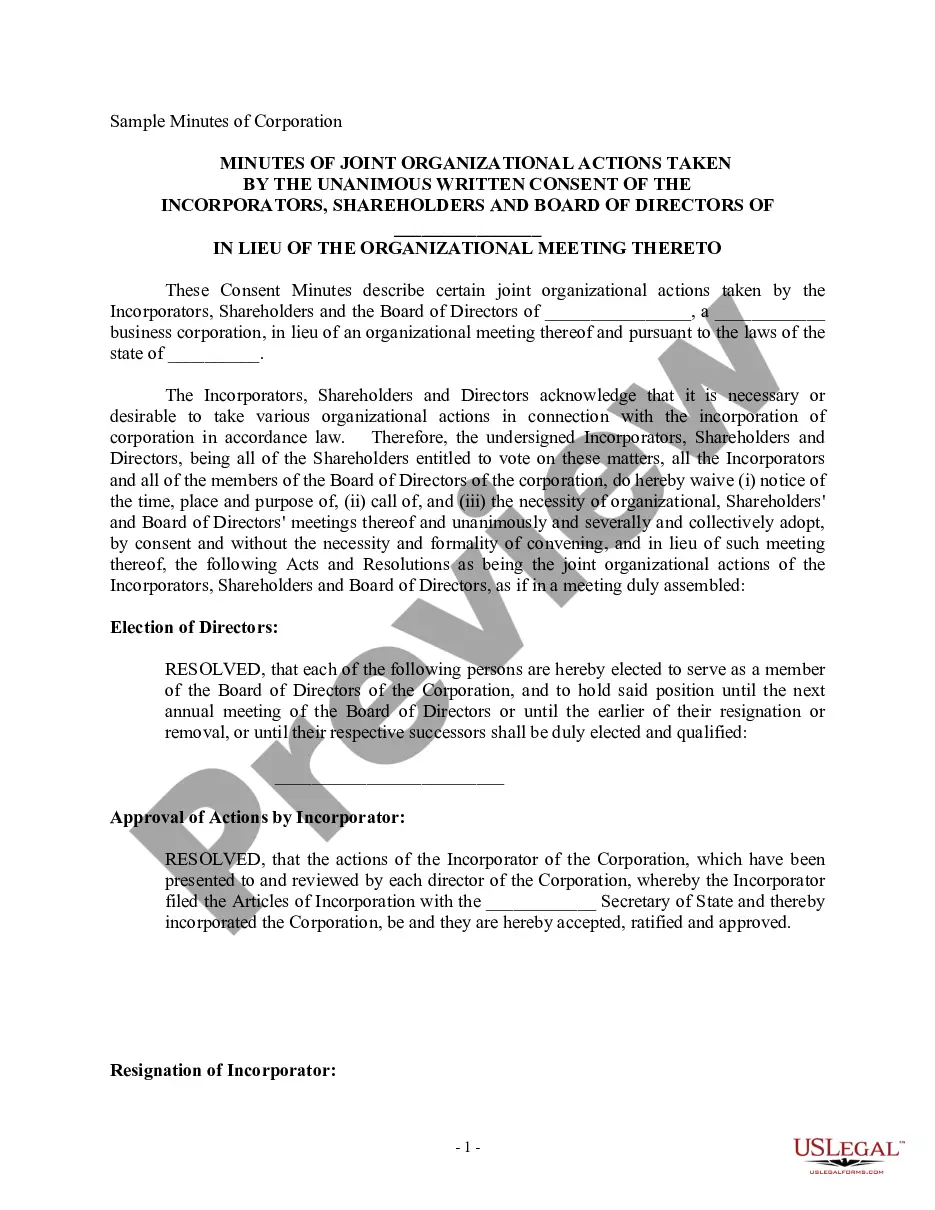

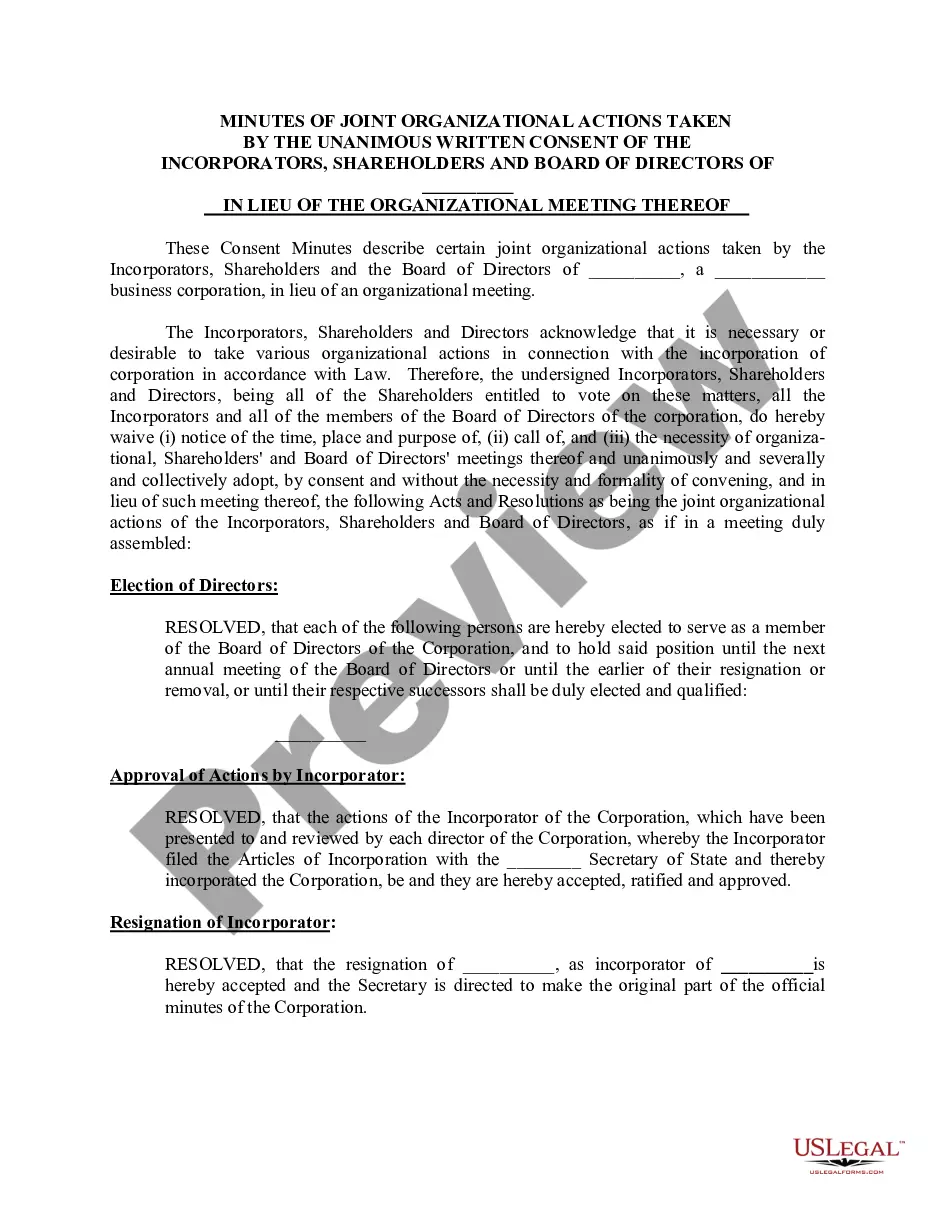

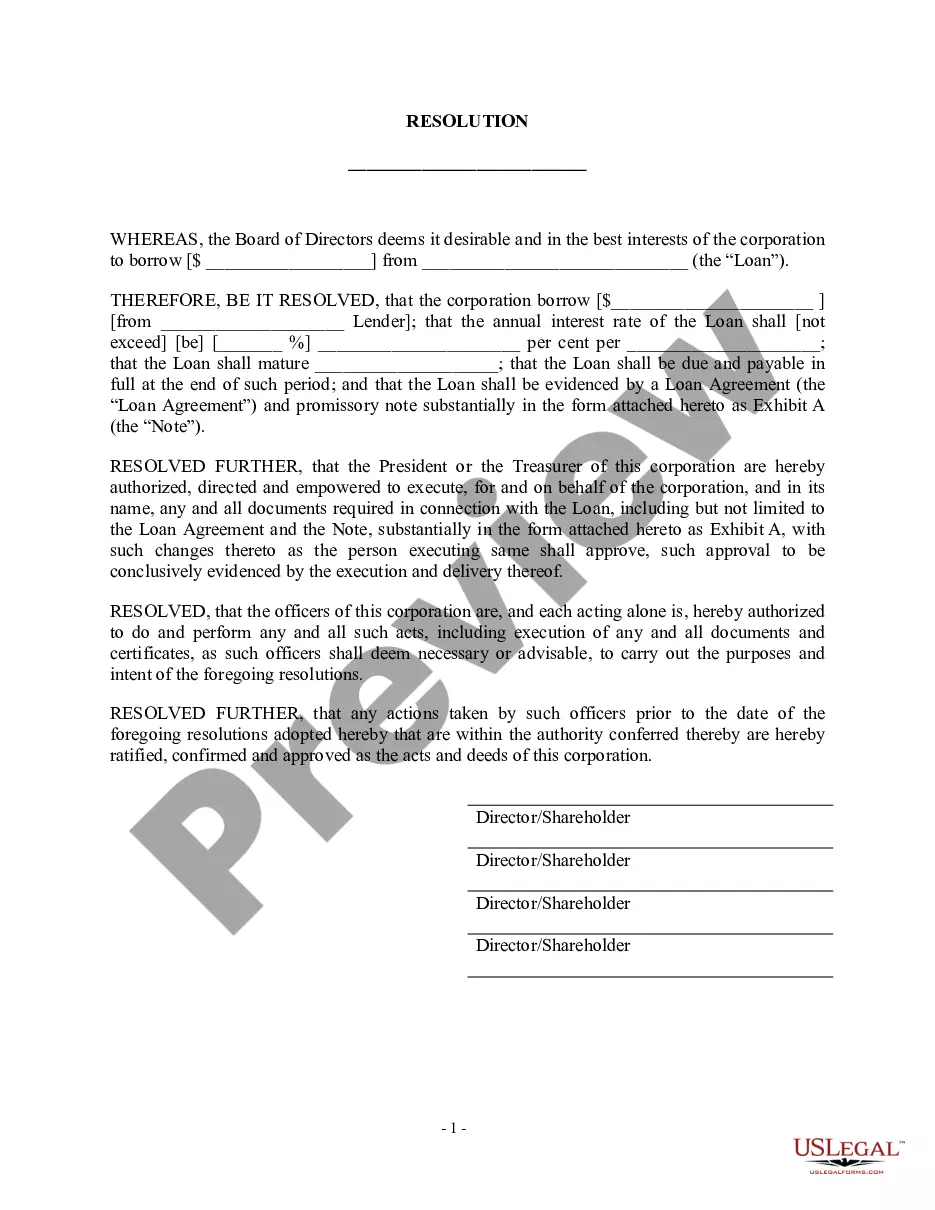

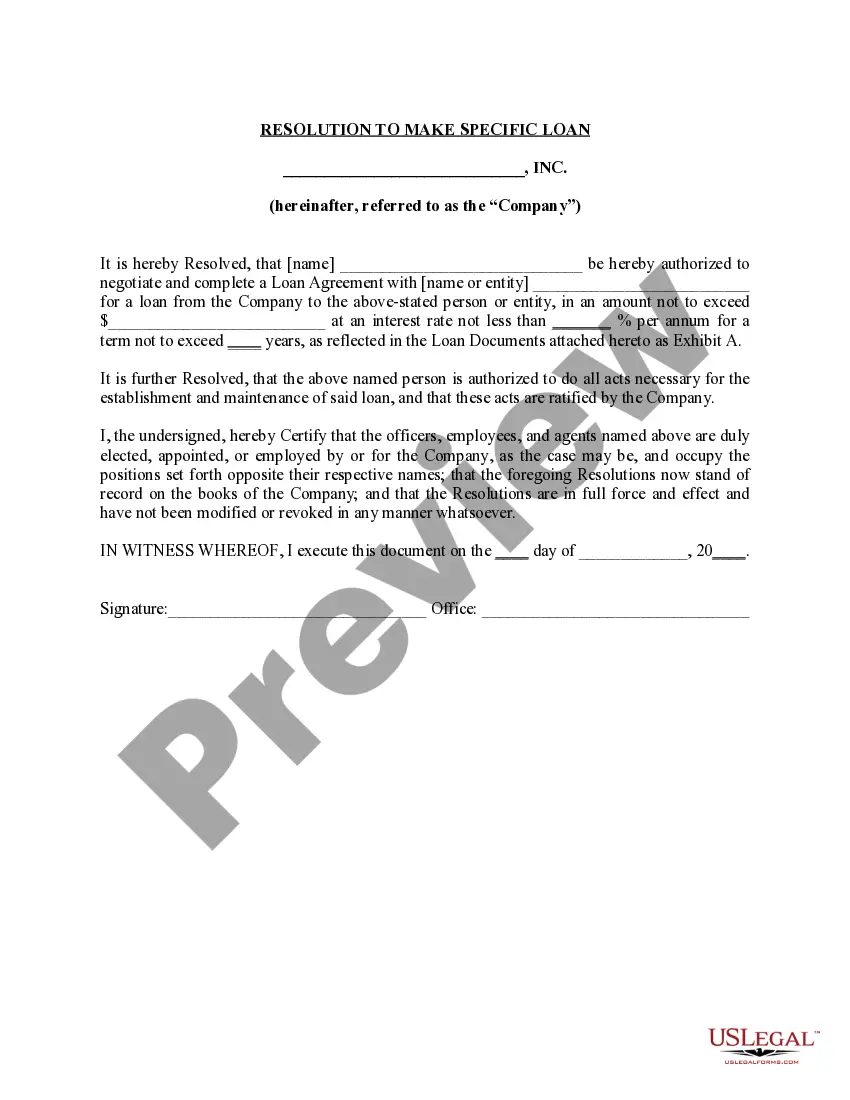

Borrowing For Commercial Property In Nassau

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Credit score: Your personal FICO Score and business credit report both play a role in determining your creditworthiness. Many lenders require a minimum credit score of 600 (or more) when you apply for a business line of credit, although having a higher score can help you secure a better interest rate.

Most small business lenders like to see a business credit score above 75, but local lenders may consider lower scores for small businesses or startups. Conventional consumer financing companies rarely make loans to individuals with credit scores below 500.

Transitioning from Residential to Commercial Apply for a special permit known as a zoning variance. Request rezoning. Keep the property as is.

Research local zoning laws - Look for zoning maps online and compare zoning trends. Switching a property from residential to commercial requires requesting a change of zone. This can only be done once it is proved that the switch would benefit the entire community.

Converting residential property into commercial property involves several key steps, including applying for change of use planning permission. This process ensures that the building is suitable for business purposes and that any alterations to the property are approved and legally compliant.

You typically have to get permission from the city to do this and that usually requires providing them with detailed plans and attending city planning meetings. Your property has to meet certain rules and standards to ensure it complies with commercial standards and building codes.

How much deposit do you need for a commercial mortgage? The amount of deposit you will need depends on several factors, but it will typically be between 20% and 40%.

A credit score for investors or businesses should be above 660 for both commercial and multifamily loans. Certain loans and alternative financing strategies can serve as workarounds in commercial real estate financing. However, this is uncommon.