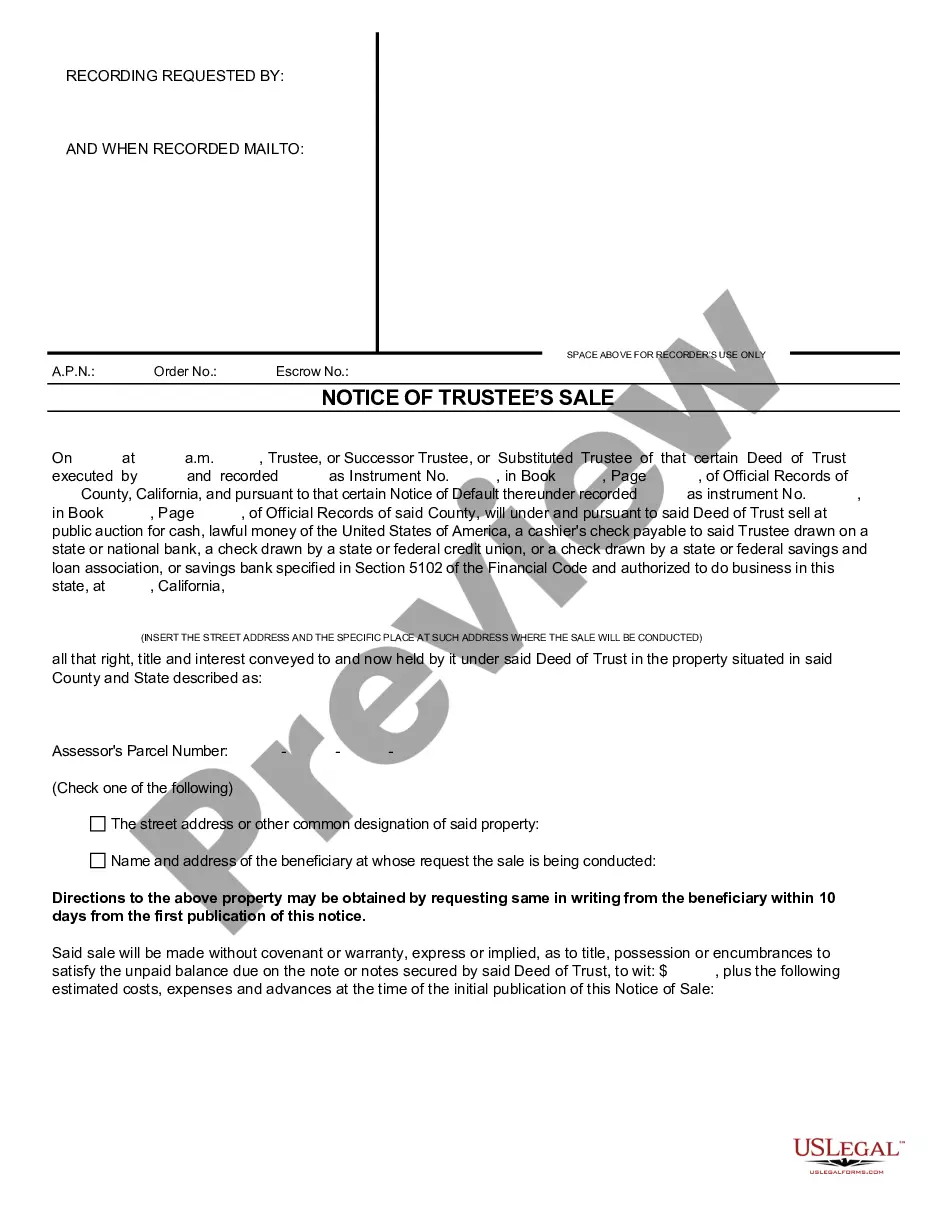

Chattel Mortgage Form With Extra Judicial Foreclosure In Bexar

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

What is the biggest differences between judicial foreclosure and strict foreclosure? that strict foreclosure does NOT involve a foreclosure sale.

Chattel is any tangible personal property that is movable. Examples of chattel are furniture, livestock, bedding, picture frames, and jewelry.

Judicial foreclosure is required in certain situations such as foreclosures involving home equity loans, reverse mortgages, or property owners' association assessments.

Deed in Lieu of Foreclosure Potential for Relocation Assistance: Sometimes, lenders may offer relocation assistance or additional time to stay in the home as part of the deal. Faster Resolution: The deed in lieu process is generally quicker than foreclosure, providing faster relief from mortgage obligations.

The former owner will have to petition the county to turn over the surplus funds. If no one petitions to recover them, the surplus funds generally can be held by the county for two years before they are distributed to the taxing bodies that foreclosed on the property.

Step 2: Notice of Sale or Order of Sale In a judicial foreclosure, once the court has issued their judgment granting the foreclosure, the clerk of the court will prepare an Order of Sale directing the sheriff or constable to sell the property at auction.

Loss in Ownership, Title, and Equity: The most obvious drawback of a deed in lieu is the loss of ownership, title, and equity in the property. A borrower will also lose any improvements that were done on the property, rental income, and other profits related to the property.

If the lender is pursuing a foreclosure outside court, you can challenge a non-judicial foreclosure by initiating a lawsuit to stop the process until a court reviews the foreclosure. A successful defense may take several different forms, ranging from procedural issues to substantive errors or abuses.

judicial foreclosure is when lenders foreclose property without getting a court order first. In a jurisdiction that passes a statute authorizing nonjudicial foreclosure, private parties must contract for a powerofsale clause in a mortgage or deed of trust to allow nonjudicial foreclosure.