Form Assignment Accounts Receivable With Credit Card Payments In Mecklenburg

Description

Form popularity

FAQ

Follow these steps to calculate accounts receivable: Add up all charges. You'll want to add up all the amounts that customers owe the company for products and services that the company has already delivered to the customer. Find the average. Calculate net credit sales. Divide net credit sales by average accounts receivable.

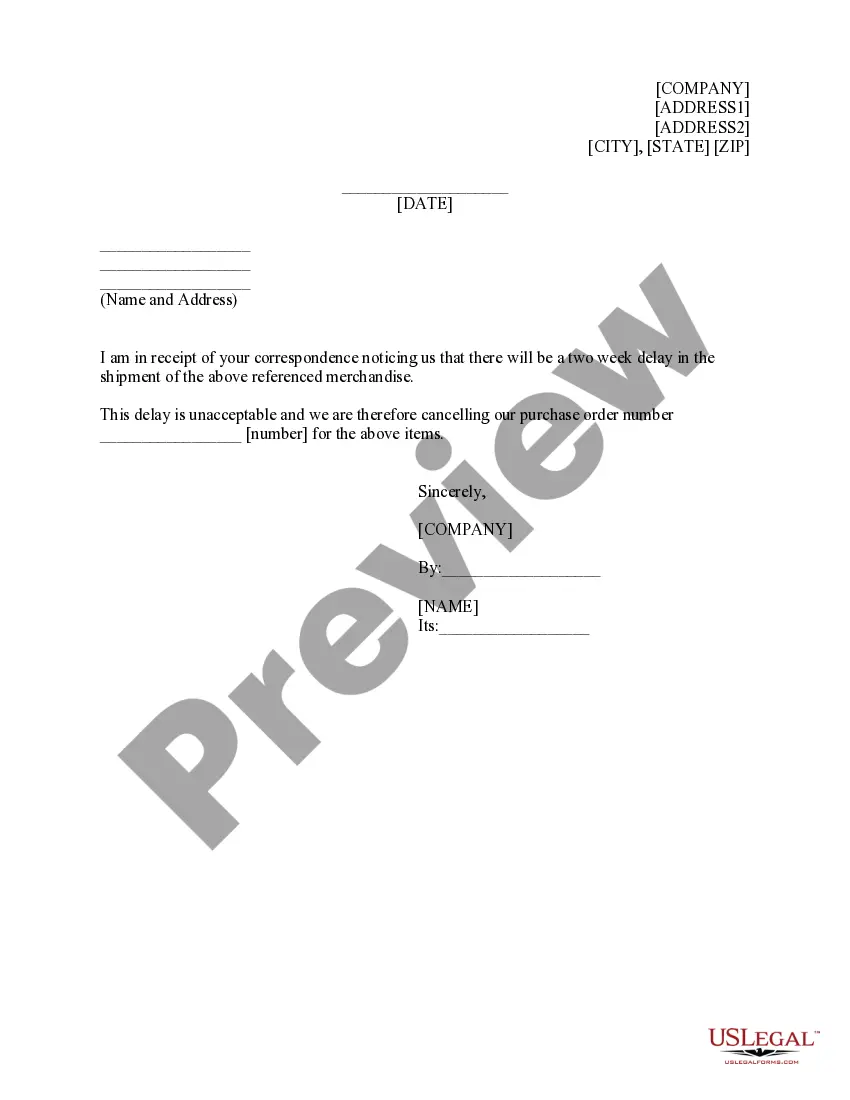

All DoD guidance and regulations indicate that sales of merchandise or services to an authorized customer using a credit card should be recorded as a receivable.

With factoring, the factor takes control of bill collection and assumes the credit risk for customer non-payment. In contrast, with the assignment of receivables, the business retains control of its customer relationships and the collection process, bearing all of the credit risk.

Assignment of accounts receivable is a method of debt financing whereby the lender takes over the borrowing company's receivables. This form of alternative financing is often seen as less desirable, as it can be quite costly to the borrower, with APRs as high as 100% annualized.

Credit Card Payments Use your actual bank account as the Checkbook (the account the payment comes from). Place your liability account under the GL Account column (the account the payment is applied to). Check the box to Automatically Import these items.

Credit Cards as Liabilities The balance owed on a credit card can be treated either as a negative asset, known as a “contra” asset, or as a liability. In this article we'll explore the optional method of using liability accounts, however, there are several advantages to using the Contra Asset Approach.

In QuickBooks, a credit card payment is treated as a liability payment, as it reduces your outstanding credit card balance. It is not considered a direct business expense, but rather the repayment of funds that were borrowed to cover business expenses.

In QuickBooks, a credit card payment is treated as a liability payment, as it reduces your outstanding credit card balance. It is not considered a direct business expense, but rather the repayment of funds that were borrowed to cover business expenses.