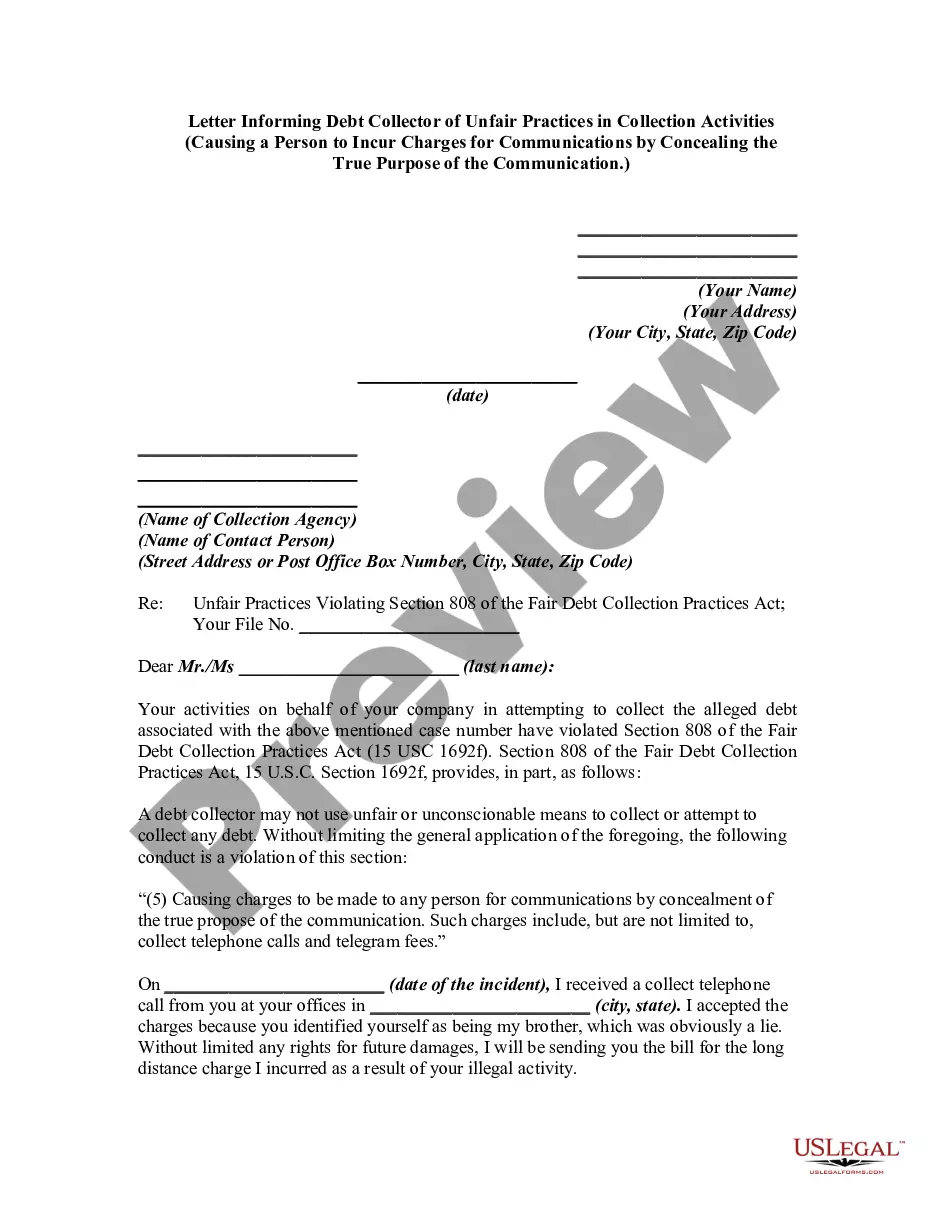

Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Understanding this form

This form is a Notice to Debt Collector used to inform a debt collector that they have violated the Fair Debt Collection Practices Act (FDCPA). It specifically addresses situations where a collector may have incurred charges to the consumer by concealing the real purpose of their communications. By sending this notice, you increase the likelihood that the debt collector will comply with the FDCPA. If noncompliance continues after this notification, it can further support your claims of intentional misconduct.

Key parts of this document

- Your contact information: Includes your name and address.

- Debt collector's information: Provides the name and address of the debt collector.

- Case number: Unique identifier for the debt in question.

- Description of the violation: A space for you to explain how the debt collector's actions violated the FDCPA.

- Second notice: Structure for notifying the debt collector of repeated violations, with a section to list the specific incidents.

- Enclosures section: A listing for including copies of complaint letters sent to appropriate authorities.

Common use cases

This form should be used when you have received communications from a debt collector that may have concealed their intent, leading to additional charges on your part. It is appropriate to send this notice after you have identified such a violation of the FDCPA or after a first warning has been ignored. The form also serves as a precursor to further legal actions, such as filing a complaint with the Federal Trade Commission (FTC) or taking civil action for damages.

Who this form is for

- Consumers who have been contacted by debt collectors.

- Individuals who have incurred charges due to misleading communications from a debt collector.

- Anyone seeking to assert their rights under the Fair Debt Collection Practices Act.

- Those who wish to document the violation for potential legal action.

Instructions for completing this form

- Enter your personal information at the top of the form, including your name and address.

- Fill in the debt collector's details, including the company name and address.

- State the relevant case number associated with the alleged debt.

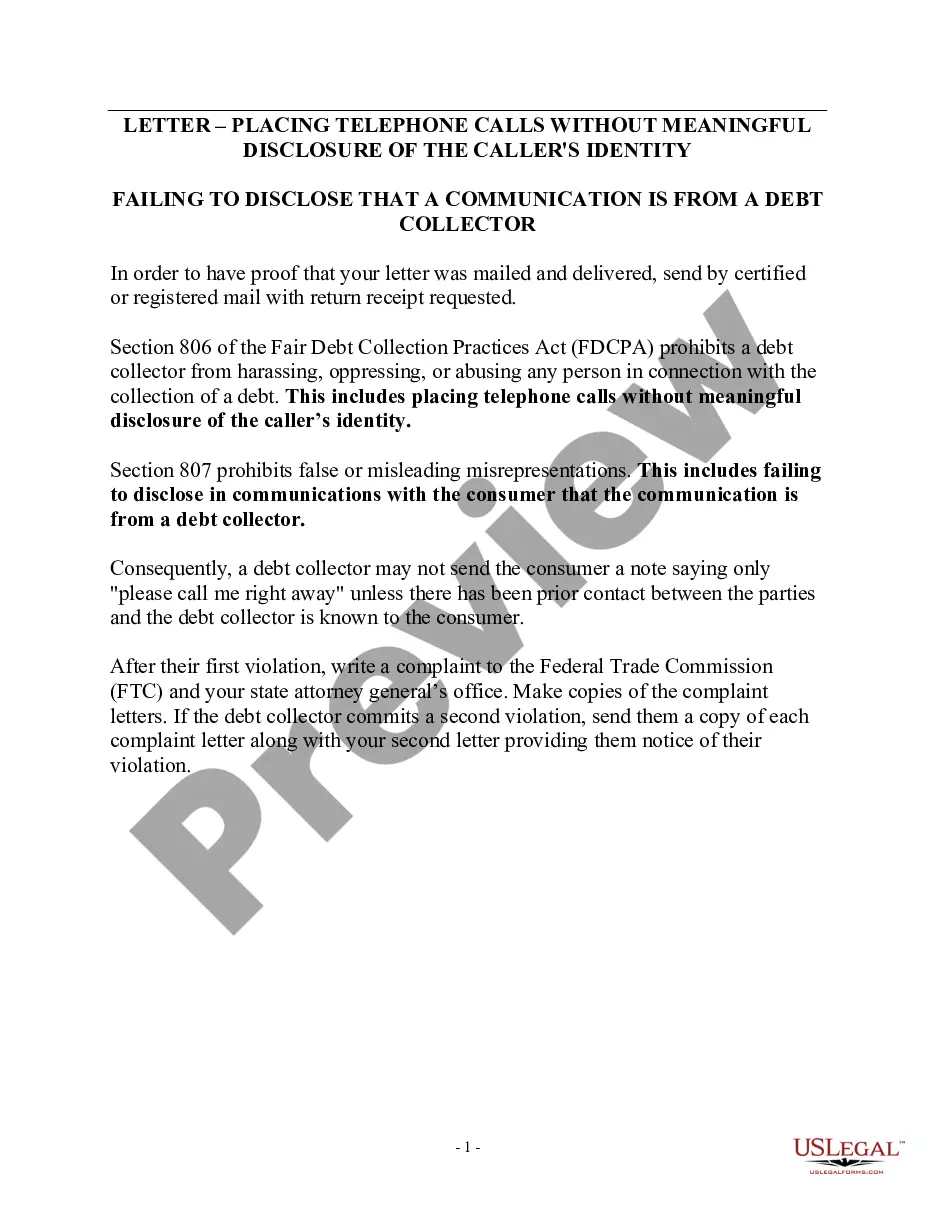

- In the violation description section, clearly explain how the debt collector's actions violated Section 808 of the FDCPA.

- Send the notice via certified or registered mail to ensure proof of delivery.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to provide specific details about the violation.

- Omitting the case number associated with the debt.

- Not sending the notice via certified mail, which is crucial for documentation.

Advantages of online completion

- Convenience of immediate download and access.

- Editability allows for personalization to match your specific situation.

- Reliability of using a form designed by licensed attorneys ensures legal soundness.

Legal use & context

- The FDCPA protects consumers from unfair or deceptive debt collection practices.

- Utilizing this form can help establish a record of the collector's violations.

- Should the issue escalate, this notice can support potential legal claims against the collector.

Summary of main points

- This form is essential for consumers facing unfair debt collection practices.

- Documenting violations can strengthen your legal position if further actions are necessary.

- Timely notification to the debt collector can often prompt compliance with the law.

Looking for another form?

Form popularity

FAQ

If the debt is still listed on your credit report, it's a good idea to pay it off so you can improve your credit card or loan approval odds. Keep in mind that paying the debt won't remove it from your credit report (unless you negotiate a pay for delete), but it does look better than the alternative.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

It's much better to deal with creditors than debt collectors. Whatever the past-due debt is for doctor bills, credit card payments, car loan the creditor may still see you as a potential return customer.You may be able to deal directly with the original creditor, but you won't know until you ask.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Improve Your Credit Score After seven years, collection accounts drop off your credit report, even if you never pay them. 1 But if the accounts are less than seven years old and not approaching the credit reporting time limit, a paid collection is better for your credit score than an unpaid one.

If the debt has been sold to a collection agency interest and charges will usually stop.However, in some cases a debt collection agency may continue adding interest and charges. They can only add amounts which are allowed in the contract you signed with the original creditor.

You might get sued. The debt collector may file a lawsuit against you if you ignore the calls and letters. If you then ignore the lawsuit, this could lead to a judgment and the collection agency may be able to garnish your wages or go after the funds in your bank account.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.