Request for Account Verification During Audit 1

Understanding this form

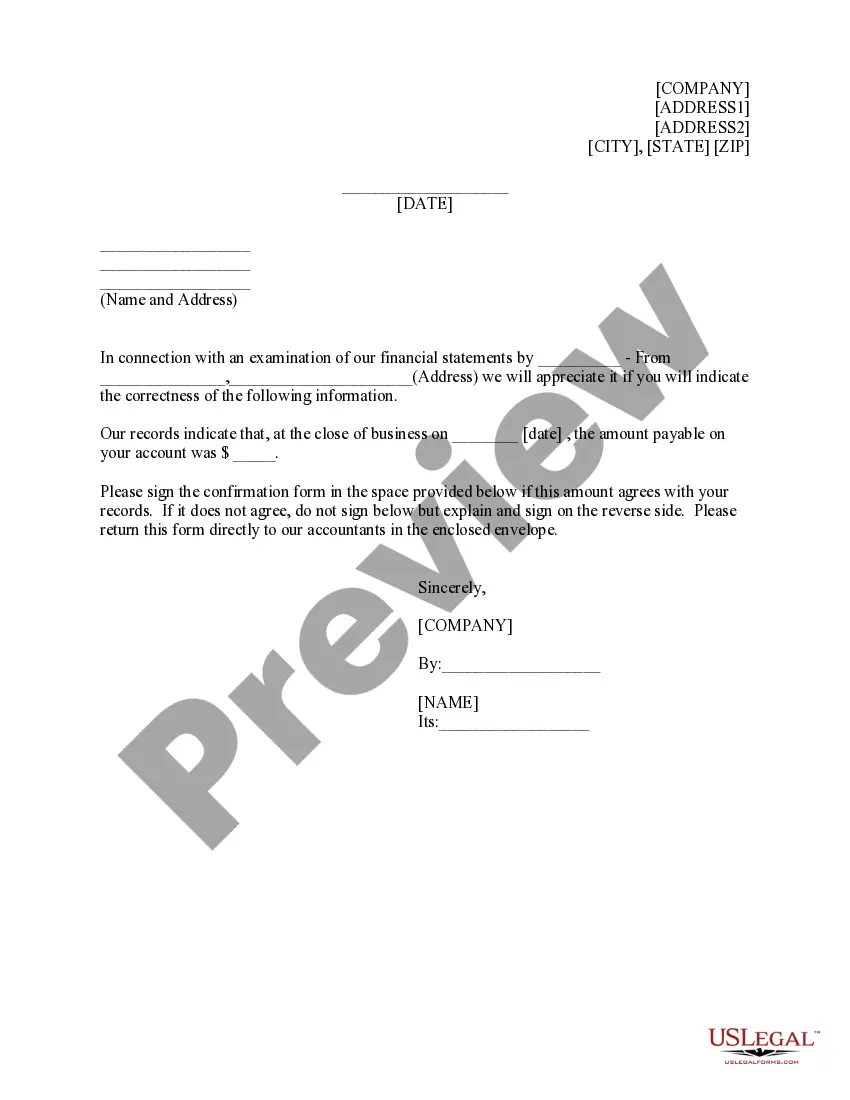

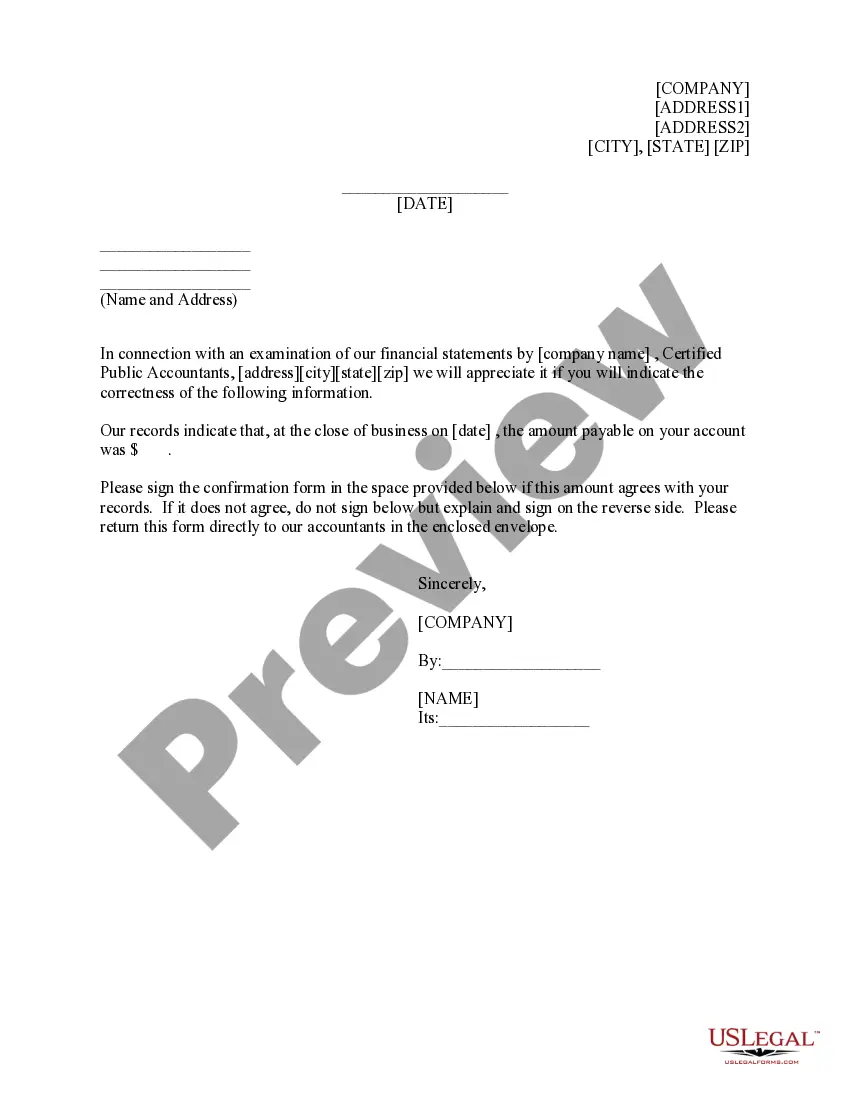

The Request for Account Verification During Audit is a formal document used by companies to verify account balances with clients or vendors during a financial audit. This form serves as a means to ensure that records are accurate and that both parties agree on the financial information presented, distinguishing it from other forms aimed at different financial functions or audits.

Form components explained

- Company name and address: Identifies the business conducting the audit.

- Date of request: Specifies when the verification was initiated.

- Client or vendor account information: Retrieves necessary details for verification.

- Balance amount: States the figure that the company claims is owed as of a specific date.

- Confirmation section: Allows clients to affirm the accuracy of the stated balance.

- Instructions for response: Encourages the return of the form to the auditors.

Situations where this form applies

This form should be used when a company undergoes a financial audit and needs to confirm the accuracy of account balances with its clients or vendors. It is particularly important when discrepancies in account records are suspected or when auditors require confirmation of balances to finalize financial statements.

Who this form is for

- Businesses undergoing financial audits.

- Accountants responsible for preparing financial statements.

- Clients or vendors who need to confirm account balances for accuracy.

- Companies seeking to maintain transparency with their financial records.

Completing this form step by step

- Enter the company's name and address at the top of the form.

- Fill in the date of the request for verification.

- Provide the name and address of the client or vendor being contacted.

- Specify the date and the account balance that needs verification.

- Have the client or vendor sign to confirm the accuracy of the balance or provide corrections on the reverse side.

- Send the completed form directly to the accountants in the provided envelope.

Notarization guidance

This form does not typically require notarization unless specified by local law. Ensure that you check for any specific requirements that may apply in your jurisdiction before submission.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to enter accurate account balance details.

- Not providing the correct date for verification.

- Omitting the client's or vendor's signature on the form.

- Not sending the form directly to the accountants as instructed.

Why complete this form online

- Easy access to downloadable templates created by licensed attorneys.

- Convenient to fill out and edit before finalizing.

- Secure storage and retrieval options available for your records.

- Time-saving by eliminating the need for in-person visits to legal offices.

Looking for another form?

Form popularity

FAQ

An audit confirmation letter is an inquiry sent by the auditor to a third party to establish the contents of the accounting records of the entity that is being audited.

In the context of auditing, Verification is a procedure of examining and confirming the ownership, actual existence, valuation and possession of the assets and liabilities appearing in the Balance Sheet. It is conducted at the end of the accounting period.

Audit Basics: Confirmation Letters The auditor selects the items for which they will request confirmation.The auditor designs the confirmation requests and tailors them to specific audit objectives.The auditor communicates the confirmation request to the third party by sending out the audit confirmation letter.

There are two types of confirmations: A positive confirmation requests that the recipient complete a form confirming account balances (for example, how much a customer owes the company). A negative confirmation requests that the recipient respond only if the balance is inaccurate. 2.

Sample Audit Confirmation Letter: I have enclosed a copy of audit for you and one copy is here in the office with all the previous accounts which I have dealt with. I would like to remind you about the account papers that you have to present for the annual tax return by the end of this year.

Confirmation of accounts receivable is a generally accepted auditing procedure. The auditor should confirm accounts receivable unless (1) they are immaterial, (2) confirmation would be ineffective, or (3) the RMM based on other procedures is judged to be sufficiently low.

Definition of the Confirmation Process Communicating the confirmation request to the appropriate third party. Obtaining the response from the third party. Evaluating the information, or lack thereof, provided by the third party about the audit objectives, including the reliability of that information.

It is a certificate required by auditors in forming an opinion on the company's annual financial statements or carrying out another kind of audit in the company.