Change Deed Trust With Irs In San Antonio

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Print and mail the form. Then, mail the printed form to the IRS using the address provided in the instructions. It's essential to keep a copy of the filled form for your records. As of now, Form 8822 cannot be filed electronically.

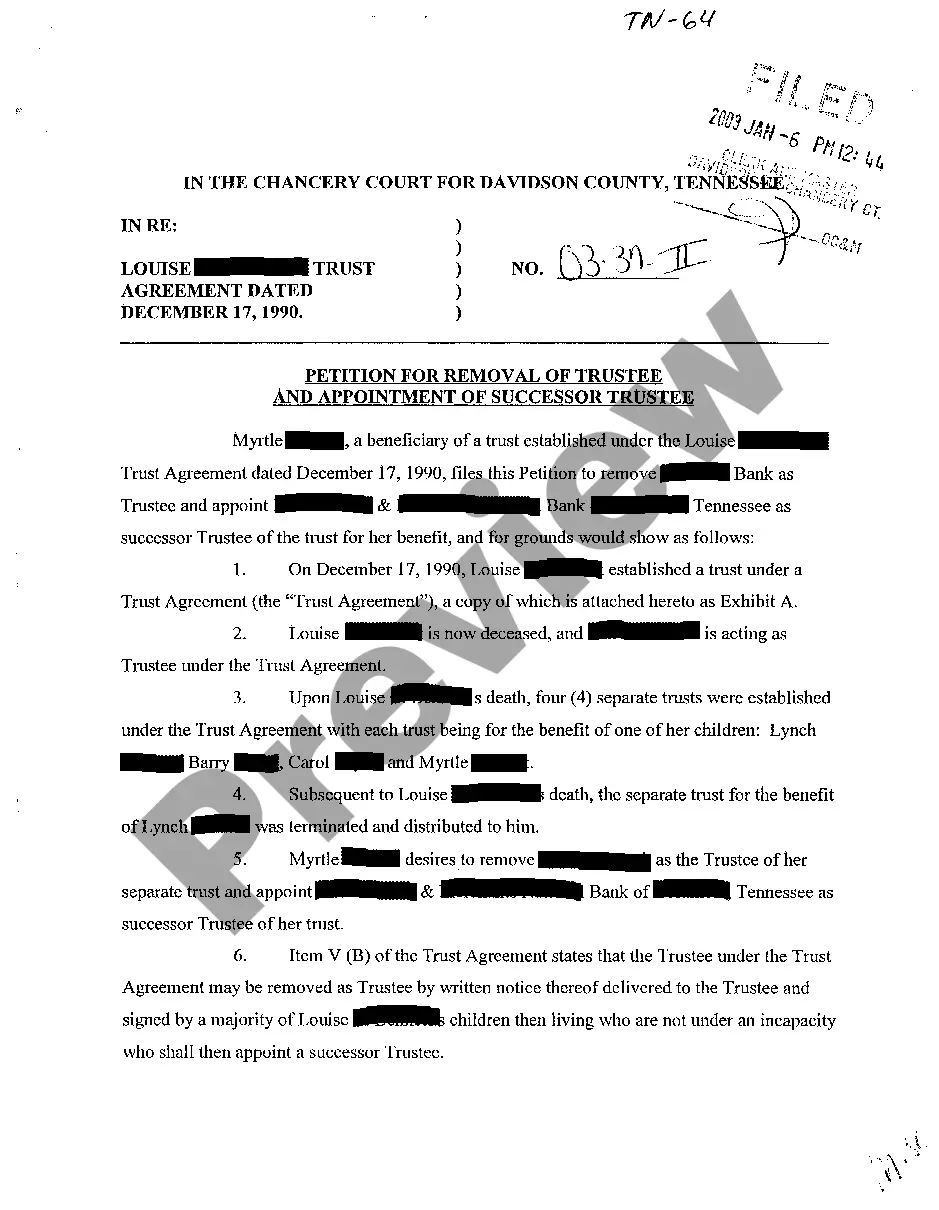

All beneficiaries must sign a written consent form to transfer assets from a trust that does not allow modifications. You will need to create the new trust first, then request the court to allow the asset transfer and the termination of the old trust.

All beneficiaries must sign a written consent form to transfer assets from a trust that does not allow modifications. You will need to create the new trust first, then request the court to allow the asset transfer and the termination of the old trust.

2 has made a major change in the way assets are treated within Irrevocable Trusts, namely concerning the provision for stepup in basis. The rule states that unless the asset in question is included in the taxable estate of the Grantor upon their death, then that asset will not receive the stepup in basis.

By form. To change your address with the IRS, you may complete a Form 8822, Change of Address (For Individual, Gift, Estate, or Generation-Skipping Transfer Tax Returns) and/or a Form 8822-B, Change of Address or Responsible Party — Business and send them to the address shown on the forms.

This transfer doesn't usually lead to an immediate tax obligation, meaning no tax is levied for merely changing the ownership. However, the trust, which now owns the stock, may become liable for taxes on dividends and capital gains from the stock.

A circular trust distribution exists where a trust (the first trust) makes a distribution to a second trust. Then all or part of that distribution goes back to the first trust as a distribution from either the second or another trust.

The fiduciary (or one of the joint fiduciaries) must file Form 1041 for a domestic trust taxable under section 641 that has: 1. Any taxable income for the tax year; 2. Gross income of $600 or more (regardless of taxable income);

You need to file IRS Form 56 if you take on a fiduciary role, such as an executor, administrator, trustee, guardian, or receiver. Here are some examples: Executor of an Estate: If you are handling the tax matters of a deceased person's estate, you must file Form 56.

How do I complete abatement form 843? Line 1 is the tax year the abatement is for. Line 2 is the total fees/penalties you are asking the IRS to remove. Line 3 is generally going to be Income (tax). Line 4 is the Internal Revenue Code section. Line 5a is the reason you are requesting the abatement.