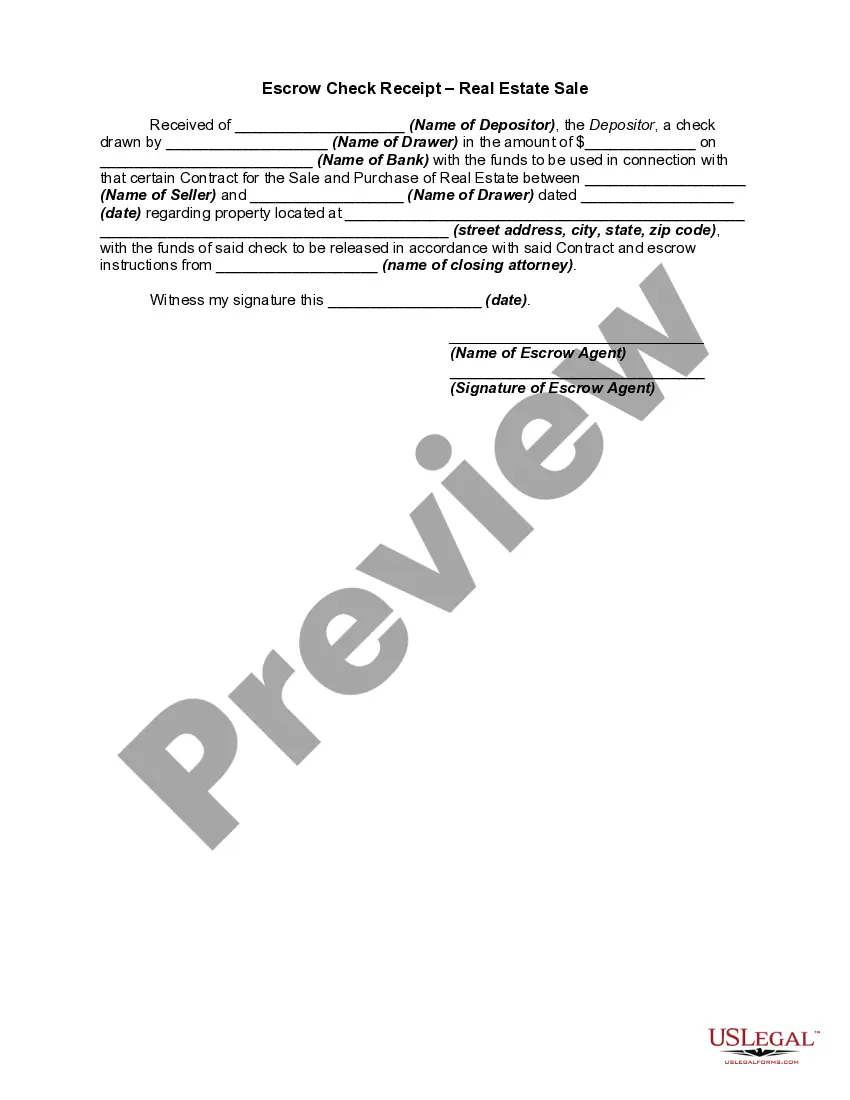

Escrow Agreement For Repairs In Palm Beach

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The 3 Requirements of a Valid Escrow The Contract between the Grantor and the Grantee. Delivery of the Deposited Item to a Depositary. Communication of the Agreed Conditions to the Depositary.

In conclusion, escrow holdbacks for repairs can be a valuable solution in real estate transactions, providing a structured way to address necessary repairs while keeping the sale on track.

Keeping the Escrow Funds: A third-party will oversee the escrow account until the closing date. This is done in ance with Florida Statutes § 651.033, which state that a certified financial institution must hold the escrow funds for the duration of the transaction. There's a clear logic behind this law.

Another potential downside to escrow accounts lies in the risk of mishandling or mismanagement. In some cases, errors or discrepancies in managing escrow funds can lead to a shortage of funds when it's time to settle property taxes or insurance premiums.

An escrow holdback for repairs is a financial arrangement where a portion of the homebuyer's funds is withheld by the lender or escrow agent until specific repairs or improvements are completed. This arrangement is typically used when there are issues with the property that need attention before the sale can close.

In an escrow agreement, one party—usually a depositor—deposits funds or an asset with the escrow agent until the time that the contract is fulfilled. Once the contractual conditions are met, the escrow agent will deliver the funds or other assets to the beneficiary.

How To Open An Escrow Account. Typically, the escrow account is most often opened by the seller's real estate agent, but escrow may be opened by anyone involved in the transaction. Escrow may be opened via phone call, email, or in person; or, click here to open an escrow account on Escrow of the West's website.

The Escrow Holder: prepares escrow instructions. requests a preliminary title search to determine the present condition of title to the property. requests a beneficiary's statement if debt or obligation is to be taken over by the buyer. complies with lender's requirements, specified in the escrow agreement.

On your paper mortgage statement or your account dashboard online, you'll see two different balances if you have an escrow account: the escrow balance and the principal balance. Your escrow balance is the amount held for payments like insurance and property taxes.