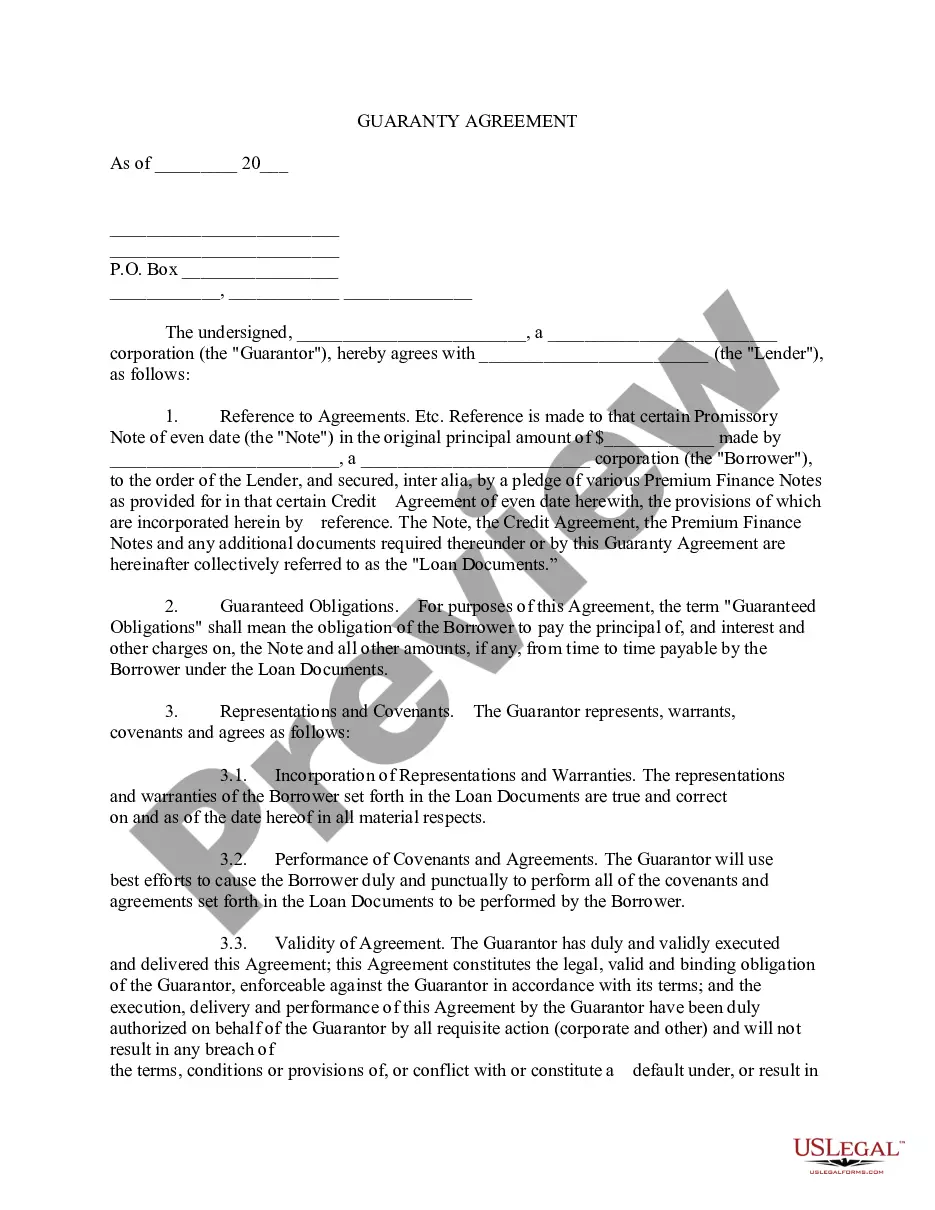

Loan Guaranty Agreement

What this document covers

The Loan Guaranty Agreement is a legal document in which a guarantor agrees to cover the debts and obligations of a borrower if they default on their loan. This form is essential for lenders as it provides an additional layer of security. Unlike other loan agreements, this specific agreement obligates the guarantor to assume responsibility for repayment under various conditions, making it a vital tool for businesses and lenders seeking assurance from third parties.

Key parts of this document

- Details of all parties involved, including the borrower (Makers) and guarantor.

- Terms of the loan, including the principal amount and any modifications.

- Clauses outlining the guarantor's liabilities and obligations.

- Conditions under which the guarantor remains liable even if circumstances change.

- Signature and notarization requirements to validate the agreement.

Situations where this form applies

This form is typically used when a lender requires additional security for a loan. It is particularly useful in scenarios where the borrower may lack sufficient credit history or collateral. By involving a guarantor, lenders can mitigate risks associated with potential defaults. Use this form when seeking to formalize the role of a guarantor in other loan agreements or when amending existing loan documents to include such provisions.

Who should use this form

- Lenders seeking additional assurance regarding loan repayment.

- Borrowers who might need a guarantor to secure a loan.

- Individuals or businesses willing to act as guarantors for loans.

Instructions for completing this form

- Identify and enter the details of all parties, including names and roles (Makers and Guarantor).

- Specify the loan amount and any amendments related to the loan documents.

- Fill in the sections outlining the obligations and liabilities of the guarantor.

- Obtain signatures from all parties involved, including the guarantor.

- Have the document notarized to ensure its legal validity, if required.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. Notarization provides verification of the identities of the parties involved and the authenticity of the signatures. You can complete this process through US Legal Formsâ integrated online notarization, which offers secure video calls with licensed notaries available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Not providing complete information on all parties involved.

- Failing to clarify the terms of the loan or amendments.

- Neglecting to have the agreement signed and notarized where necessary.

- Overlooking the specific obligations and rights of the guarantor.

Why use this form online

- Convenient access to legal templates anytime and anywhere.

- Editability allows customization to fit your specific situation.

- Reliable templates drafted by experienced attorneys.

Quick recap

- The Loan Guaranty Agreement protects lenders by securing loan obligations through a guarantor.

- It is crucial to match the form with local laws for proper enforceability.

- Proper completion and notarization are essential for the validity of this agreement.

Looking for another form?

Form popularity

FAQ

For a personal loan agreement to be enforceable, it must be documented in writing and signed by both parties. You may choose to keep a copy in your county recorder's office if you wish, though it's not legally necessary. It's sufficient for both parties to keep their own copy, ideally in a safe place.

A guaranteed loan is a loan that a third party guaranteesor assumes the debt obligation forin the event that the borrower defaults. Sometimes, a guaranteed loan is guaranteed by a government agency, which will purchase the debt from the lending financial institution and take on responsibility for the loan.

Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule. Set and interest rate. Put your agreement in writing. Keep payment records.

Identity of the Parties. The names of the lender and borrower need to be stated. Date of the Agreement. Interest Rate. Repayment Terms. Default provisions. Signatures. Choice of Law. Severability.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed. They do not usually say when payment is due, nor include any interest provisions.

A guaranty of payment is an independent agreement by a person or an entity to pay the loan when it goes into default. Even if the borrower is unable or unwilling to pay back the loan, the Bank can require the guarantor to pay it back.

State the purpose for the loan. #Set forth the amount and terms of the loan. Your agreement should clearly state the amount of money you're lending your friend, the interest rate, and the total amount your friend will pay you back.

Guaranty Agreement a two-party contract in which the first party agrees to perform in the event that a second party fails to perform. Unlike a surety, a guarantor is only required to perform after the obligee has made every reasonable and legal effort to force the principal's performance.