Personal Property Business Form For Taxes In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Can I File My LLC and Personal Taxes Separately? Yes, if your LLC is considered a corporation, then these taxes can be filed separately from your personal taxes. If your LLC is not considered a corporation, the taxes are to be filed with your personal taxes.

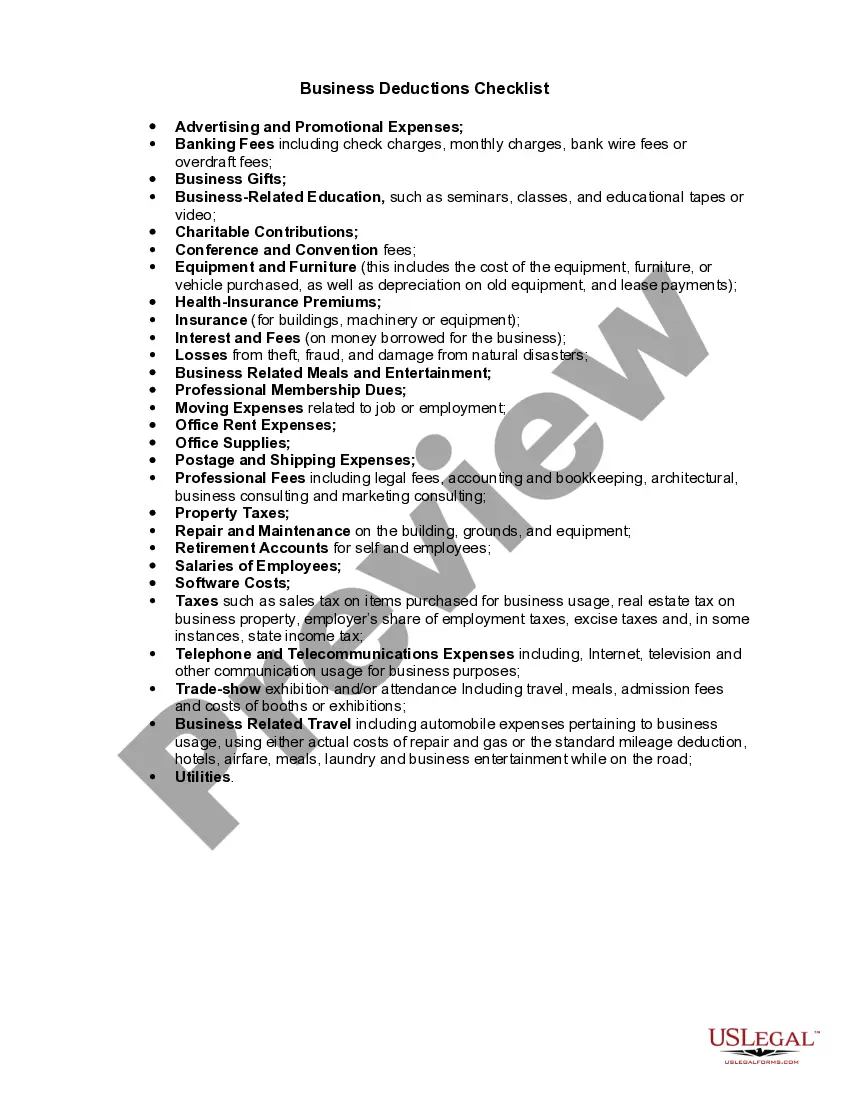

In addition to real estate, Indiana taxes all personal property. The taxpayer is responsible for reporting all tangible personal property that is used in their trade or business, used for the production of income, or held as an investment that should be or is subject to depreciation for federal income tax purposes.

You have to file an income tax return if your net earnings from self-employment were $400 or more. If your net earnings from self-employment were less than $400, you still have to file an income tax return if you meet any other filing requirement listed in the Form 1040 and 1040-SR instructions PDF.

Deductible personal property taxes are those based only on the value of personal property such as a boat or car. The tax must be charged to you on a yearly basis, even if it's collected more than once a year or less than once a year.

Include the income from the business on your Form 1040, U.S. Individual Income Tax Return and the appropriate schedule(s): Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship); Schedule E (Form 1040), Supplemental Income and Loss; and/or Schedule SE (Form 1040), Self-Employment Tax.

Include the income from the business on your Form 1040, U.S. Individual Income Tax Return and the appropriate schedule(s): Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship); Schedule E (Form 1040), Supplemental Income and Loss; and/or Schedule SE (Form 1040), Self-Employment Tax.

Business Personal Property Tax is a tax assessed on tangible personal property businesses own. This type of property includes equipment, furniture, computers, machinery, and inventory, among other items not permanently attached to a building or land.

The state of Georgia provides the following exemptions: All personal clothing and effects, household furniture, furnishings, equipment, appliances, and other personal property used within the home, if not held for sale, rental or other commercial use, shall be exempt from all ad valorem taxation.