Equipment Lease Agreement with an Independent Sales Organization

What this document covers

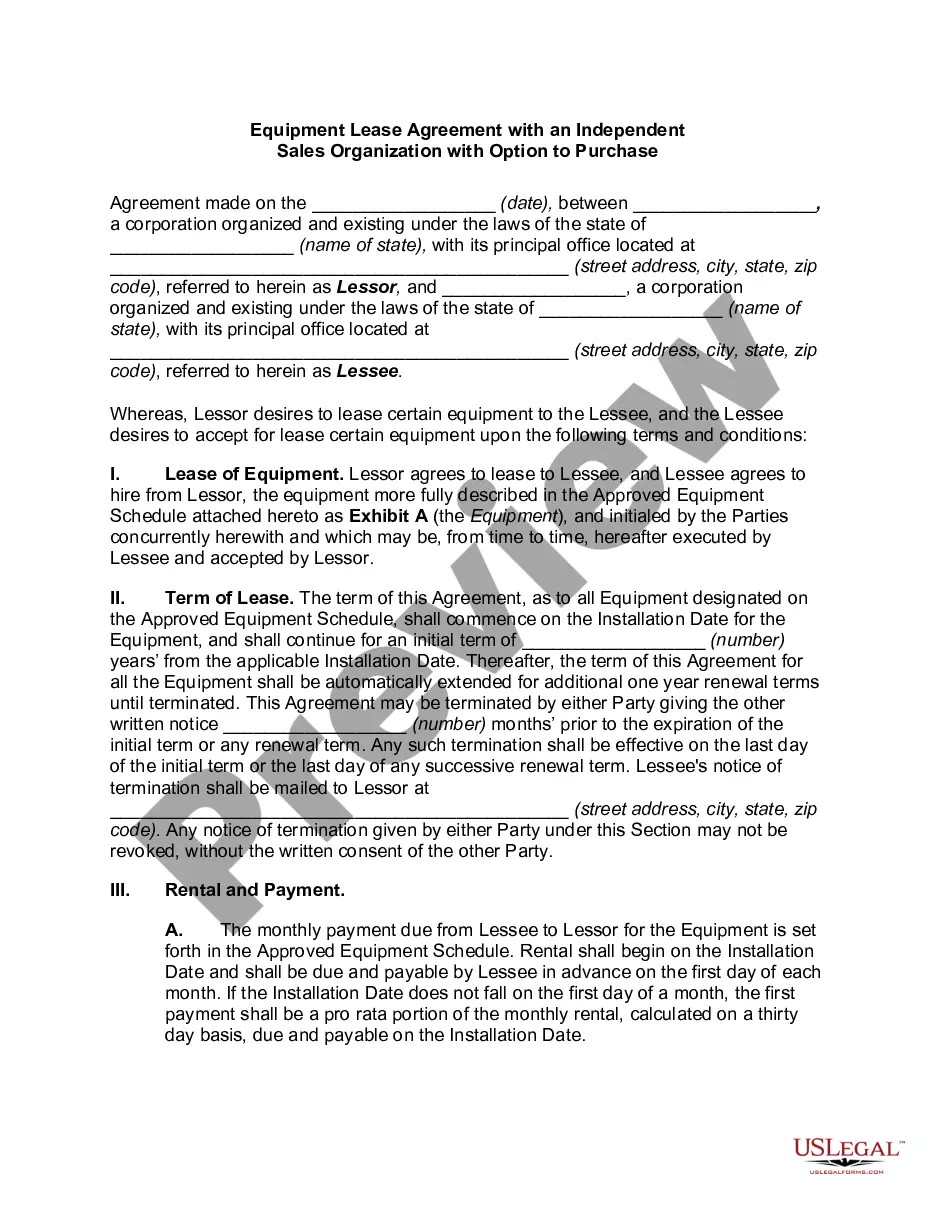

The Equipment Lease Agreement with an Independent Sales Organization is a legally binding document that outlines the terms for leasing equipment between a lessor and a lessee in sectors like computer and software industries. This agreement safeguards the interests of both parties by detailing responsibilities for rental payments, equipment maintenance, and the return of equipment. Unlike simple rental agreements, this comprehensive lease includes clauses for warranties, defaults, and options for purchase, ensuring clarity and protection for both users involved in the transaction.

Form components explained

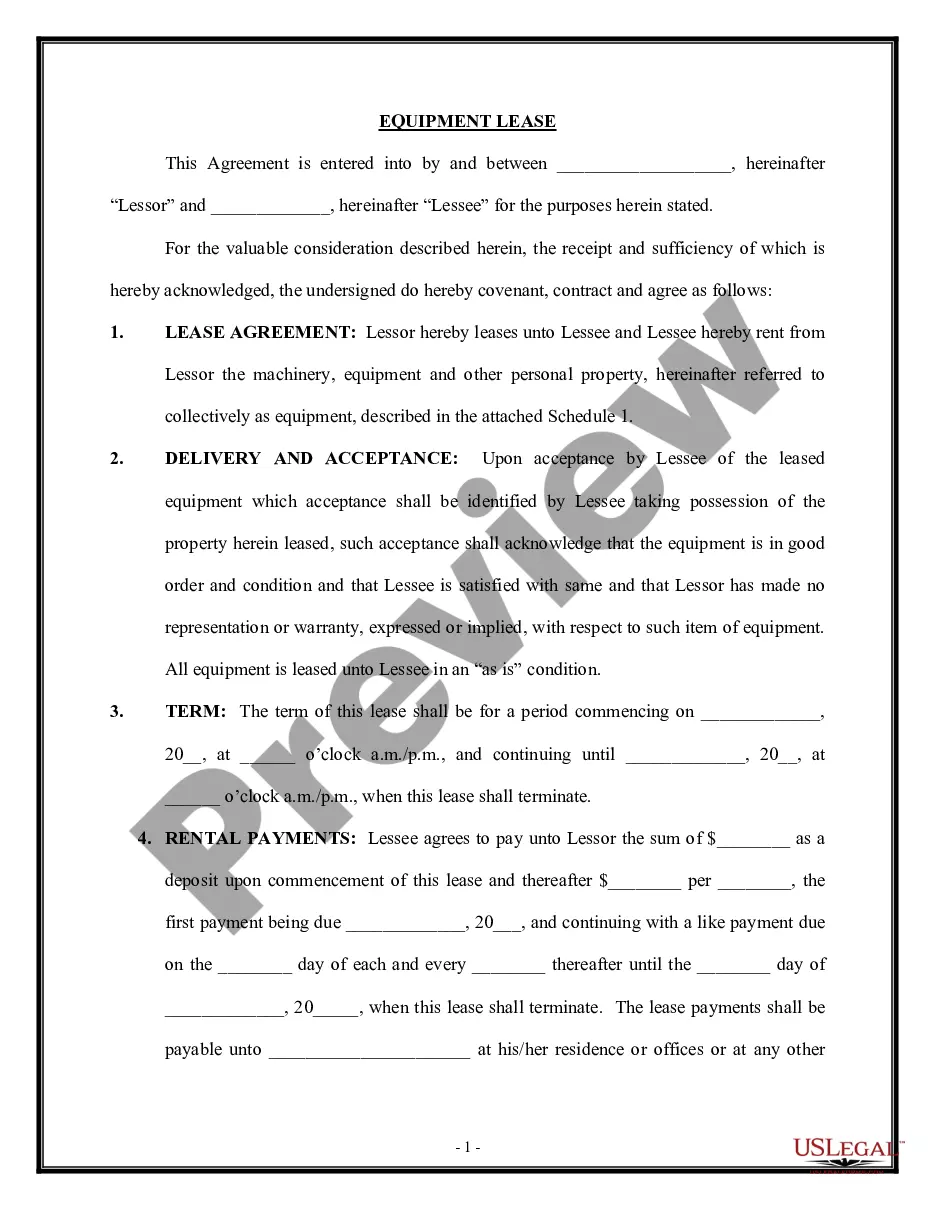

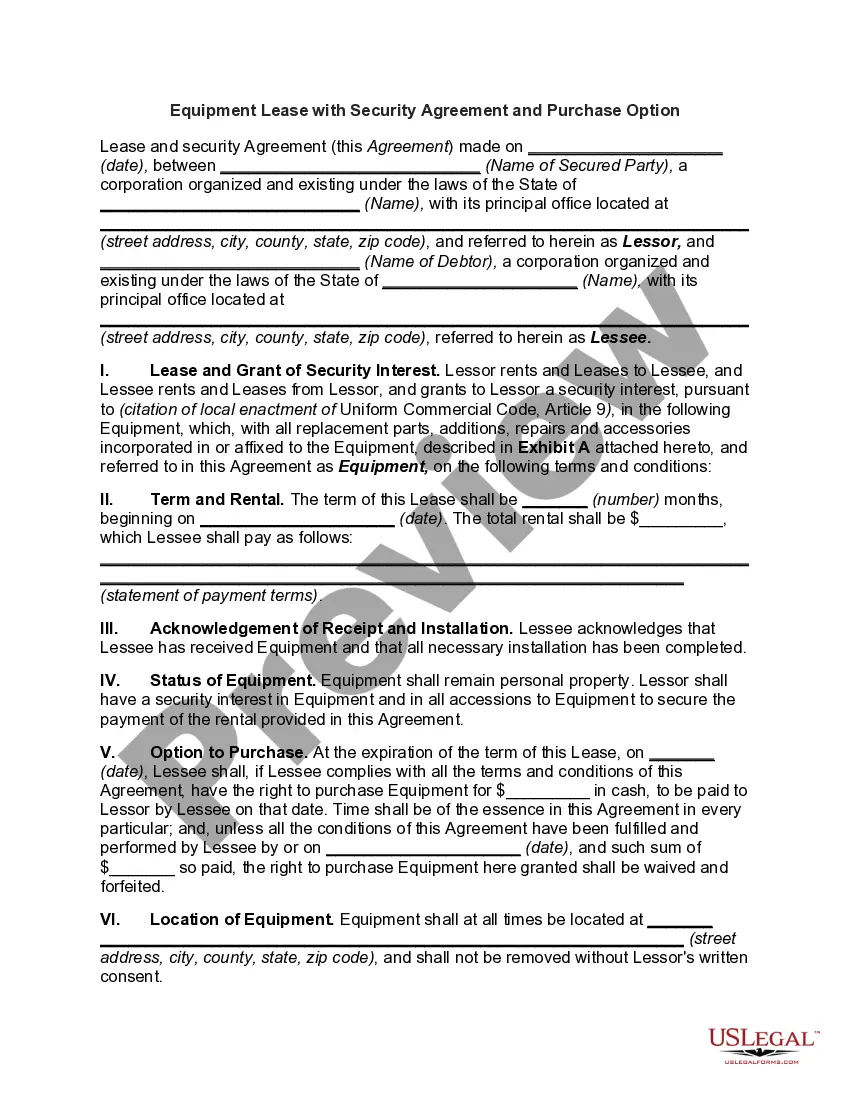

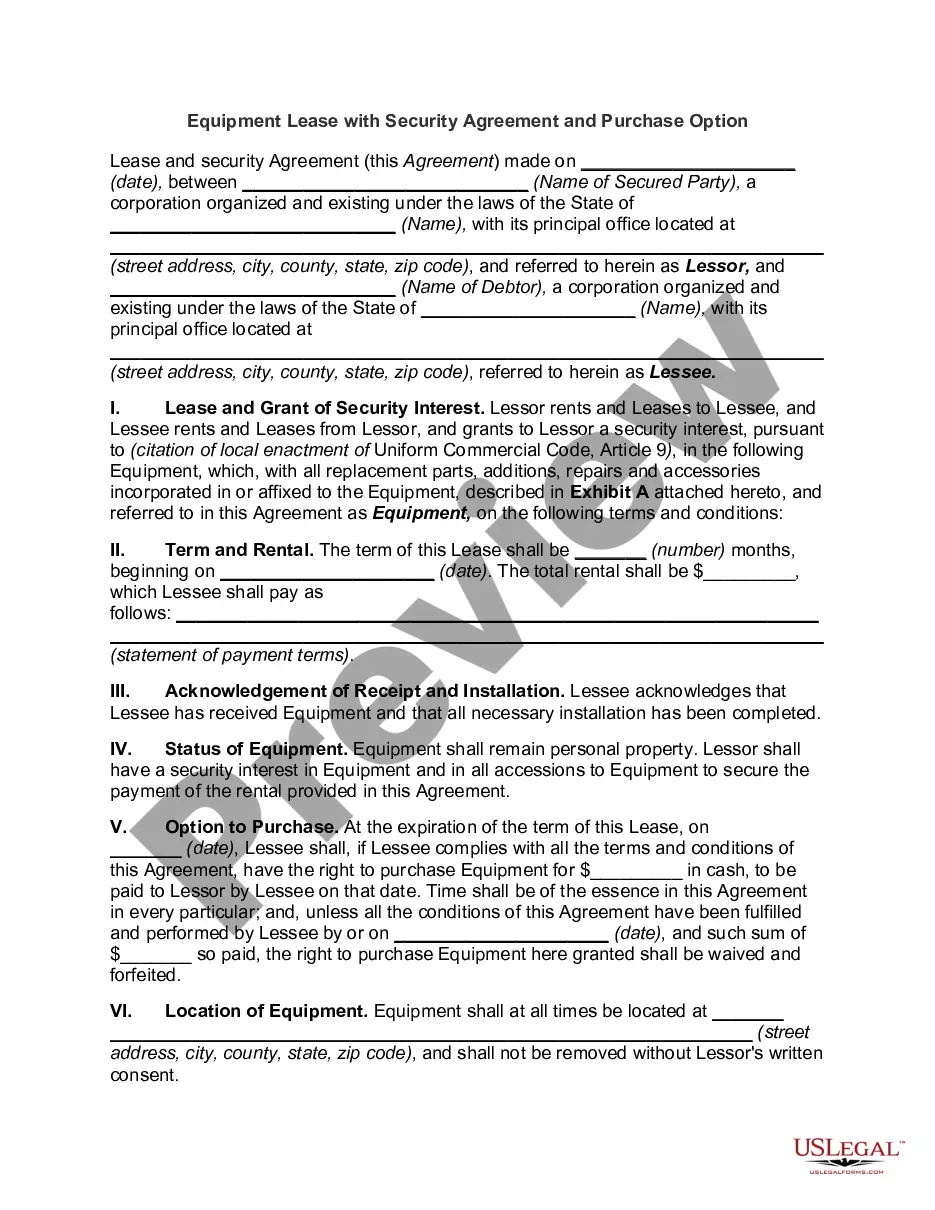

- Parties involved: Identifies the lessor and lessee entering the lease.

- Lease duration: Specifies the initial term of two years and conditions for renewal and termination.

- Payment terms: Outlines monthly rental fees, payment schedule, and penalties for late payments.

- Delivery and installation clauses: Details obligations of both parties regarding equipment delivery and installation.

- Maintenance responsibilities: Clearly states the lessee's obligations for upkeep and repair of the leased equipment.

- Option to purchase: Provides the lessee the right to purchase the equipment under specified conditions.

When to use this document

This form is essential when a business needs to lease equipment rather than purchase it outright. It is applicable in scenarios where a company partners with an Independent Sales Organization to expand operations without a significant upfront investment. This agreement can be utilized in various industries requiring specialized equipment, including technology, manufacturing, and service sectors.

Intended users of this form

- Businesses seeking to lease equipment on a long-term basis.

- Independent Sales Organizations that require equipment to facilitate their operations.

- Companies needing to outline the specific terms and conditions associated with leasing agreements.

- Legal representatives or advisors drafting leasing contracts for clients.

Completing this form step by step

- Identify the lessor and lessee: Clearly enter the names and addresses of both parties.

- Specify the lease term: Fill in the installation date and duration of the lease, noting the initial and renewal terms.

- Enter payment details: Include monthly rental amounts and specify any additional terms related to payment schedules.

- Detail delivery and installation terms: Outline who is responsible for these duties and any related costs.

- Review maintenance obligations: Ensure the lessee understands their responsibilities regarding the upkeep of the equipment.

- Complete the signature section: Both parties should sign and date the agreement to make it legally binding.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify the installation date can lead to misunderstandings about the lease commencement.

- Not clarifying maintenance responsibilities may result in disputes over equipment condition.

- Missing signatures or incorrect party information can invalidate the agreement.

- Failing to review key payment terms may lead to unexpected costs for late payments.

Why use this form online

- Convenient access: Easily download and customize the form from anywhere at any time.

- Editable format: Modify the agreement to meet specific business needs without extensive legal costs.

- Guided process: Online templates often include prompts to ensure all necessary information is captured.

- Legally vetted: Using forms prepared by licensed attorneys ensures compliance with legal standards.

Looking for another form?

Form popularity

FAQ

Yes. An LLC is a legal entity. A legal entity can lease property from others, including from its owners, which of course would include a member of the LLC. Rental payments from the LLC can be paid but you should also review with both your...

Assets being leased are not recorded on the company's balance sheet; they are expensed on the income statement. So, they affect both operating and net income.

Unlike an outright purchase or equipment secured through a standard loan, equipment under an operating lease cannot be listed as capital. It's accounted for as a rental expense. This provides two specific financial advantages: Equipment is not recorded as an asset or liability.

There are two main types of leases that can be used to purchase used equipment: Operating leases and Capitol Finance leases. Operating Lease This type of lease offers the lowest payment in any kind of financing scheme.There's also a tax advantage because the equipment is both considered an asset and a liability.

Click on the Create icon 2a01. In the Other column, choose Journal Entry. Add the relevant asset account for Operating Lease- Right-of-Use asset. Debit the present value of your lease payments. Choose the applicable liability account and input the present value of your lease payments.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

The Lease Must be in Writing It does not matter if the lease is handwritten or typed. If the lease is for more than one year, it must be in written form and contain the following terms.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

A lessee must capitalize a leased asset if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An asset should be capitalized if:The lease runs for 75% or more of the asset's useful life.