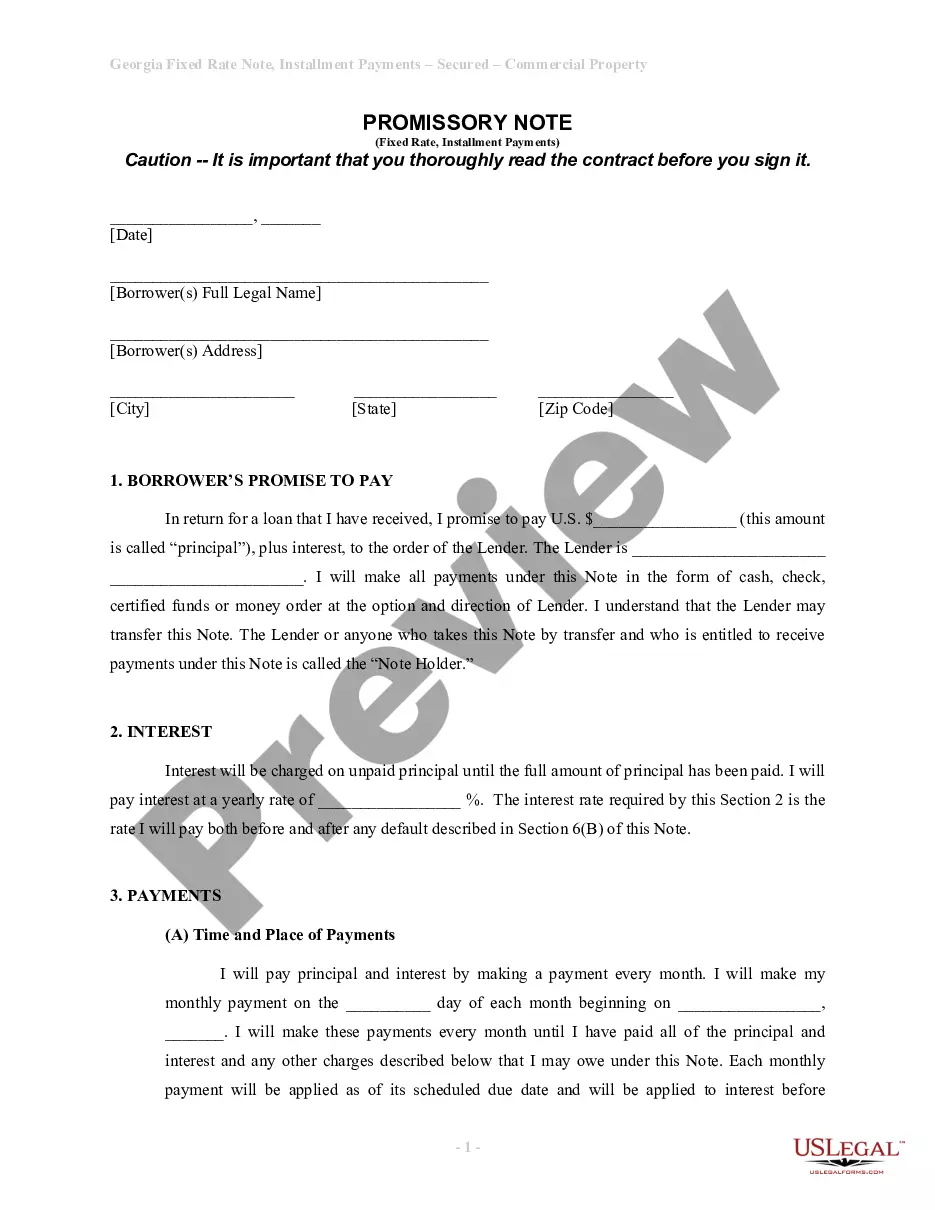

Georgia Promissory Note Without Interest Tax Implications

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Georgia Unsecured Installment Payment Promissory Note For Fixed Rate?

When you wish to finalize the Georgia Promissory Note Without Interest Tax Consequences that adheres to your local state’s regulations and statutes, numerous alternatives are available to choose from.

There's no requirement to verify each document to ensure it meets all the legal criteria if you are a US Legal Forms member.

It is a reliable source that can assist you in obtaining a reusable and current template on any topic.

Acquiring properly composed official documents becomes easy with US Legal Forms. Moreover, Premium members can also benefit from the robust integrated tools for online document editing and signing. Experience it today!

- US Legal Forms is the most extensive online repository featuring a collection of over 85,000 ready-to-use documents for business and personal legal matters.

- All templates are validated to correspond with each state's regulations.

- Thus, when you download the Georgia Promissory Note Without Interest Tax Consequences from our site, you can be assured that you possess a valid and current document.

- Acquiring the necessary example from our platform is quite straightforward.

- If you already possess an account, simply Log In to the system, confirm your subscription is active, and save the chosen file.

- In the future, you can access the My documents section in your profile and keep access to the Georgia Promissory Note Without Interest Tax Consequences at any time.

- If it’s your first time with our library, please follow the guidelines below.

- Browse the proposed page and examine it for conformity with your needs.

Form popularity

FAQ

A promissory note must specify the percentage interest charged on the loan. All loans should carry some interest, even if it is between family members.

The buyer doesn't want to have to pay interest, and the seller feels funny asking for it, so they agree, no interest. Unfortunately, the IRS may impute interest received to the seller, even if the parties agreed to zero interest or a rate below the IRS' published rates.

A simple promissory note will state the full amount is due on the stated date; you won't need a payment schedule. You can decide whether to charge interest on the loan amount and include the interest in the document if needed.

Generally, any income you generate from a promissory note is taxable income and must be reported. The income generated is simply the interest you earned on the note for the tax year in question. If you lent the money personally rather than through your business, report the income on your personal income tax return.

Regardless of whether the interest was reported on Form 1099-INT, interest income from promissory notes always must be reported by individual income taxpayers to the IRS on Schedule B of Form 1040. On this schedule, taxpayers total the aggregate amount of interest and ordinary dividends from all sources.