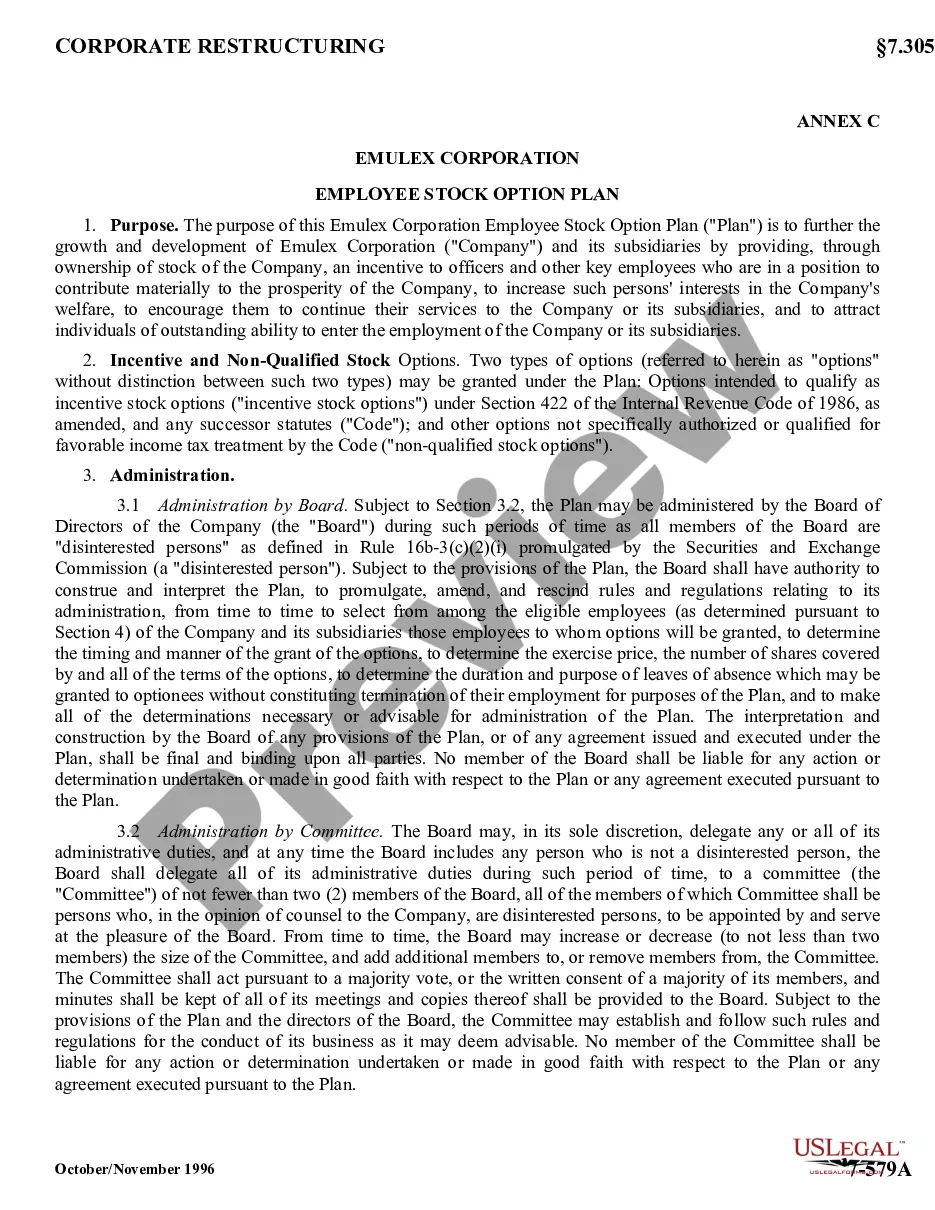

Stock Award Plan of Optelecom, Inc.

About this form

The Stock Award Plan of Optelecom, Inc. is a legal document designed for corporations to create a framework for granting stock awards to employees, officers, and consultants. This plan serves as a tool for businesses to attract and retain talent by offering competitive incentive compensation and opportunities for stock ownership. It is distinct from similar forms due to its specific provisions related to administration, eligibility, and the terms under which stock awards are granted.

Main sections of this form

- Purpose of the Plan: Aims to motivate and reward employees through stock awards.

- Administration: Managed by a committee comprised of nonemployee members of the Board of Directors.

- Stock Subject to the Plan: Provides details about the total number of shares available for awards.

- Eligibility: Defines who can receive stock awards, including employees and consultants.

- Awards and Certificates: Outlines the issuance of stock certificates to recipients.

- Termination and Amendment: Specifies conditions under which the plan can be modified or terminated.

Common use cases

This form should be utilized when a corporation seeks to establish a structured stock award plan to incentivize and reward key employees and consultants. It is particularly useful during the development of employee retention strategies or when looking to enhance compensation packages in competitive markets.

Intended users of this form

- Corporate boards looking to implement an employee stock award plan.

- Human resources professionals responsible for compensation and benefits.

- Business owners who want to retain top talent through stock ownership incentives.

Steps to complete this form

- Identify the purpose of the stock award plan and state the goals clearly.

- Designate the committee responsible for administering the plan and outline their authority.

- Specify the number of shares available for awards and the eligibility criteria for participants.

- Detail the process for issuing stock certificates to award recipients.

- Include guidelines for amending or terminating the plan as necessary.

Is notarization required?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Not specifying eligibility criteria clearly, leading to confusion about who qualifies for stock awards.

- Failing to establish a clear administrative process, which can result in inconsistent implementation of the plan.

- Overlooking necessary compliance with securities regulations, which could invalidate the plan.

Benefits of completing this form online

- Convenience of accessing and downloading the form anytime, from anywhere.

- Editability to tailor the plan according to the specific requirements of your business.

- Reliability of using templates drafted by licensed attorneys to ensure legal sufficiency.

Legal use & context

- The plan is enforceable as long as it complies with established corporate governance laws.

- It allows companies to incentivize and reward employees without cash outlays.

- Properly drafted plans minimize disputes over stock awards and eligibility.

Summary of main points

- The Stock Award Plan of Optelecom, Inc. facilitates employee incentive by granting shares.

- It must be carefully administered according to specific rules to ensure fairness and compliance.

- Regular amendments and shareholder approvals are crucial for ongoing legal compliance.

Looking for another form?

Form popularity

FAQ

RSUs are generally always worth something versus stock options, which can expire worthless if the stock price is below the strike price. Additionally, with RSUs you don't have to come up with the cash to exercise the options if your company doesn't offer some sort of cashless exercise option.

Under US GAAP, stock based compensation (SBC) is recognized as a non-cash expense on the income statement. Specifically, SBC expense is an operating expense (just like wages) and is allocated to the relevant operating line items: SBC issued to direct labor is allocated to cost of goods sold.

200bDefinition200b A restricted stock award is when a company grants someone stock as a form of compensation. The stock awarded has additional conditions on it, including a vesting schedule, so is called restricted stock. Restricted stock awards may also be called simply stock awards or stock grants.

Stock Based Compensation (also called Share-Based Compensation or Equity Compensation) is a way of paying employees, executives, and directors of a company with equity in the business.Shares issued to employees are usually subject to a vesting period before they are earned and can be sold.

A recipient of restricted stock is taxed at ordinary income tax rates, subject to tax withholding, on the value of the stock (less any amounts paid for the stock) at the time of vesting.Any dividends paid while the stock is unvested are taxed as compensation income subject to withholding.

Stock options are only valuable if the market value of the stock is higher than the grant price at some point in the vesting period. Otherwise, you're paying more for the shares than you could in theory sell them for. RSUs, meanwhile, are pure gain, as you don't have to pay for them.

Stock appreciation rights (SARs) are a type of employee compensation linked to the company's stock price during a predetermined period.However, employees do not have to pay the exercise price with SARs. Instead, they receive the sum of the increase in stock or cash.

Under US GAAP, stock based compensation (SBC) is recognized as a non-cash expense on the income statement. Specifically, SBC expense is an operating expense (just like wages) and is allocated to the relevant operating line items: SBC issued to direct labor is allocated to cost of goods sold.

Stock compensation should be recorded as an expense on the income statement. However, stock compensation expenses must also be included on the company's balance sheet and statement of cash flows.