The FACTA Red Flags Rule: A Primer

Description

Key Concepts & Definitions

The FACTA Red Flags Rule: This rule, enacted as part of the Fair and Accurate Credit Transactions Act (FACTA), mandates that certain financial institutions and creditors develop and implement a written Identity Theft Prevention Program. The program is designed to detect, prevent, and mitigate identity theft in connection with account openings and existing accounts.

Step-by-Step Guide to Implementing the FACTA Red Flags Rule

- Identify Relevant Red Flags: Review and incorporate relevant patterns, practices, and specific forms of activity that are indicators of possible identity theft.

- Create Detection Procedures: Establish procedures that will be used to detect the red flags you've identified as relevant to your institution.

- Prevent and Mitigate Identity Theft: Outline actions you will take upon the detection of a red flag to prevent and mitigate identity theft.

- Update the Program: The program must reflect changes in risks to customers or to the safety and soundness of the creditor or financial institution from identity theft. Keep it updated regularly.

Risk Analysis

Implementing an insufficient program can result in legal penalties, loss of customer trust, and financial losses. Proactive engagement with fraud prevention, data security, and theft prevention strategies will minimize these risks effectively.

Common Mistakes & How to Avoid Them

- Lacking Customization: Failing to tailor the program to the specific needs and risks of your institution. Avoid this by conducting thorough risk assessments specific to your entity.

- Underestimating Threats: Overlooking new forms of identity theft. Stay informed with the latest security practices and update your program accordingly.

- Poor Training: Not training staff adequately on the identity theft prevention program. Ensure all relevant employees understand their roles in implementing the program.

Best Practices

- Maintain Comprehensive Records: Keep detailed records of identified red flags and actions taken in response to them.

- Secure Communication: Use secure email practices for all sensitive or personal information exchanged within and outside the organization.

- Customer Communication: Education about fraud prevention and identity theft risks is crucial for customer protection. Inform them about the signs of identity theft and what steps your entity has taken to protect their information.

How to fill out The FACTA Red Flags Rule: A Primer?

When it comes to drafting a legal document, it’s easier to delegate it to the specialists. However, that doesn't mean you yourself can not find a sample to utilize. That doesn't mean you yourself can not get a template to utilize, nevertheless. Download The FACTA Red Flags Rule: A Primer from the US Legal Forms web site. It gives you numerous professionally drafted and lawyer-approved forms and samples.

For full access to 85,000 legal and tax forms, users simply have to sign up and choose a subscription. When you’re registered with an account, log in, look for a particular document template, and save it to My Forms or download it to your gadget.

To make things less difficult, we have incorporated an 8-step how-to guide for finding and downloading The FACTA Red Flags Rule: A Primer fast:

- Make sure the form meets all the necessary state requirements.

- If available preview it and read the description before purchasing it.

- Hit Buy Now.

- Choose the suitable subscription for your needs.

- Make your account.

- Pay via PayPal or by credit/visa or mastercard.

- Select a needed format if a number of options are available (e.g., PDF or Word).

- Download the file.

Once the The FACTA Red Flags Rule: A Primer is downloaded you are able to complete, print and sign it in any editor or by hand. Get professionally drafted state-relevant documents in a matter of seconds in a preferable format with US Legal Forms!

Form popularity

FAQ

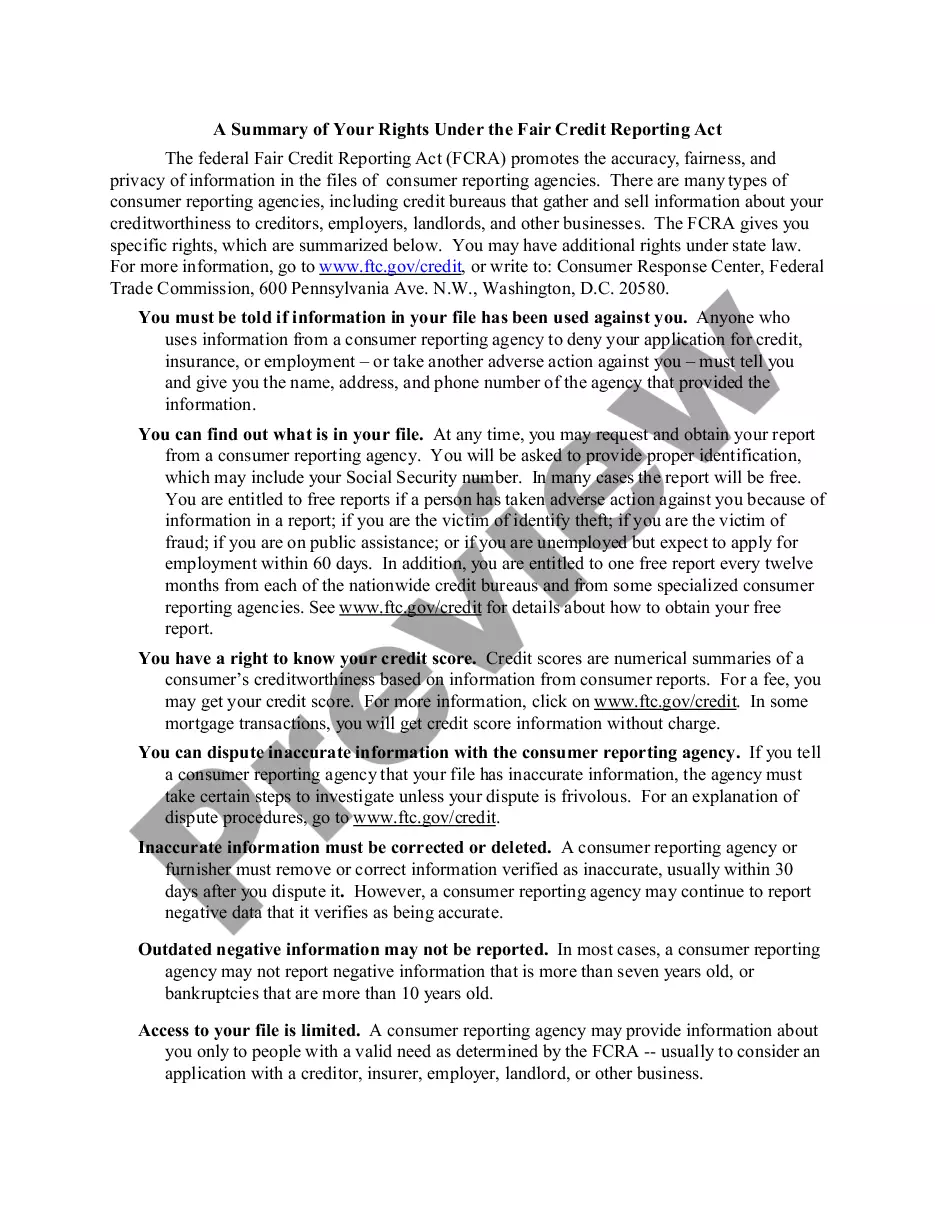

The Fair and Accurate Credit Transaction Act (FACTA) is an amendment to the Fair Credit Reporting Act (FCRA) and includes the Red Flags Rule, implemented in 2008. The Red Flags Rule calls for financial institutions and creditors to implement red flags to detect and prevent against identity theft.

Red Flag Requirements Initial Risk Assessment Policies and Procedures Manual Train Staff on Program Implementation New Account Authentication. (All consumer accounts) Validate Change of Address Requests. (All consumer accounts) Anti-Phishing Program Identity Theft Protection. (All consumer accounts)

1) Identify Relevant Red Flags. 2) Detect Red Flags. 3) Prevent and Mitigate Identity Theft. 4) Update Program.

The Red Flags Rule requires organizations to implement a written identity theft prevention program to help them identify any of the relevant red flags that indicate identity theft in daily operations. The Rule also offers steps to help prevent the crime and to mitigate its damage.

The Red Flags Rule (RFR) is a set of United States federal regulations that require certain businesses and organizations to develop and implement documented plans to protect consumers from identity theft.A creditor is any business or organization that regularly provides goods or services and bill customers later.

The Red Flags Program helps organizations plan, develop, implement and administer an identity theft prevention program to ensure compliance.Red Flags present as suspicious patterns or specific practices that provide clues that there may be identity fraud activity.

1 The Red Flags Rule was issued in 2007 under Section 114 of the Fair and Accurate Credit Transaction Act of 2003 (FACT Act), Pub. L. 108-159, amending the Fair Credit Reporting Act (FCRA), 15 U.S.C. ' 1681m(e).

Red Flags Rule and Identity Theft Prevention Program The Red Flags Rule requires financial institutions (and some other organizations) to establish and implement a written Identity Theft Prevention Program (ITPP) designed to detect, prevent and mitigate identity theft in connection with their covered accounts.

The Red Flags Rule requires that each "financial institution" or "creditor"which includes most securities firmsimplement a written program to detect, prevent and mitigate identity theft in connection with the opening or maintenance of "covered accounts." These include consumer accounts that permit multiple payments