Loan Participation Agreement Template With Balloon Payment In Collin

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

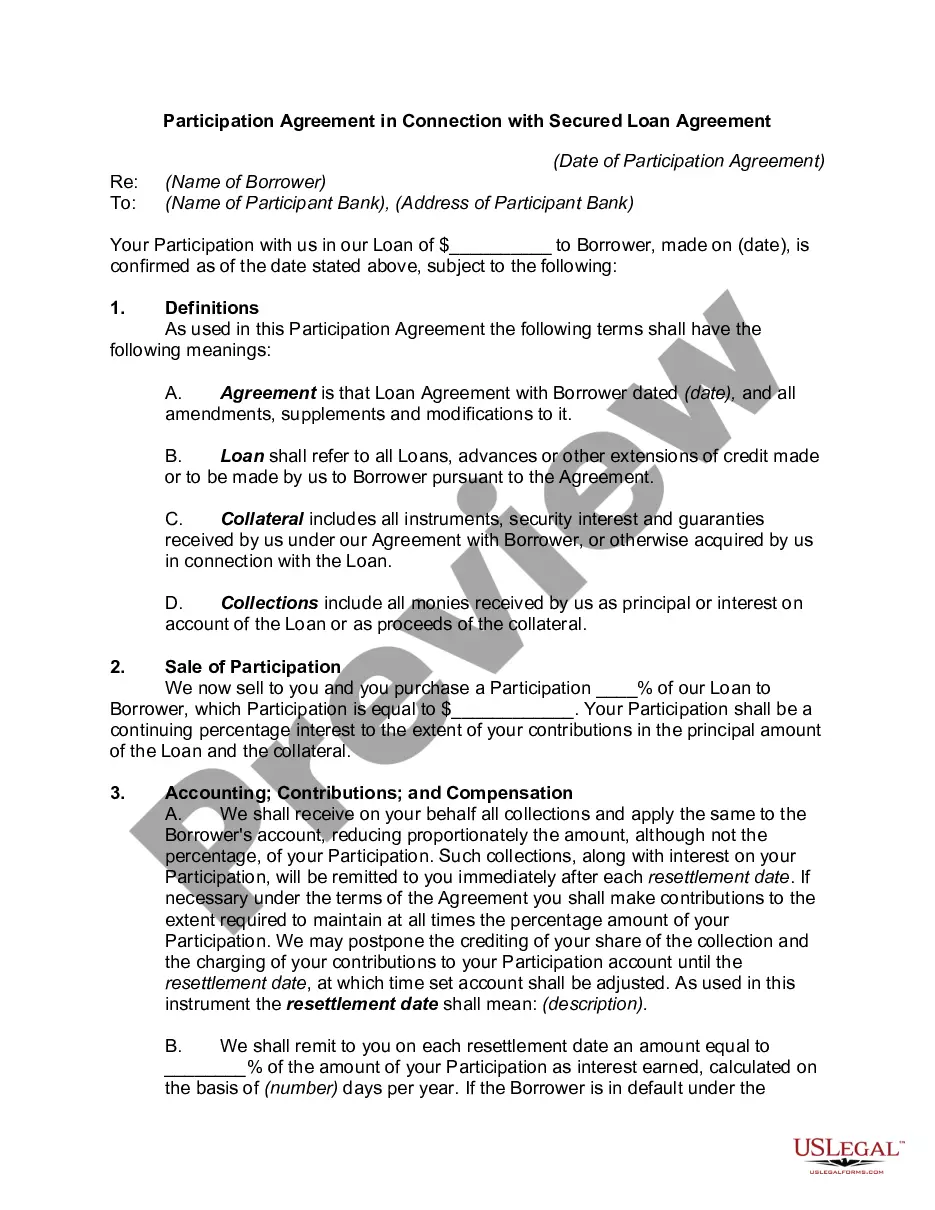

With participations, the contractual relationship runs from the borrower to the lead bank and from the lead bank to the participants, whereas with syndications, the financing is provided by each member of the syndicate to the borrower pursuant to a common negotiated agreement with each member of syndicate having a ...

However, the larger balloon payment at the end represents a substantial financial obligation that needs to be carefully planned and managed. Accounting Treatment: The balloon payment is usually recorded as a liability in the financial statements until it becomes due.

The Tax Administration proceeds to recharacterize the related-party profit participating loans into a ordinary senior loans: only «fixed» interest is considered tax deductible and variable interest is reclassified as dividends.