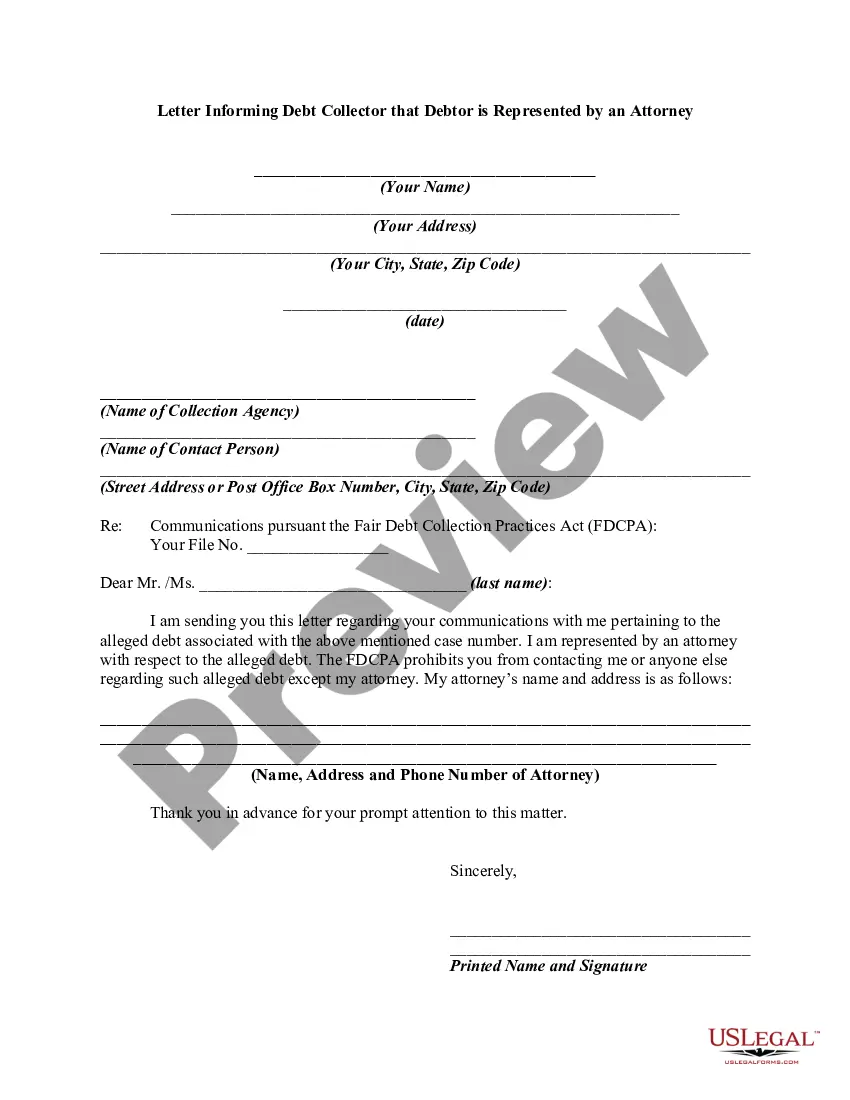

Letter to Debt Collector - Only Contact My Attorney

About this form

This document is a Letter to Debt Collector - Only Contact My Attorney. It serves to formally notify a debt collector that you are represented by an attorney and request that they cease direct communication with you. This letter is an important tool for individuals facing debt collection issues, as it helps establish communication boundaries and protects your rights under the Fair Debt Collection Practices Act (FDCPA).

Main sections of this form

- Sender's information: Your name, address, and date.

- Recipient's information: The debt collector's company name, contact person, and address.

- Case number reference: A specific case number related to the alleged debt.

- Attorney's information: Your attorney's name, address, and contact details.

- Notice of your representation: A statement requesting the collector to direct all communications to your attorney.

- Documentation of violations: Notices regarding any violations of the FDCPA and a request to cease further contact.

Common use cases

This form should be used when you are being contacted by a debt collector and have retained an attorney to handle your debt issues. It is essential in situations where direct communication from the collector may be intrusive or overwhelming. The letter protects your rights by informing the collector that all correspondence should be directed to your attorney.

Who can use this document

- Individuals currently dealing with debt collection efforts.

- People who have hired an attorney to manage their debt-related matters.

- Consumers who wish to communicate boundaries to debt collectors and prevent further direct contact.

Steps to complete this form

- Fill in your name and address at the top of the letter.

- Insert the date when you are sending the letter.

- Provide the debt collector's name and contact details.

- Reference the case number associated with the alleged debt.

- Include your attorney's contact information in the designated section.

- Sign the letter and send it via certified or registered mail for proof of delivery.

Notarization guidance

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include your attorney's contact information.

- Not referencing a specific case number, which could lead to confusion.

- Forgetting to send the letter via certified or registered mail, missing proof of delivery.

- Omitting to make copies of the letter and any correspondence for your records.

Why use this form online

- Convenient access to download and complete the form anytime.

- Editability allows you to customize the form with your specific details.

- Reliability ensures that the form is drafted in compliance with legal standards.

Legal use & context

- This form is designed to assert your rights under the FDCPA.

- Sending this letter may deter the collector from further direct communication and harassment.

- In case of violations by the collector, this letter serves as documentation for potential legal action.

Key takeaways

- Use the letter to formally notify a debt collector to contact your attorney instead.

- Document all communications and any violations of the FDCPA.

- Ensure the letter is sent with proof of delivery to maintain a record.

Looking for another form?

Form popularity

FAQ

The dollar amount of the debt. Original creditor's name and information. Statements about the validity and timeline of your debt repayment. Clear points of contact. Your right to dispute the collection, as well as instructions and required timeline.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

Keep Calm and Respond Promptly. It's important to remember that the unpaid debt has passed through the original creditor to a debt collection attorney. Write It Down. Dispute Discrepancies. Be Upfront and Honest. Follow Up Immediately to a Court Summons.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

If you know that the debt is valid, you may be able to negotiate a settlement payment with the original creditor. If they have already written off the debt, they may accept a lower total payment.If you satisfy the original debt, you can request that the collection agency stop contacting you.

I am responding to your contact about a debt you are attempting to collect. You contacted me by phone/mail, on date. You identified the debt as any information they gave you about the debt. Please stop all communication with me and with this address about this debt.

Working with the original creditor, rather than dealing with debt collectors, can be beneficial. Often, the original creditor will offer a more reasonable payment option, reduce the balance on your original loan or even stop interest from accruing on the loan balance altogether.

Dispute When Collectors SellWhen this happens, you can have the older collection removed by disputing it with the credit bureaus. If the debt collector fails to respond to the dispute, the credit bureau should remove the account since it has not been verified.

If you want to negotiate directly with the creditor, ask the collection agency for the phone number of the collections department of the original creditor. Then call the creditor and ask if you can negotiate on the debt directly with the creditor.