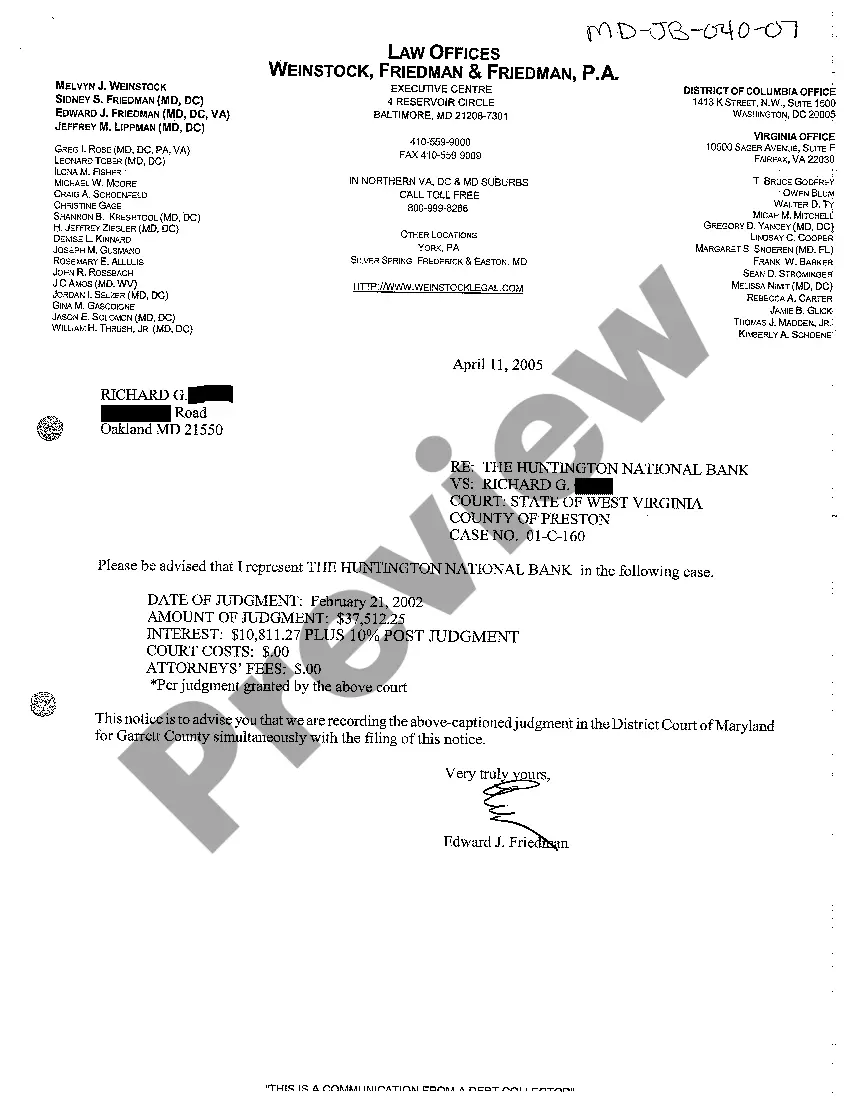

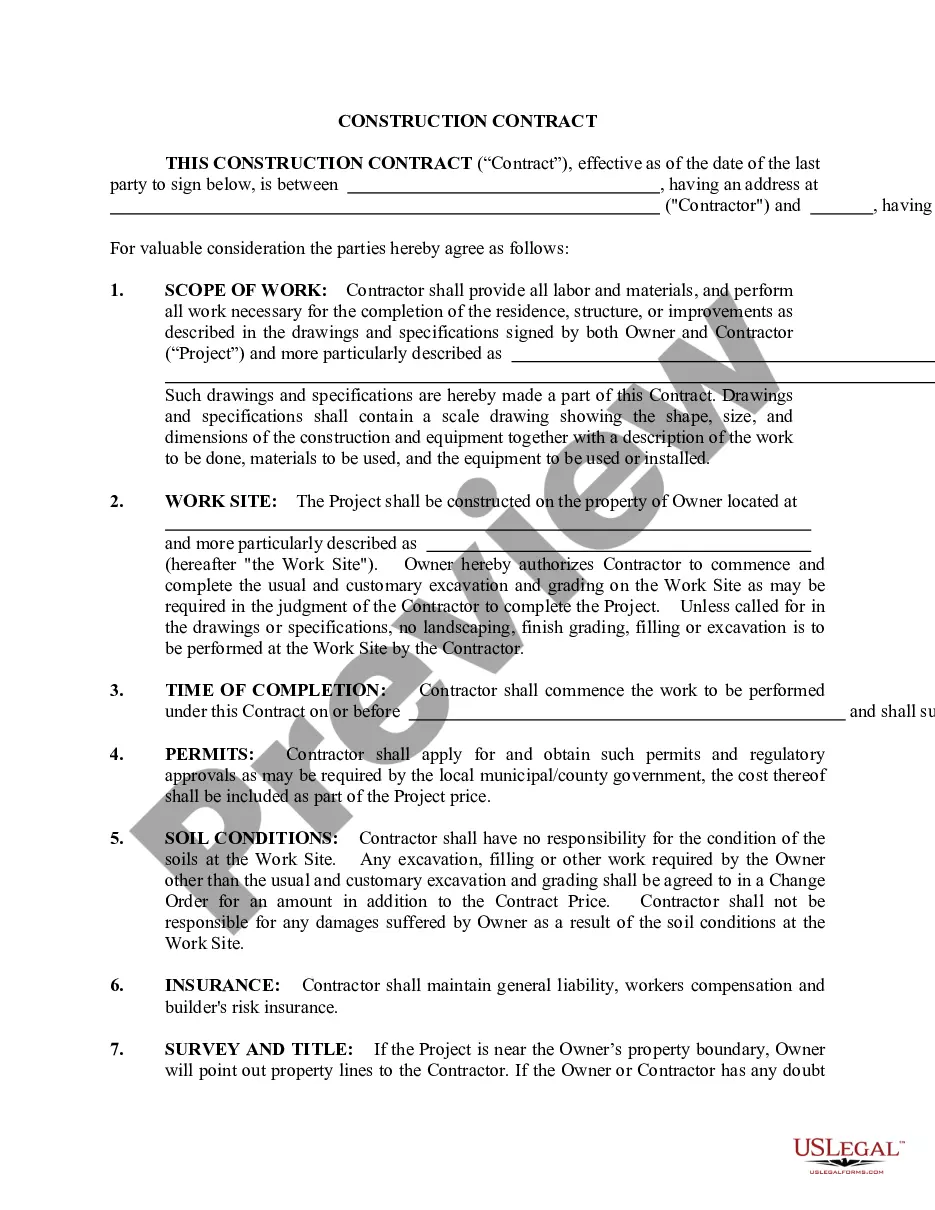

Assignment Mortgage After Foreclosure Filed

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Arkansas Assignment Of Mortgage Package?

How to locate professional legal documents that adhere to your state regulations and complete the Assignment Mortgage Following Foreclosure Filed without consulting an attorney.

Numerous online services offer templates to address diverse legal situations and formal procedures.

However, it may take a while to determine which of the available samples meet both your use case and legal standards.

Should you not possess an account with US Legal Forms, follow the instructions below: Review the webpage you've accessed to confirm if the form meets your requirements.

- US Legal Forms is a trustworthy platform that assists you in finding official papers crafted according to the latest updates in state law while saving costs on legal support.

- US Legal Forms is not just a typical online directory; it comprises over 85,000 validated templates for various business and personal circumstances.

- All documents are categorized by area and state to facilitate a quicker and more efficient search process.

- Moreover, it integrates with advanced tools for PDF modification and eSignature, allowing users with a Premium subscription to easily complete their paperwork online.

- Minimal effort and time are required to acquire the needed documentation.

- If you have an account already, Log In and verify that your subscription is active.

- Download the Assignment Mortgage Following Foreclosure Filed using the appropriate button adjacent to the file name.

Form popularity

FAQ

Missing one to three mortgage payments can trigger the foreclosure process based on lender policies. Generally, a lender may consider initiating foreclosure after the borrower is three months behind. It's advisable to contact your lender as soon as you foresee payment issues, particularly to discuss options like the assignment mortgage after foreclosure filed, which can provide pathways for resolution.

The 37-day foreclosure rule is specific to lender actions after a borrower defaults on payments. This time frame often involves critical communications regarding the trustee's sale and the need to prepare for potential eviction. Understanding this rule can aid homeowners in strategizing their options, including navigating the assignment mortgage after foreclosure filed effectively.

Foreclosure actions typically unfold in five essential stages. Initially, the lender sends a notice of default, followed by a period for the borrower to remedy the situation. After this, the property may enter the court system if the borrower cannot resolve the defaults. Then, an auction occurs where the home may be sold. Finally, if necessary, there can be a post-foreclosure phase addressing the assignment mortgage after foreclosure filed.

In certain situations, exceptions to the 120-day foreclosure rule can apply. When a borrower does not occupy the home as their primary residence, the rule may not apply. Additionally, properties that fall under specific government programs often have different timelines. It's important to understand these exceptions, especially when considering the assignment mortgage after foreclosure filed process.

A foreclosure can remain on your credit report for up to seven years. Although this may feel daunting, there are strategies to improve your credit score in the meantime. Taking proactive steps, like seeking an assignment mortgage after foreclosure filed, can help rebuild your financial profile and enhance your chances of securing better financing in the future.

You may qualify for a new mortgage as soon as two years after a foreclosure, depending on certain conditions. Lenders may offer various programs that cater to your unique needs during this recovery phase. Exploring options like an assignment mortgage after foreclosure filed can assist you in regaining financial stability sooner.

After a foreclosure filed, you typically can apply for another mortgage within two to seven years, depending on the lender's guidelines and your financial situation. It is crucial to demonstrate improved credit and financial stability during this period. Many borrowers explore options like an assignment mortgage after foreclosure filed to rebuild their financial future.

Yes, a mortgage company can pursue you for remaining debt after foreclosure. If the sale of your property does not cover the full mortgage balance, they might seek collection of that deficiency. Understanding your rights in this matter is crucial, especially related to the assignment mortgage after foreclosure filed. Consulting with an expert can help clarify your situation and options.

Completing an assignment of mortgage involves transferring the original lender’s interest to another entity. You must prepare a written document detailing the terms of the assignment, sign it, and have it notarized. Additionally, this document should be filed with your local land records office. If you find this process overwhelming, uslegalforms offers resources that guide you through the assignment mortgage after foreclosure filed efficiently.

Obtaining a mortgage after foreclosure typically requires a waiting period of three to seven years, depending on the lender and circumstances. During this time, it’s essential to rebuild your credit and demonstrate financial stability. Many people successfully secure loans again, especially when they understand the process of assignment mortgage after foreclosure filed. Patience and preparation are key.