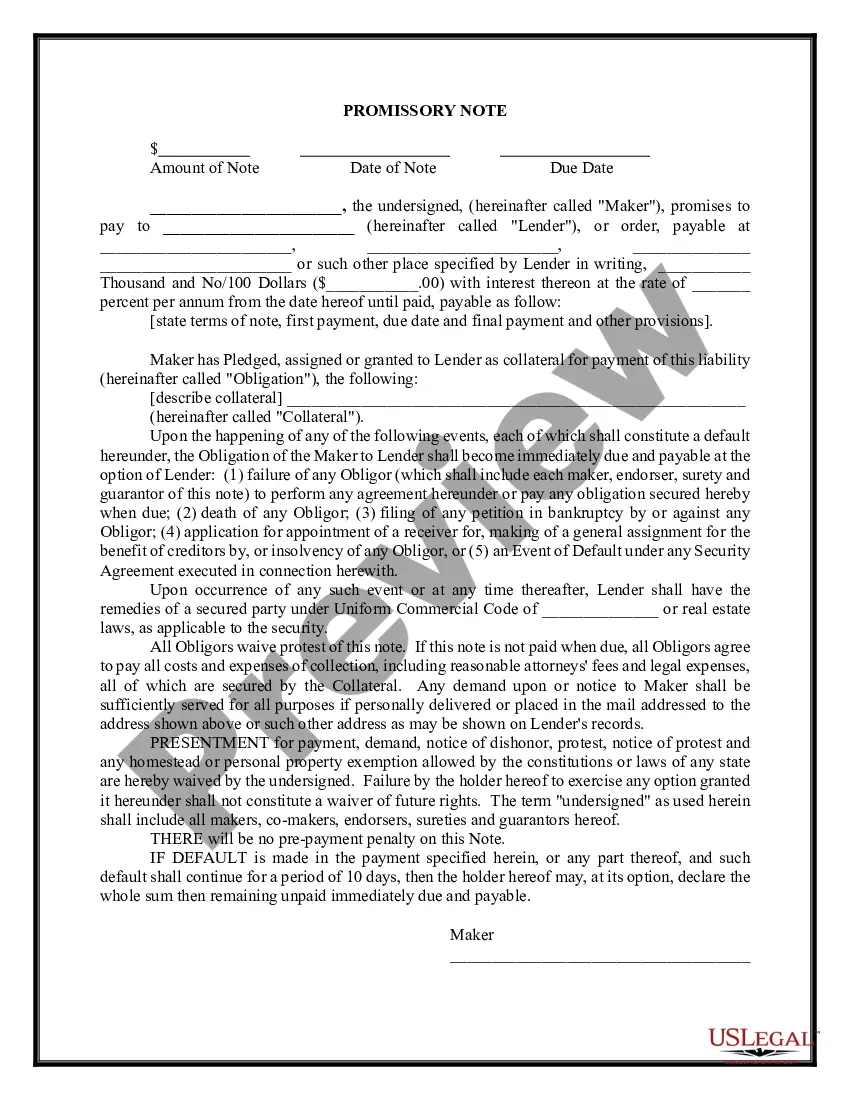

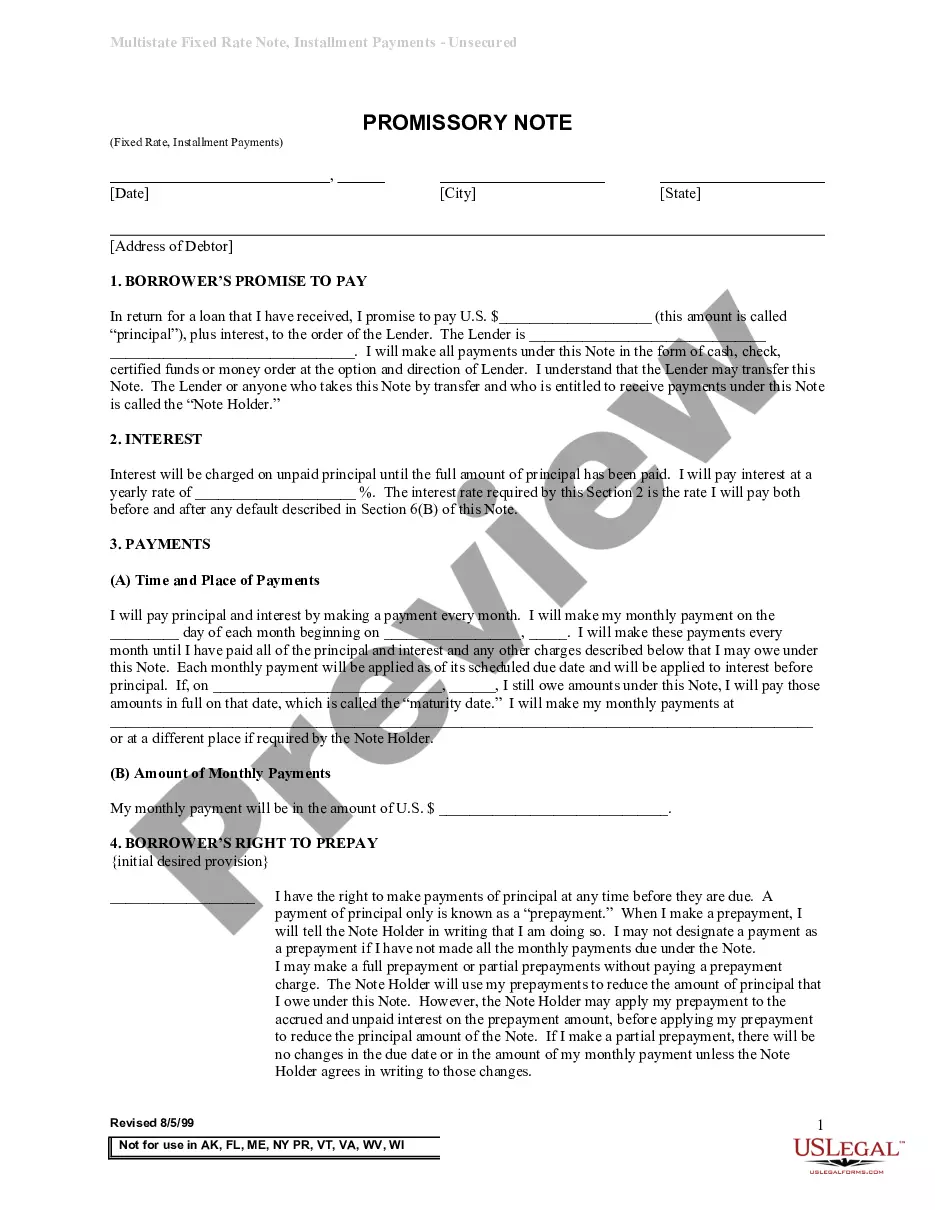

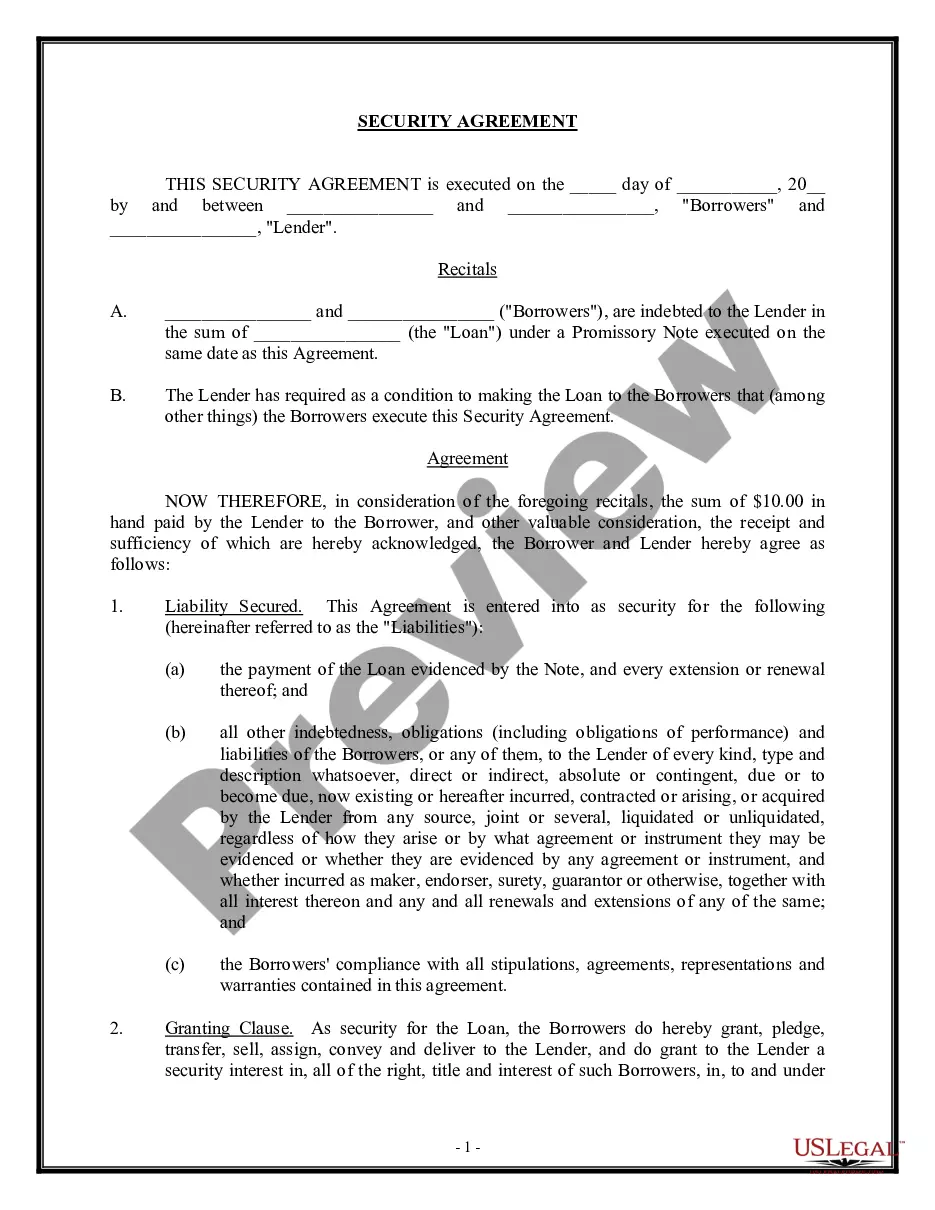

Note Secured By Mortgage On Real Estate

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Multistate Promissory Note - Secured?

Creating legal documents from the ground up can occasionally be somewhat daunting.

Certain situations may require extensive research and substantial financial investment.

If you're looking for a more straightforward and cost-effective method of preparing Note Secured By Mortgage On Real Estate or any other paperwork without the hassle, US Legal Forms is always available to assist you.

Our online repository of over 85,000 current legal documents covers nearly every facet of your financial, legal, and personal affairs.

Before proceeding directly to download the Note Secured By Mortgage On Real Estate, please consider these suggestions: Review the form preview and descriptions to ensure you are on the correct document, verify that the template you select meets your state and county's standards, choose the most suitable subscription plan to acquire the Note Secured By Mortgage On Real Estate, and then download the form. Afterward, fill it out, certify it, and print it. US Legal Forms boasts a flawless reputation and over 25 years of expertise. Join us today and simplify the process of completing forms!

- With just a few clicks, you can swiftly obtain templates that comply with state and county regulations, meticulously crafted for you by our legal experts.

- Utilize our platform whenever you need dependable and trustworthy services to quickly locate and download the Note Secured By Mortgage On Real Estate.

- If you're already familiar with our services and have set up an account with us before, simply Log In to your account, find the form and download it, or retrieve it later from the My documents section.

- Don’t have an account? No worries. Setting one up takes hardly any time, and navigating the library is straightforward.

Form popularity

FAQ

The 3 7 3 rule in mortgage refers to a guideline aimed at improving the clarity of mortgage lending. It suggests that lenders should provide borrowers with three key pieces of information within seven days of application, and all details should be clearly understood within three days of closing. This rule promotes transparency in lending, helping borrowers make informed decisions regarding their note secured by mortgage on real estate.

Yes, mortgage notes are typically considered public records. When a mortgage is recorded with the local government, the associated note is also made available for public viewing. This transparency helps potential buyers and lenders verify the status of a property, ensuring that a note secured by mortgage on real estate is documented and accessible. However, specific details might vary by state, so it's wise to check local regulations.

Generally, a letter of credit is not directly secured by real estate. Instead, it is a financial instrument issued by a bank, providing a guarantee of payment to a seller or lender. However, in some cases, if you need additional security, you might be able to back a letter of credit with real estate through a separate agreement. This could create a layered approach to securing your financial obligations.

The main difference lies in collateral. A secured note is backed by an asset, such as real estate, which provides the lender with a claim if the borrower defaults. In contrast, an unsecured note lacks collateral, making it riskier for lenders. Therefore, a note secured by mortgage on real estate tends to offer better protection for investors.

Secured notes can be a solid investment option due to the reduced risk they offer. Since these notes are backed by real estate, they often provide a level of security that unsecured investments lack. Investors looking for reliable returns may find that a note secured by mortgage on real estate serves as a stable addition to their portfolio.

What should be included in a Secured Promissory Note? The amount of the loan and how that money may be transferred. All parties involved and their contact information. ... Repayment schedule. ... Any interest on the loan. ... The details of the collateral.

Because a mortgage note is a security instrument, it can be bought and sold on the secondary mortgage market. Therefore, mortgage lenders sometimes sell mortgage notes to real estate investors who are attracted to these relatively risk-free investments and the potential to earn passive income.

A secured note is guaranteed by an interest in an asset that is worth at least the amount of the note. If you have a mortgage or an automobile loan, you are the borrower in a secured note. In the case of a mortgage, you hold a secured note with your home pledged as collateral.

The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust.

What is included in a promissory note? Amount you're borrowing. Interest rate (if an adjustable-rate mortgage, this is the introductory rate) Amount of monthly payment and due date. Information about the property. Information about the borrower's ?right to prepay? ARM cap information, if applicable.