Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities - Failure to Disclose to Debtor in Initial Communication that Debt Collector was Attempting to Collect a Debt

What this document covers

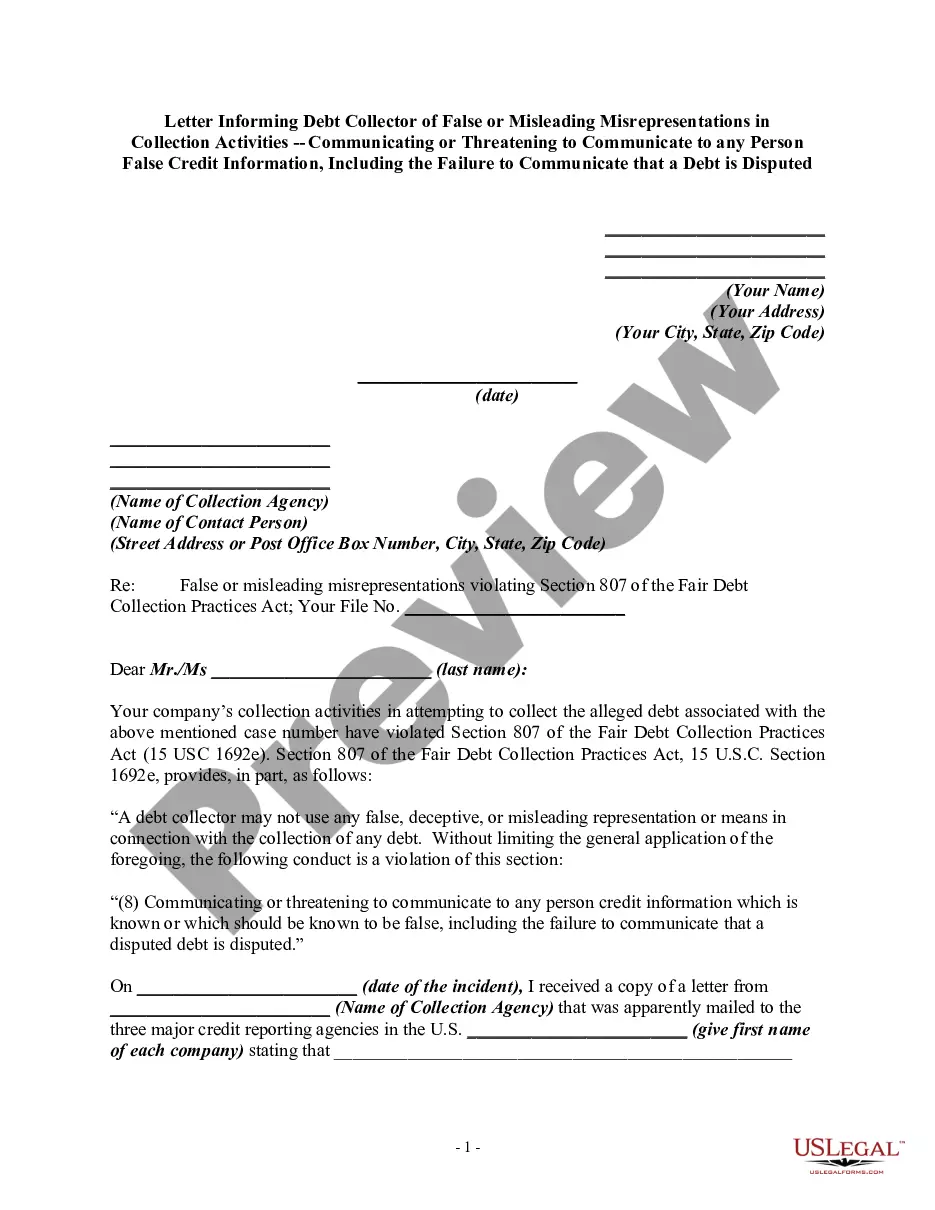

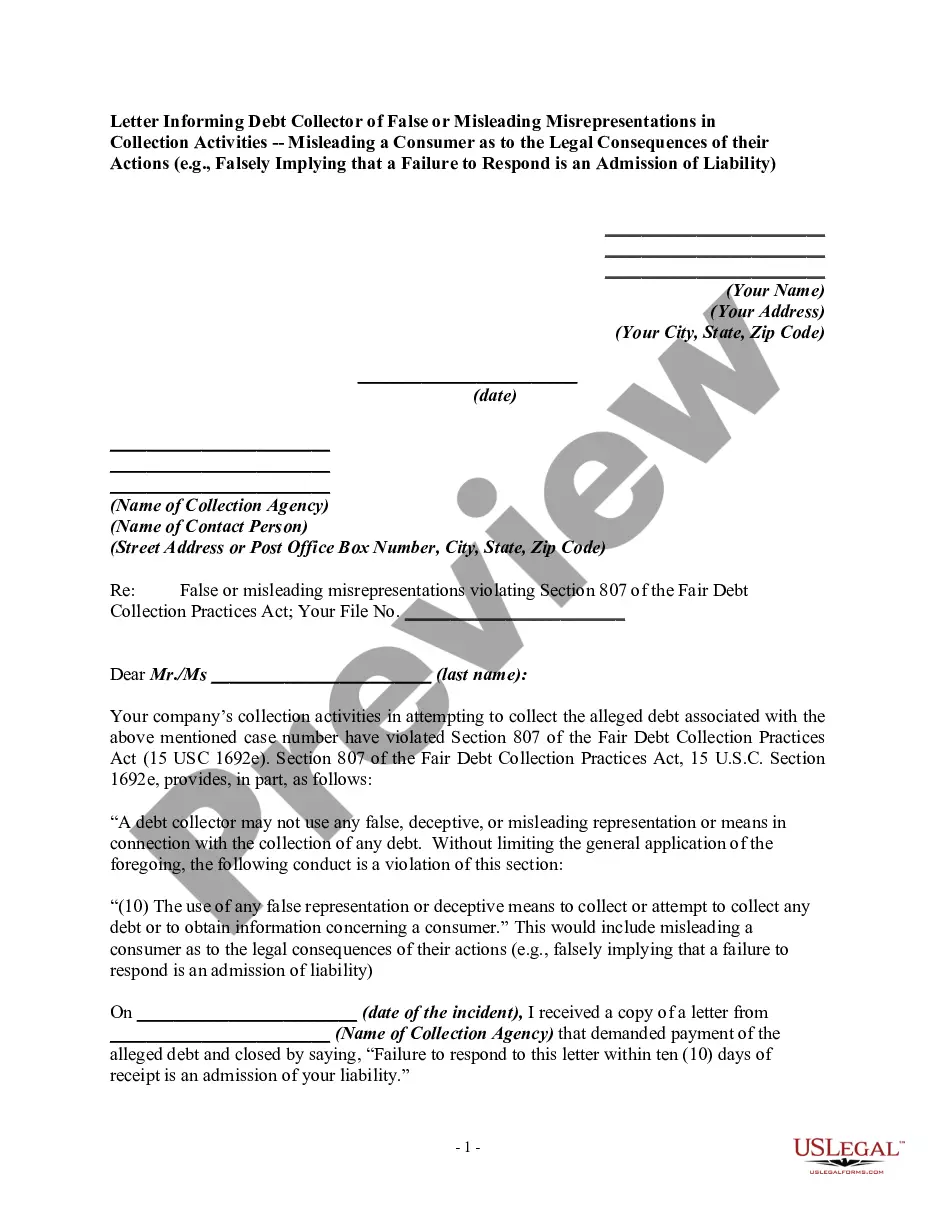

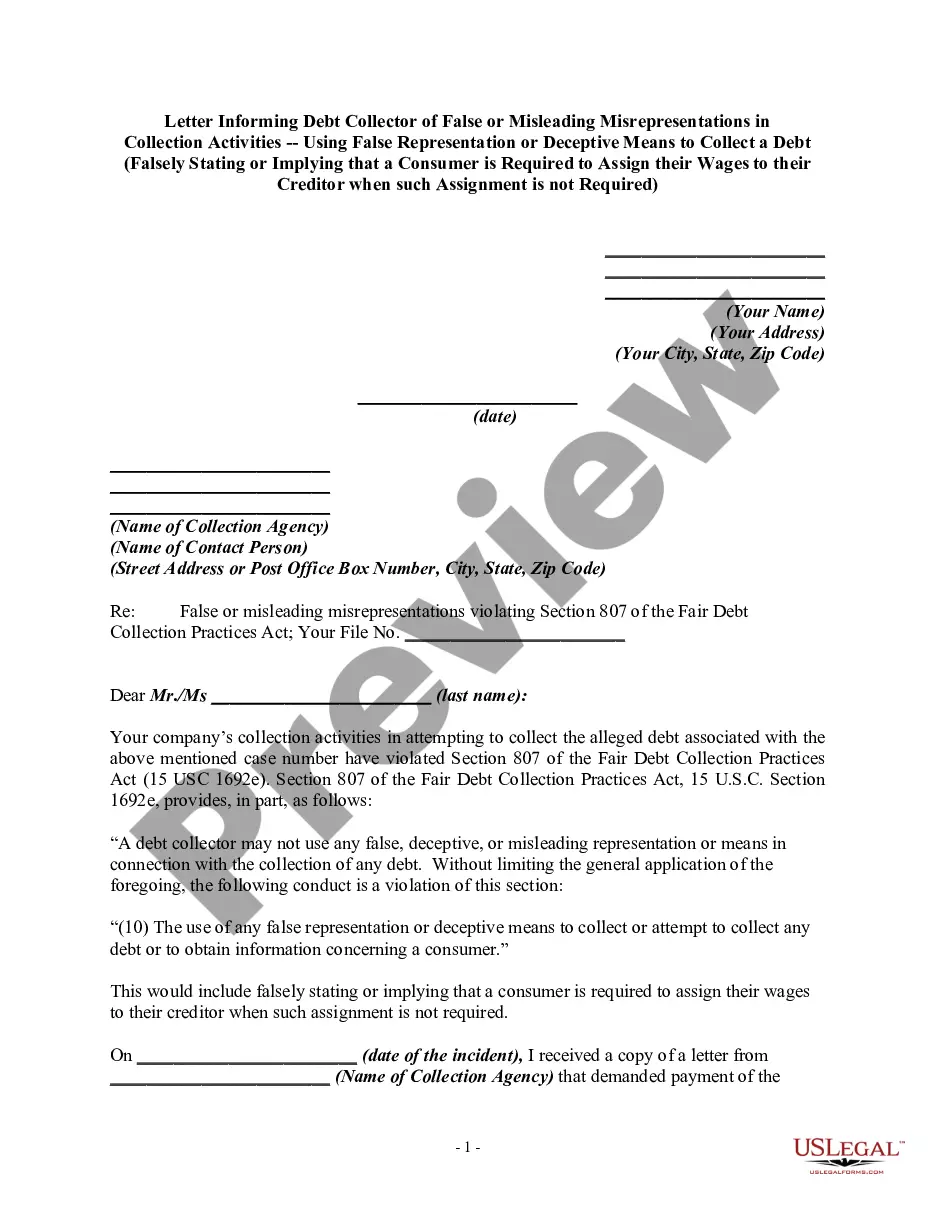

The Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities serves as a formal notice to a debt collector who has failed to properly disclose their intent during initial communications. Specifically governed by Section 807 of the Fair Debt Collection Practices Act, this letter aims to address and rectify misleading practices by debt collectors. By using this letter, individuals can assert their rights and demand compliance with legal standards, distinguishing it from general communications about debts.

Key components of this form

- Your name and address.

- Date of the letter.

- Name and address of the collection agency.

- Reference to the Fair Debt Collection Practices Act violation.

- Details of the initial communication incident.

- Your printed name and signature.

When to use this form

Who should use this form

- Individuals who have been contacted by a debt collector.

- Consumers who believe a debt collector has misrepresented themselves.

- Individuals seeking to assert their legal rights under the Fair Debt Collection Practices Act.

Completing this form step by step

- Enter your name and full address at the top of the letter.

- Insert the date when you are filling out the letter.

- Provide the name and address of the collection agency.

- Clearly state the specific violation of the Fair Debt Collection Practices Act.

- Describe the details of the initial communication you received from the debt collector.

- Sign the letter by printing your name and adding your signature at the bottom.

Does this document require notarization?

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all required personal information.

- Not clearly stating the violation of the Fair Debt Collection Practices Act.

- Leaving out necessary dates related to the communication.

- Not signing the letter before sending it off.

Why complete this form online

- Convenience of downloading the letter for immediate use.

- Editability allows you to customize the letter to your situation.

- Access to reliable templates drafted by licensed attorneys.

Looking for another form?

Form popularity

FAQ

Reach out to the company the collector says is the original creditor. They might help you figure out if the debt is legitimate and if this collector has the right to collect the debt. Also, get your free, annual credit report online or at 877-322-8228 and see if the debt shows up there. Dispute the debt in writing.

If you believe any account information is incorrect, you should dispute the information to have it either removed or corrected. If, for example, you have a collection or multiple collections appearing on your credit reports and those debts do not belong to you, you can dispute them and have them removed.

The Federal Trade Commission advises that you be as specific as possible in the letter about the reason why you think you do not owe this debt (or owe all of it, if you're disputing the amount), but you should give as little personal information as possible in the letter.

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

Dispute When Collectors SellWhen this happens, you can have the older collection removed by disputing it with the credit bureaus. If the debt collector fails to respond to the dispute, the credit bureau should remove the account since it has not been verified.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.

Your full name and address. The collections agency's name and address. A request for the amount of the debt claimed to be owed. A request for the name of the original creditor. A request for the judgment information (if applicable) A request for proof of the company's license.