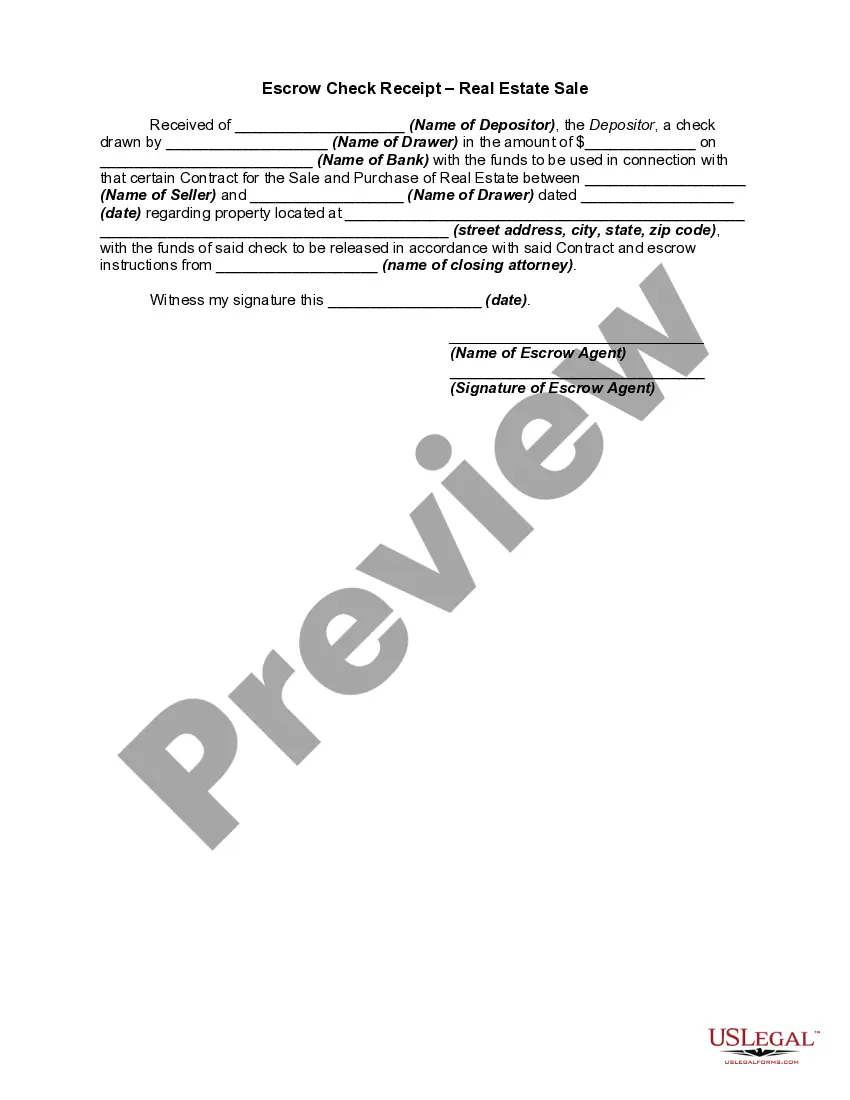

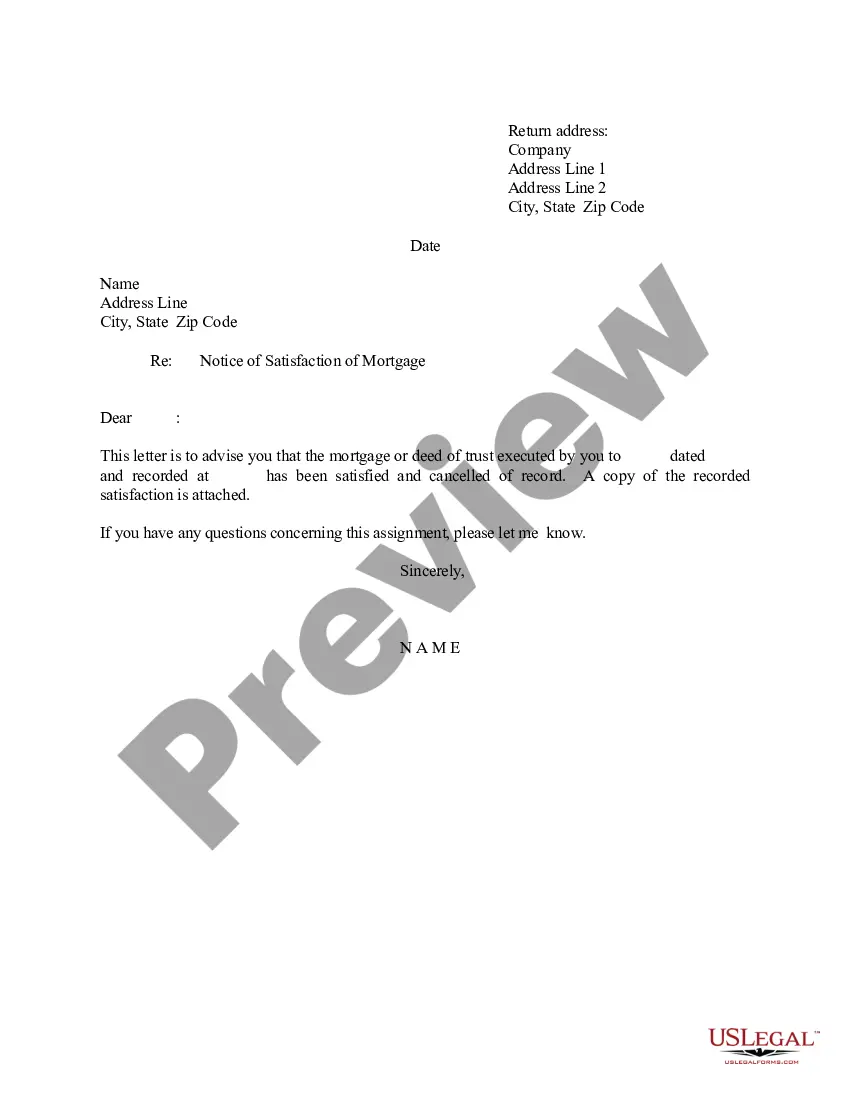

Escrow Seller Does Fortnite Have In Nevada

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Purpose: To protect the public from financial harm if the escrow agency commits fraud or engages in unfair business practices. Who Regulates Escrow Agencies in Nevada: The Nevada Department of Business and Industry, Division of Mortgage Lending.

Nevada's escrow process is similar to other states where an escrow agent, closing agent, or representative from a title company is used to complete the transaction.

Not every state requires an escrow account, but some municipalities require the accounts even when the states do not. States that don't require a separate escrow account often require landlords to place security deposits in a regulated financial institution.

Note: The escrow/impound account must include a two-month escrow cushion for all items with the exception of mortgage insurance, in which no cushion is to be established. Exceptions to the two-month cushion policy exist for properties located in the following states: Limited to one month: MT. Zero months: ND, NV.

Currently, the escrow states are: Alaska, Arizona, California, Hawaii, Idaho, Nevada, New Mexico, parts of Ohio, Oregon, Utah and Washington. States that structure closings differently. You and the seller are not required to be in the same location.

Title agents and escrow officers must be licensed in Nevada. Applicants must: 1) Be a Nevada resident (or reside within 50 miles of the state) and at least 18 years of age. 2) Complete pre-licensing education requirements at a state-approved school.

The specifics on who pays the transfer tax in Nevada are sometimes up for negotiation, but usually the seller is responsible.

Escrow fees are charged for the services of an escrow agent who acts as a neutral party in the transaction, holding and disbursing funds as needed. These fees are typically split between the buyer and seller, but the exact split can be a point of negotiation.