Wisconsin Western District Bankruptcy Guide and Forms Package for Chapters 7 or 13

Overview of this form

The Wisconsin Western District Bankruptcy Guide and Forms Package is designed for individuals looking to file for bankruptcy under Chapters 7 or 13. This package contains essential legal forms and detailed instructions that help users navigate the bankruptcy process. Unlike other bankruptcy forms, this package is specifically tailored for individuals in Wisconsin, offering guidance on choosing the appropriate chapter based on their financial situation.

Key components of this form

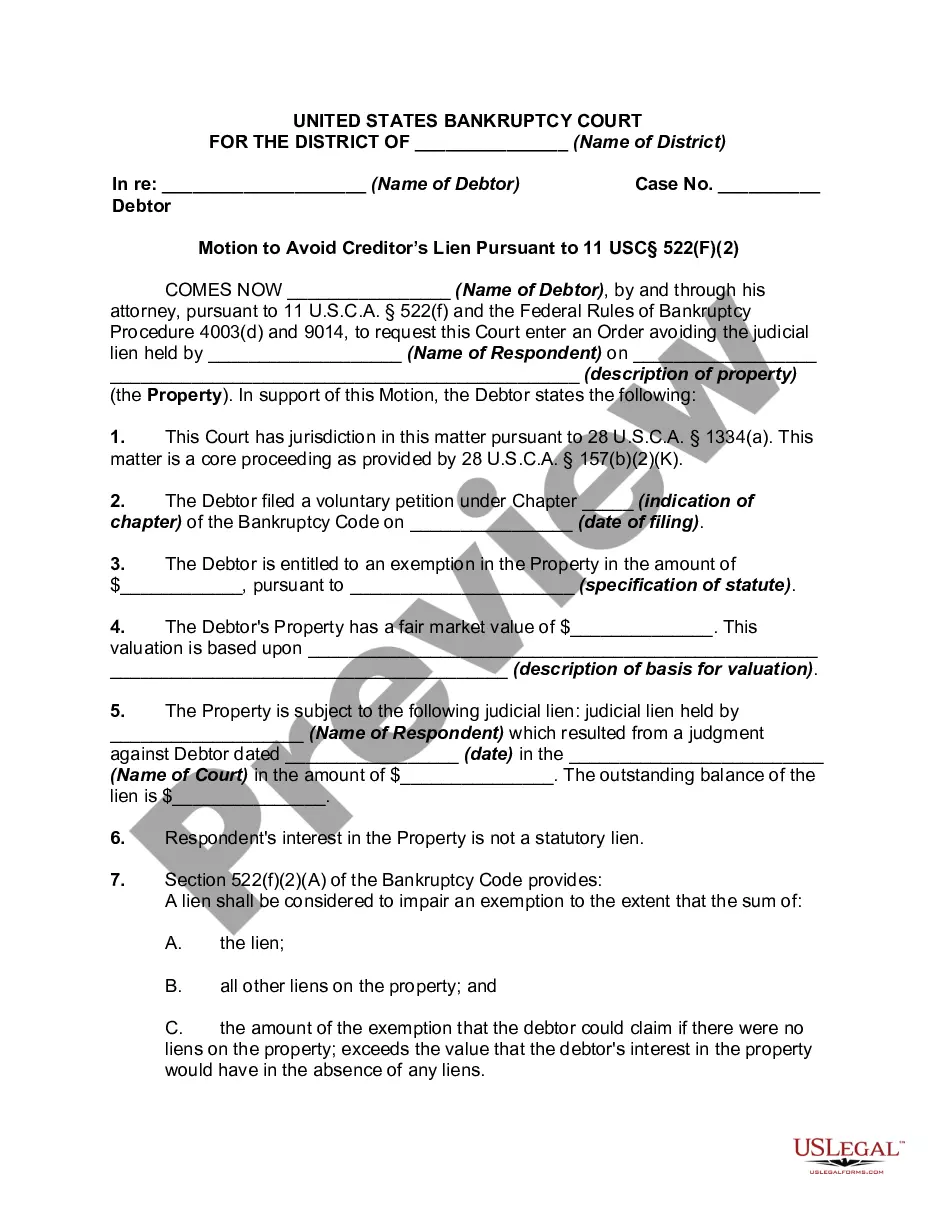

- Chapter 7 and Chapter 13 bankruptcy forms

- Instructions for completing the forms

- Eligibility criteria for each chapter of bankruptcy

- Information about current monthly income and means testing

- Login credentials for accessing the downloadable forms

Situations where this form applies

This form is used when an individual faces overwhelming debt and is considering filing for bankruptcy. Specifically, it is beneficial for those who wish to either liquidate non-exempt assets to discharge debts (Chapter 7) or establish a repayment plan over time for their debts (Chapter 13). It is also applicable if someone needs to confirm their eligibility to file under either chapter based on their income and financial circumstances.

Intended users of this form

This package is intended for:

- Individuals considering bankruptcy in Wisconsin, including married couples and sole proprietors.

- Those unable to pay their debts and seeking debt relief.

- Individuals who have regular income and wish to create a repayment plan via Chapter 13.

- Filers who need assistance determining which chapter of bankruptcy to file under.

How to complete this form

- Determine if you will file under Chapter 7 or Chapter 13 based on your financial situation.

- Gather necessary financial documents, including income statements and debt lists.

- Complete the relevant forms, including the Statement of Current Monthly Income (for Chapter 7) and repayment plan (for Chapter 13).

- Review the completed forms with an attorney, if possible, to ensure accuracy.

- Submit the forms along with any required fees to the bankruptcy court.

Notarization guidance

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to disclose all debts or assets on the forms.

- Choosing the wrong bankruptcy chapter without understanding the implications.

- Not completing the means test correctly before filing Chapter 7.

- Missing deadlines for filing the forms and required fees.

Benefits of using this form online

- Convenience of downloading forms directly from home.

- Editable digital format allows for easy completion.

- Access to the most recent revisions and legal guidelines.

- Ability to quickly store and retrieve forms for future reference.

Legal use & context

- The completed forms serve as official documentation for bankruptcy proceedings in Wisconsin.

- Utilizing the correct forms and following procedures can aid in the successful discharge of applicable debts.

- Failure to properly complete or submit these forms may result in dismissal of the bankruptcy case.

What to keep in mind

- The Wisconsin Western District Bankruptcy Guide and Forms Package supports individuals in filing for bankruptcy under Chapter 7 or Chapter 13.

- Careful consideration and accurate completion of forms are crucial to successfully resolving debt issues.

- Consultation with an attorney is highly recommended to navigate the complexities of bankruptcy law.

Legal terms and meanings

- Bankruptcy discharge: A legal release from personal liability for certain debts.

- Exempt property: Assets that may be protected from seizure in bankruptcy proceedings.

- Means test: A calculation to determine if an individual qualifies for filing under Chapter 7.

- Repayment plan: A structured plan required in Chapter 13 that outlines how debts will be repaid over time.

Looking for another form?

Form popularity

FAQ

A Chapter 7 bankruptcy will generally discharge your unsecured debts, such as credit card debt, medical bills and unsecured personal loans. The court will discharge these debts at the end of the process, generally about four to six months after you start.

What is the bankruptcy discharge process and how long does it take? The discharge process takes 6-8 weeks from time of the last disbursement. Payroll stop deducts sometimes takes up to four weeks to process. The Trustee does a final audit to make sure all claims were paid correctly.

Generally speaking, the debtor's creditors are paid from nonexempt property of the estate. The primary role of a chapter 7 trustee in an asset case is to liquidate the debtor's nonexempt assets in a manner that maximizes the return to the debtor's unsecured creditors.

A discharge is a win! The bankruptcy discharge order wipes out your personal legal liability to pay a debt. A dismissal is usually a loss. It means the bankruptcy case was closed before a discharge was entered.

A Chapter 13 debt discharge is a court order releasing the debtor of all debts that are dischargeable.Creditors are also prohibited from trying to collect debts after the case is finalized.

When you log into your account, you will see a month and year in the top right corner. As a general rule, this is a the approximate date as to when your Chapter 13 bankruptcy will finish.

Although a chapter 13 debtor generally receives a discharge only after completing all payments required by the court-approved (i.e., "confirmed") repayment plan, there are some limited circumstances under which the debtor may request the court to grant a "hardship discharge" even though the debtor has failed to

Analyze your debt. Determine your property exemptions. Make sure you are eligible. Redeem or reaffirm secured debts. Fill out the bankruptcy forms. Take a credit counseling course. File the forms. Pay the filing fee or request a fee waiver.

Chapter 7 bankruptcy allows liquidation of assets to pay creditors. Unsecured priority debt is paid first in a Chapter 7, after which comes secured debt and then nonpriority unsecured debt. Filing Chapter 7 typically involves completing forms and a review of assets by the trustee.