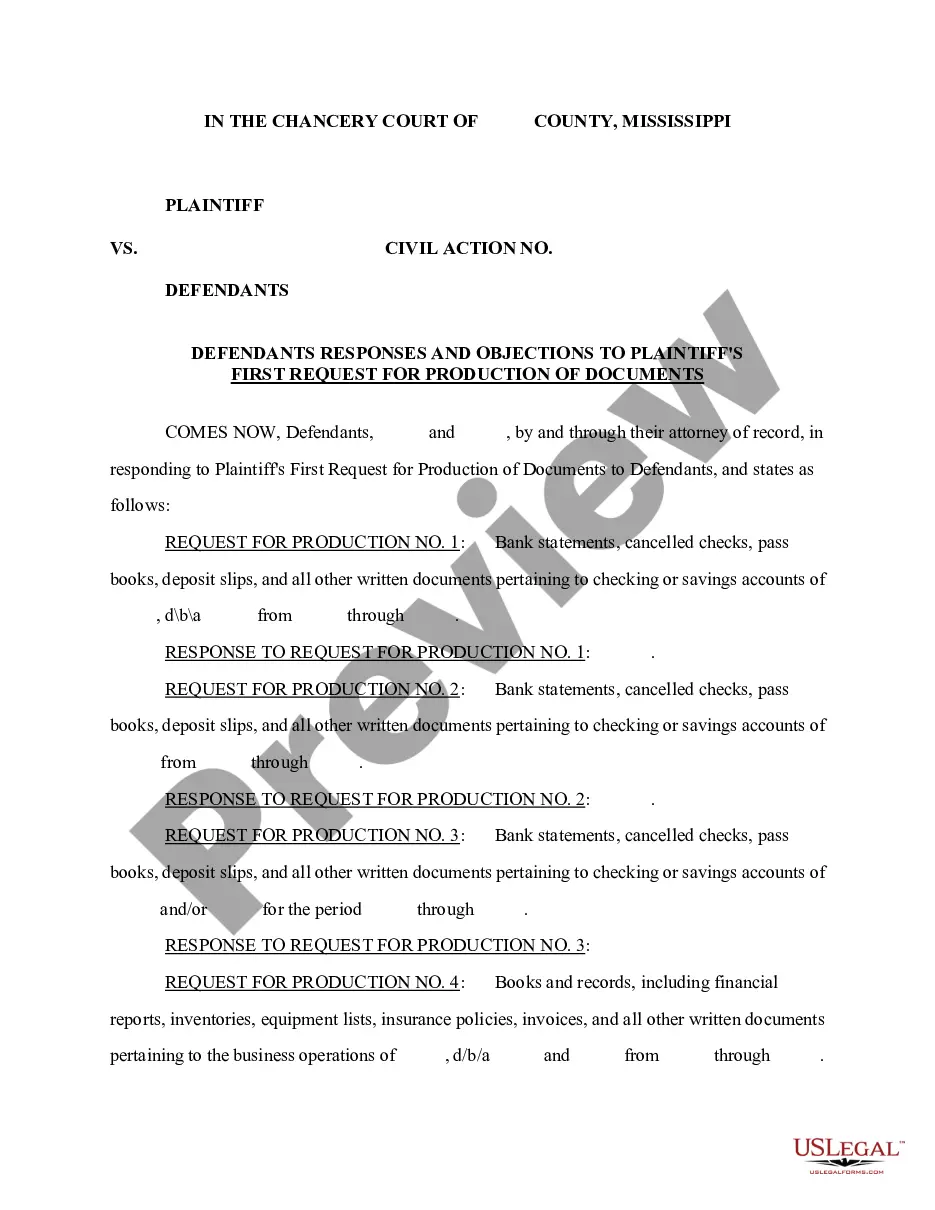

Secure Debt Shall Foreclose In Montgomery

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The right of redemption allows the original owner to redeem the property by paying off back taxes and/or liens against the property within one year of the date of the foreclosure sale. The redemption period for homestead property is 180 days.

Because this process can be complicated it is important to know what the process is and the timeline that you are afforded. Typically, the Alabama foreclosure process takes approximately 30 to 60 days.

No matter how far along the process is, right up until the day of foreclosure, it can be stopped by filing for bankruptcy. Mortgage companies often string people along, promising but not delivering help, until there is no time left.

A: Foreclosure is the method used by a lender (such as a bank or mortgage company) to take ownership and possession of the property used to collateralize your mortgage if you get behind in your payments. In Alabama, lenders do not have to sue you in court first in order to foreclose on your property.

Foreclosure is when a lender uses a legal process to force the sale of a property (like a home) to cover a debt. This can happen when someone takes out a mortgage to buy a home and then stops making payments (defaults on the mortgage).

In Alabama, lenders do not have to sue you in court first in order to foreclose on your property. Lenders do have to publish the foreclosure date in a local newspaper for three consecutive weeks prior to the foreclosure sale. You may also receive a letter from your lender advising you of their intentions.

Key Takeaways In general, a lender won't begin foreclosure until you've missed four consecutive mortgage payments. Timing can vary from lender to lender, as well as the state of the housing market at the time. Lenders generally prefer to avoid foreclosure because it is costly and time-consuming.

It benefits both the lender and the borrower. To initiate the process, the borrower will submit a loss mitigation application to their mortgage provider. If all goes well, the borrower will be relieved of their debts on the property, though this is not always the case. Sometimes, there will be a deficiency judgment.

Foreclosures can stay on your credit reports for up to seven years.

Another way to surrender your home is through a consent foreclosure. A consent foreclosure allows the homeowner to consent to a judgment of foreclosure being entered against him. In exchange for consenting to judgment, the creditor cannot begin deficiency judgment proceedings against the debtor.