Limited Companies

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

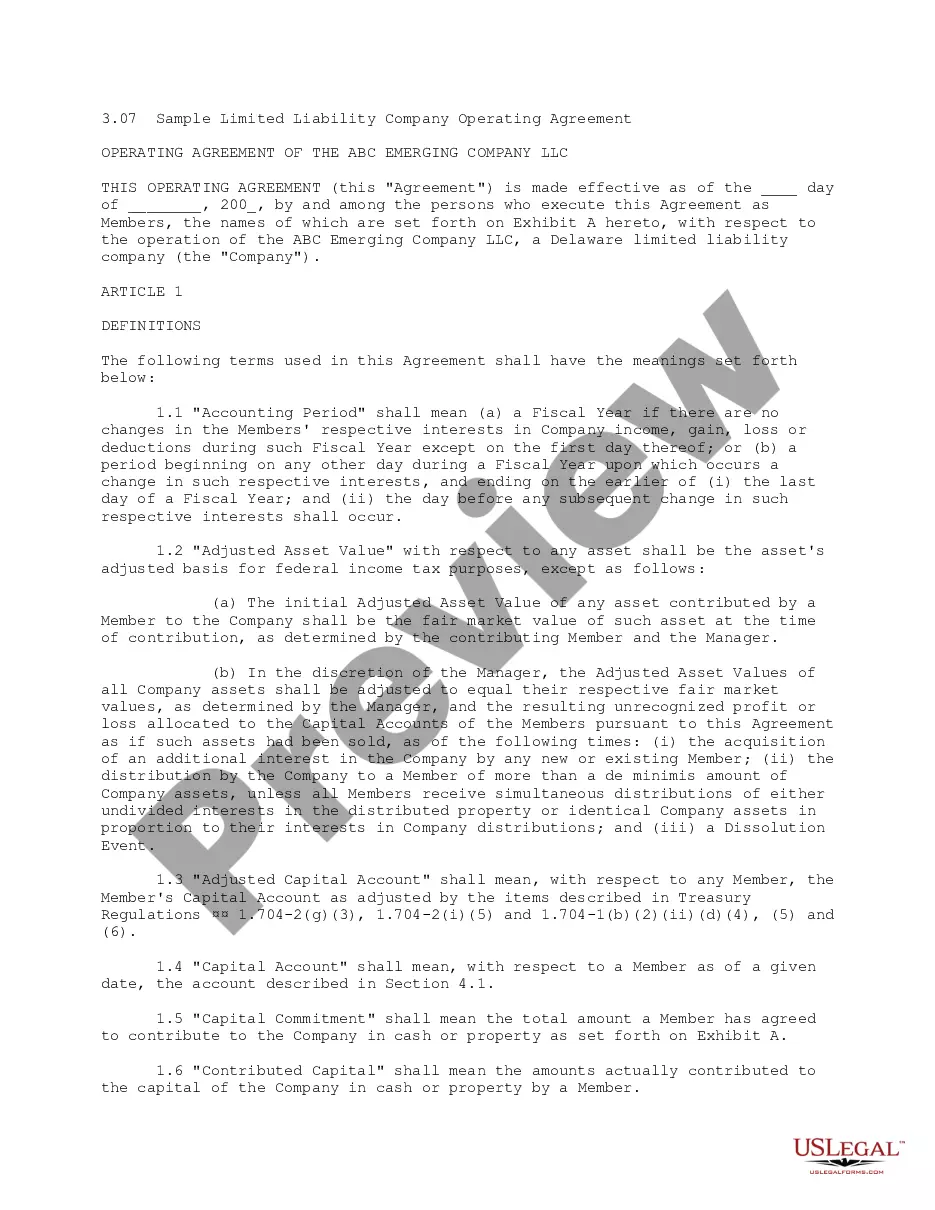

How to fill out North Carolina Limited Liability Company LLC Operating Agreement?

- If you have previously used US Legal Forms, log in to your account to download the required form template. Ensure your subscription is active; otherwise, renew it.

- If this is your first visit, begin by checking the Preview mode and form descriptions to find the right document that meets your requirements and aligns with your local jurisdiction.

- If necessary, utilize the Search tab to refine your search for other relevant templates that may better suit your needs.

- Once you've identified the appropriate document, click on the Buy Now button and select your desired subscription plan. You will need to set up an account for full access.

- Complete your purchase by entering your credit card information or using your PayPal account for payment.

- Finally, download your chosen form and save it to your device. You can also access it under the My documents section of your profile whenever needed.

By following these straightforward steps, you can efficiently secure the legal documents needed for your limited company.

With US Legal Forms, you gain access to a comprehensive library and expert assistance, ensuring your documents are both precise and legally compliant. Don't hesitate to start your journey today!

Form popularity

FAQ

A limited company must file specific documents with the IRS and state authorities to maintain its good standing. This includes annual reports, tax returns, and, depending on your classification, forms like 1120 for C corporations or 1120-S for S corporations. Additionally, adhering to filing deadlines is crucial to avoid penalties. The uslegalforms platform can provide templates and guidance to ensure you complete these requirements accurately and on time.

Deciding between an S corporation and a C corporation for your startup involves considering your business goals and funding strategies. Limited companies that plan to attract investors may prefer C corporation status due to its flexibility in issuing various classes of stock. On the other hand, if you want to pass corporate income directly to shareholders to avoid double taxation, an S corporation might be better suited. Carefully evaluating your business needs, in consultation with professionals, is crucial for this decision.

To find out whether your LLC is designated as an S corp or a C corp, you can review your IRS tax filings or look for previous correspondence regarding your tax election status. If you haven’t chosen an S corporation election, your LLC is treated as a C corporation by default. It’s essential to regularly check your tax status, as this can affect your financial responsibilities and business planning. Using services like uslegalforms can simplify your review process.

To determine if your LLC is classified as a C corporation or an S corporation, check the IRS filings associated with your company. If you filed form 2553 and received approval, your LLC is taxed as an S corporation; otherwise, it defaults to C corporation taxation. Additionally, you can consult the documentation submitted at the time of formation or contact a tax professional for guidance. Understanding this classification allows you to better strategize your tax obligations.

Limited companies, specifically LLCs, can elect to be taxed as either a C corporation or an S corporation, but they are not inherently classified as either. By default, an LLC is a pass-through entity, meaning profits and losses pass directly to the owners. If you want your LLC to be taxed as an S corporation, you must file form 2553 with the IRS. This flexible approach allows you to choose the tax treatment that fits your business best.

Choosing to operate as a limited company can be a wise decision for many entrepreneurs. This structure offers significant protection of personal assets from business liabilities, enhancing financial security. Additionally, forming a limited company can provide a more professional image, potentially attracting more clients and investment opportunities. Evaluating your specific circumstances will help determine if this option suits your business goals.

Limited companies face several disadvantages, including higher administrative costs and complexity in compliance. This structure requires regular financial reporting and formalities that can burden small businesses. Additionally, some owners may feel constrained by the need to disclose financial information to regulators and the public. However, these drawbacks should be measured against the benefits of limited liability protection.

A limited company is characterized by having a distinct legal status that limits the liability of its owners. In this structure, the owners share the business's profits and responsibilities based on their investment. Limited companies typically must register with the state and file annual financial reports, demonstrating their compliance with existing regulations. This protects personal assets from business liabilities, making it a popular choice.

One disadvantage of a limited company is the restriction on financial flexibility. Limited companies must adhere to strict financial reporting and accounting regulations, which can consume valuable resources. Furthermore, raising capital may require significant disclosure of company information, deterring potential investors. Nonetheless, this structure provides essential protections, balancing the trade-offs.

The primary difference between Ltd and LLC lies in their formation and structure. A Limited (Ltd) company is more common in the UK and has shareholders, while a Limited Liability Company (LLC) is popular in the US and offers flexibility in management. Both types provide limited liability protection, yet the regulations governing them differ by jurisdiction. Understanding these differences helps you choose the right structure for your business.