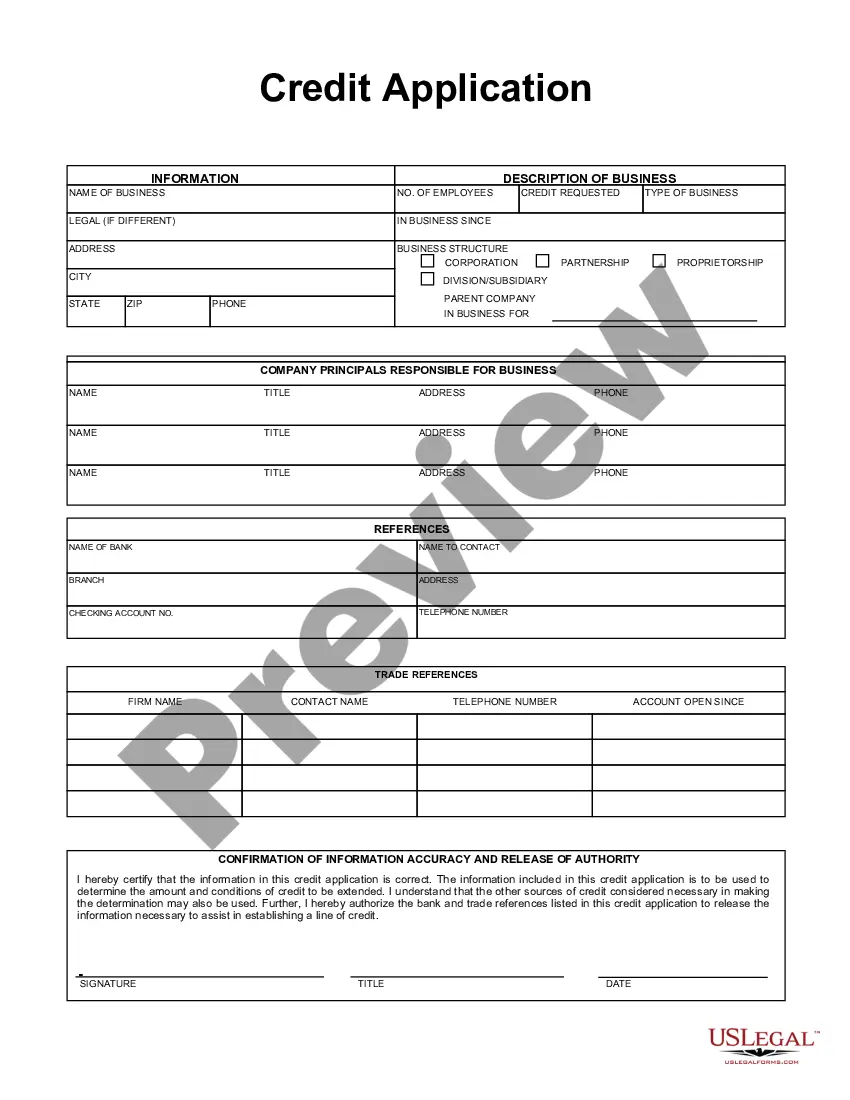

South Carolina Business Credit Application

Understanding this form

The Business Credit Application is a legal document used by individuals or businesses to apply for credit when purchasing goods or services. This form details the terms of repayment, including interest rates, and provides provisions for default and liability. It is essential for establishing a formal agreement between the seller and purchaser and helps ensure clarity and protection for both parties in financial transactions.

Form components explained

- Identification of the seller and purchaser

- Terms of sale, including payment due dates and interest rates

- Provisions for default and collection of debts

- Disclaimer of warranties and responsibilities of the seller

- Conditions regarding the retention of title for goods sold on credit

- Instructions for examining invoices and disputing charges

When to use this form

This form should be used when an individual or business intends to purchase goods or services on credit from a seller and needs to formalize the terms of repayment. It is particularly useful in situations where the buyer may not have sufficient cash flow to make immediate payments or when a seller requires assurance of payment. Utilizing this form helps to mitigate risks associated with credit transactions.

Who this form is for

- Individuals seeking credit for personal or small business purchases

- Small business owners looking to establish credit lines with suppliers

- Corporate entities that require structured credit agreements with vendors

- Partnerships needing to formalize credit terms as guarantors

How to prepare this document

- Identify the seller and enter their business name and contact details.

- Fill in your details as the purchaser, including your legal name and contact information.

- Specify the terms of sale, including due dates for payment and applicable interest rates.

- Review and sign the form, ensuring all parties understand their responsibilities.

- Keep a copy for your records and provide a signed original to the seller.

Does this document require notarization?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to read and understand the terms before signing the agreement.

- Not specifying an interest rate or due date clearly.

- Neglecting to communicate any discrepancies in invoices promptly.

- Assuming all warranties are included without confirming the seller's disclaimers.

Benefits of using this form online

- Convenience of downloading and filling out the form at your own pace.

- Editability allows you to customize terms that suit your specific agreement.

- Reliability of forms drafted by licensed attorneys to ensure legality.

- Access to templates that can save time compared to drafting from scratch.

Looking for another form?

Form popularity

FAQ

640 to 700: Business loan providers generally consider a credit score that falls somewhere between 640 and 700 to be goodbut not excellent. Generally, the minimum credit score for SBA and term loans is around 680.

At a minimum, you will need to provide income tax returns, your credit score, bank account information, a business financial statement, and personal identification such as a driver's license. For more information about loan paperwork, go to Business Loan Documents to Provide.

To qualify for the earned income credit: You must file as single or married filing jointly.You cannot earn over a certain amount of investment income for the year. For 2019 this amount is $3,600, for 2020 the amount is $3,650.

With a credit score between 550 and 620, you could qualify for a short-term loan or even a medium-term loan if your business is doing well. Owners with a credit score over 600. If your credit score is 620 or above, you may qualify for a medium-term loan.

Generally, you should be able to find a startup loan as long as you have at least a few months in business and your credit score is at least 500. You'll also need to show that you have sufficient income (personal or business, depending on the lender's requirements) to repay the loan.

Basic Qualifying Rules Have investment income below $3,650 in the tax year you claim the credit. Have a valid Social Security number. Claim a certain filing status. Be a U.S. citizen or a resident alien all year.

It is difficult to qualify for a small business loan with a credit score lower than 700.Additionally, you should build a strong personal credit score and drive down any debt prior to applying for a business loan.

South Carolina's version of the federal EITC was adopted in 2018 and is being phased in over six years. For tax year 2019, eligible taxpayers could claim up to 41.67% of the federal credit.By tax year 2023, South Carolina taxpayers will be able to claim 125% of the federal EITC.

The credit is calculated on South Carolina Form I-385, Motor Fuel Income Tax Credit. This form must be included with the resident taxpayer's income tax return. The credit is available for up to two private passenger motor vehicles or motorcycles per taxpayer.