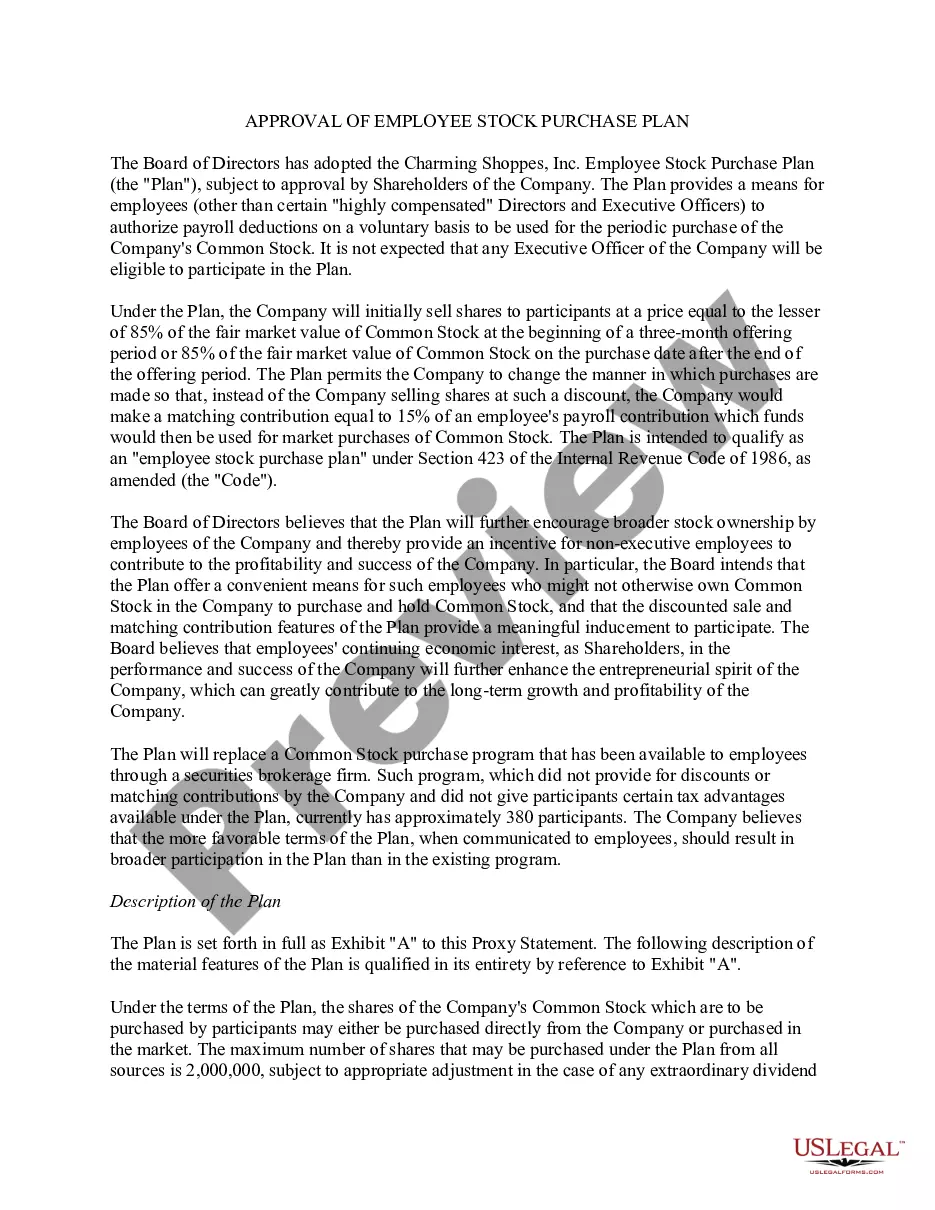

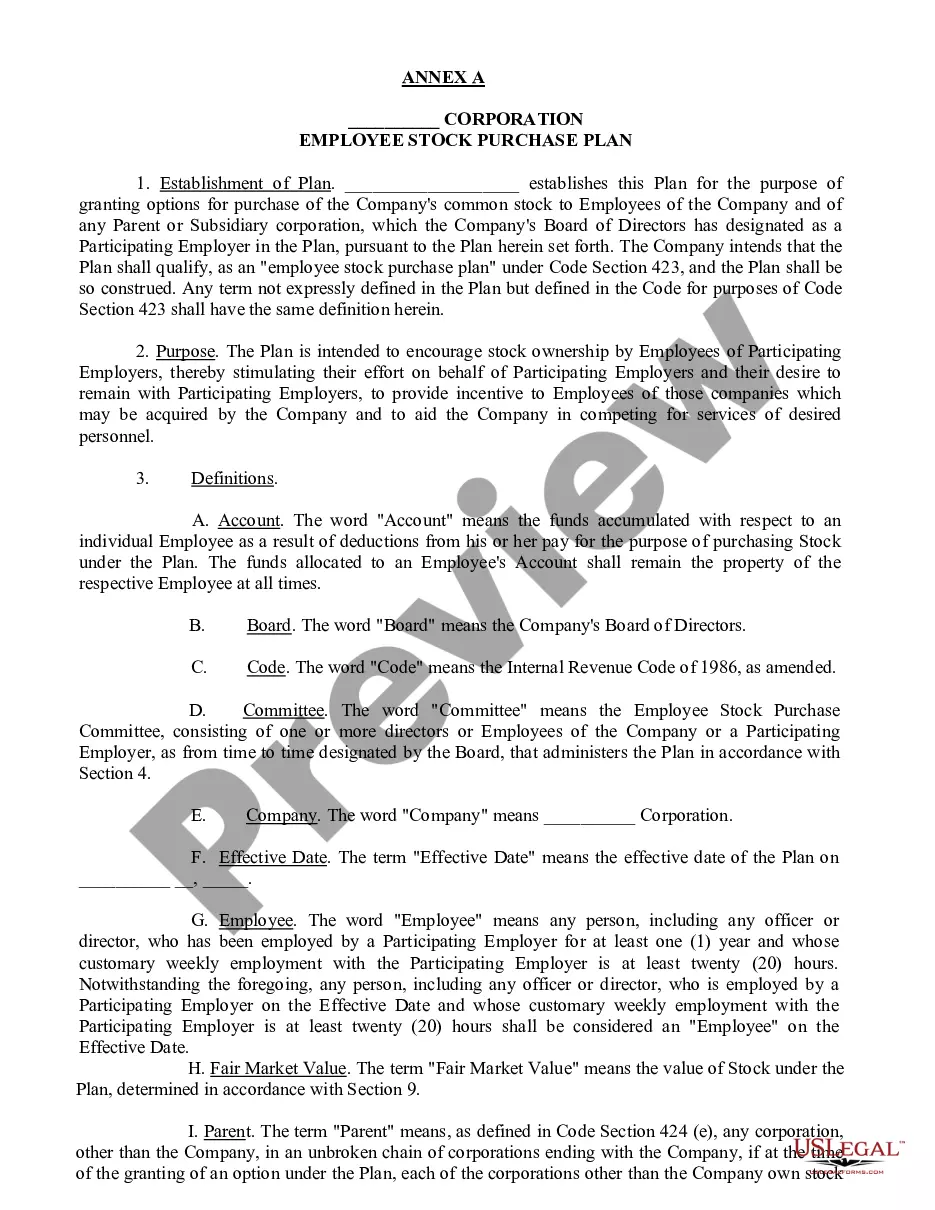

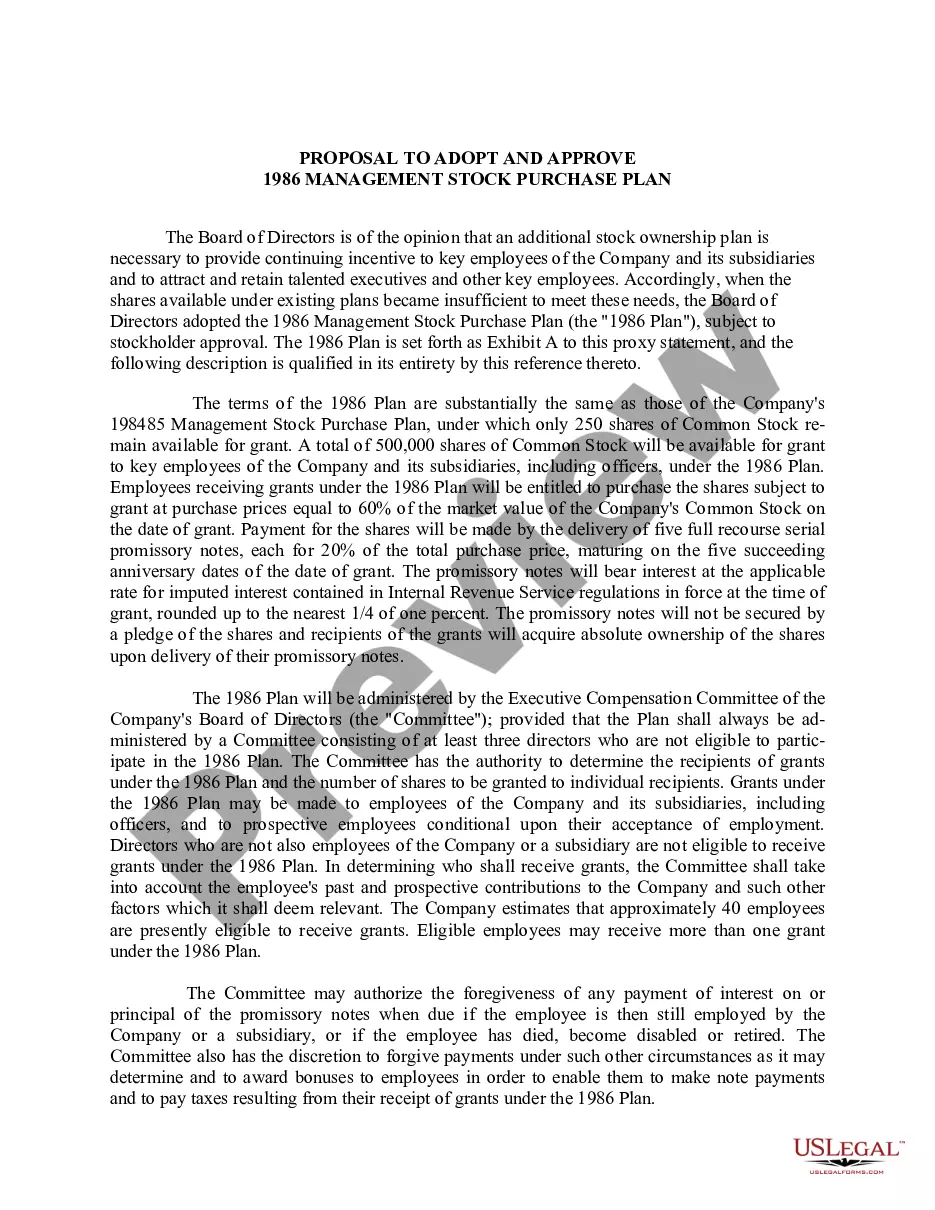

Approval of Company Employee Stock Purchase Plan

What is this form?

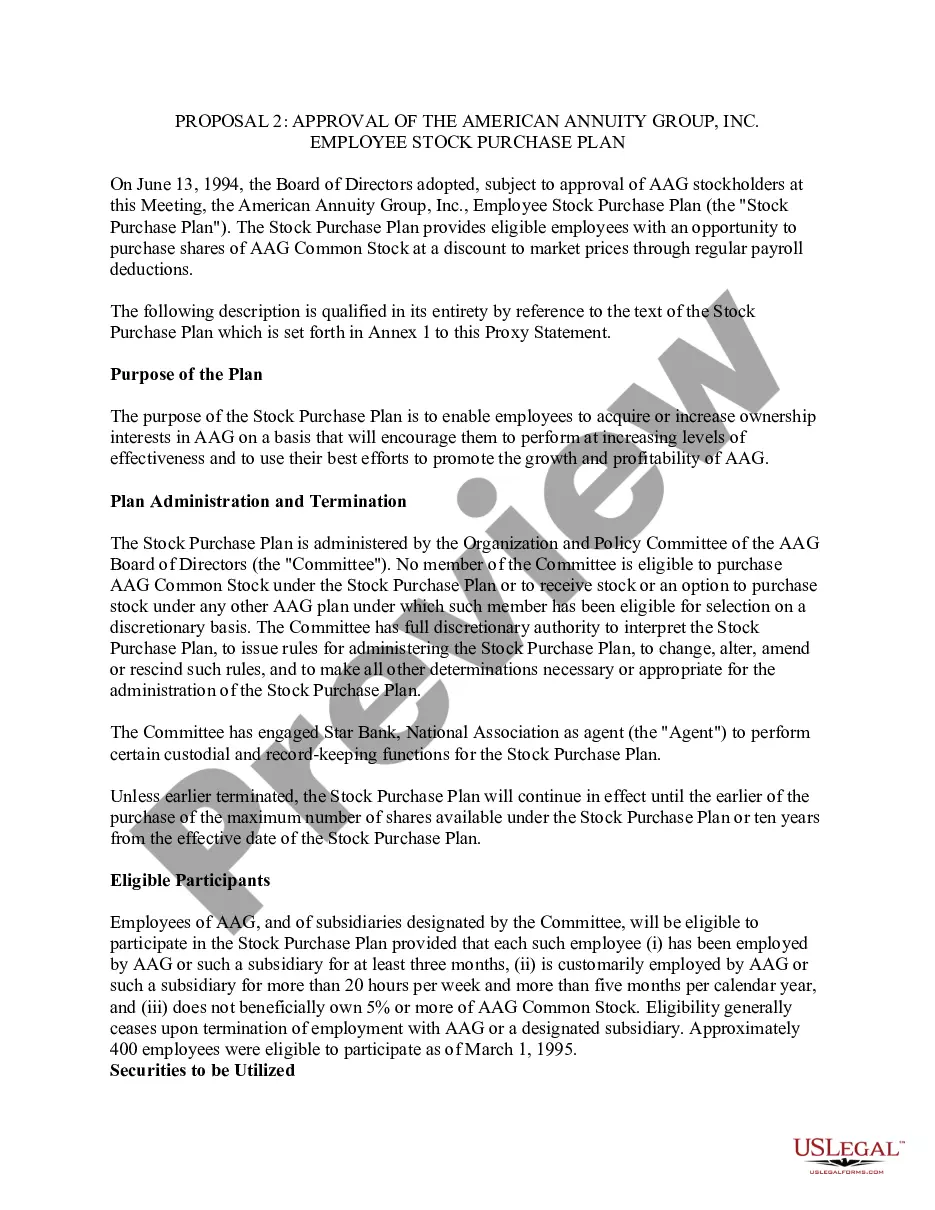

The Approval of Company Employee Stock Purchase Plan is a formal document used by companies to implement a stock purchase plan for eligible employees. This plan incentivizes employee ownership in the company and encourages retention. Unlike other employment documents, this form specifically details the terms and conditions related to the purchase of company stock by employees under IRS Section 423 guidelines.

Main sections of this form

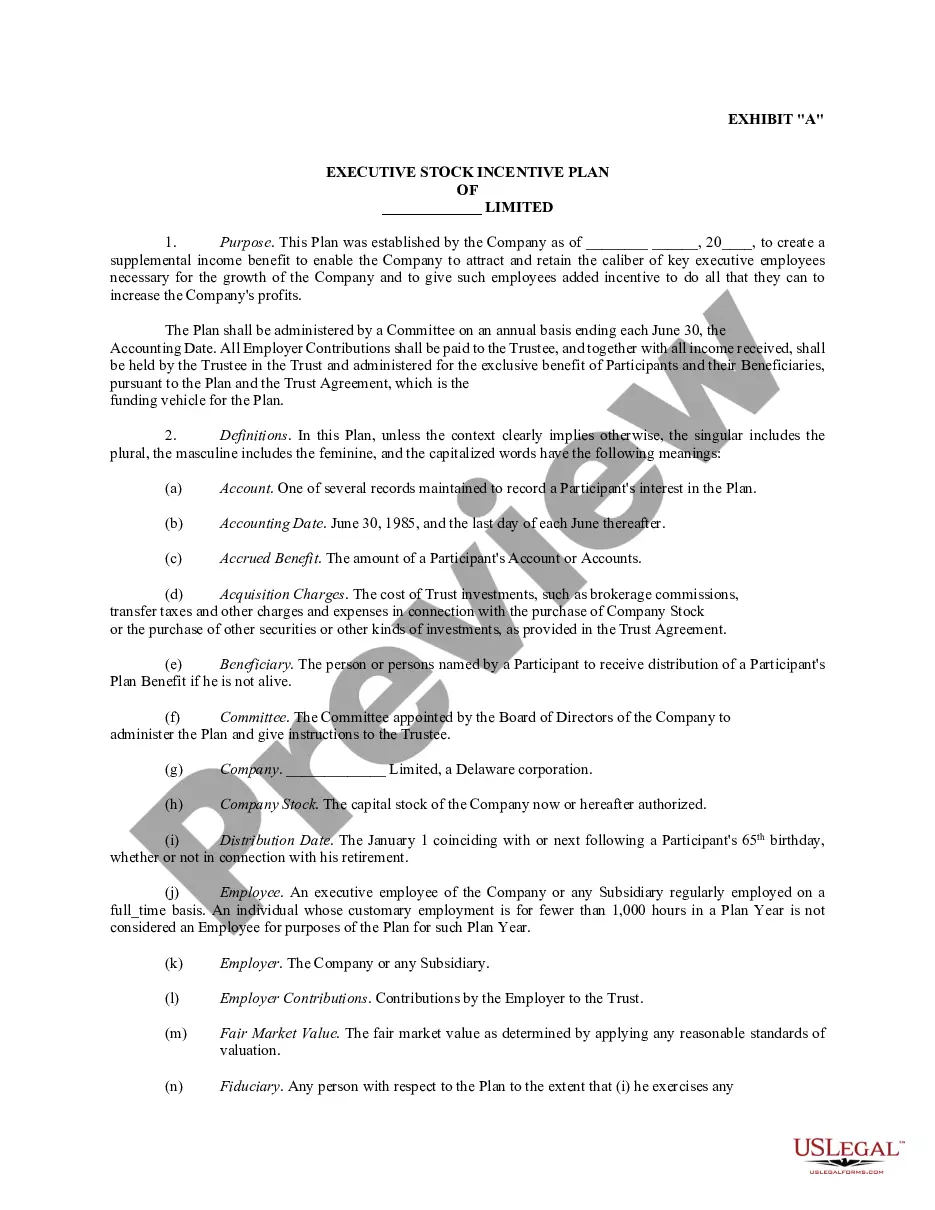

- Adoption date of the Employee Stock Purchase Plan by the Board of Directors.

- Eligibility criteria for employees to participate in the plan.

- Provisions related to the number of shares available and duration of offerings.

- Details on subscription agreements and payroll deductions for participation.

- Terms regarding the exercise of options and implications of employment termination.

- Federal income tax consequences associated with stock purchase under the plan.

When to use this form

This form is used when a company decides to establish a stock purchase plan for its employees. It is relevant during the introduction phase of such a program, especially when the Board of Directors seeks to formally approve and adopt the plan. It is also utilized during annual meetings where shareholder approval is sought.

Who needs this form

- Companies looking to implement an Employee Stock Purchase Plan.

- Corporate Boards of Directors responsible for approving employee stock plans.

- Human resource professionals managing employee compensation packages.

- Legal representatives drafting or reviewing corporate governance documents.

Steps to complete this form

- Fill in the adoption date of the Employee Stock Purchase Plan.

- Specify the eligibility criteria, including minimum employment duration and hours worked.

- Determine the number of shares reserved for issuance under the plan.

- Outline the terms for payroll deductions and subscription agreements for employees.

- Include details on tax implications related to the stock options offered.

Is notarization required?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to specify eligibility criteria clearly, which may cause confusion among employees.

- Not updating the form as per the latest tax regulations, leading to compliance issues.

- Leaving out critical details about the number of shares available, which could affect employee participation.

Advantages of online completion

- Convenient access to a legally reviewed form tailored for your company's needs.

- Editable fields allow for customization to ensure compliance with specific corporate requirements.

- Secure storage and easy retrieval of your corporate documents at any time.

Legal use & context

- The plan must comply with Internal Revenue Code Section 423 for favorable tax treatment.

- It is crucial to ensure all eligible employees are informed about their rights under the plan.

- Maintaining accurate records of stock offerings is essential for IRS compliance and employee transparency.

What to keep in mind

- The Approval of Company Employee Stock Purchase Plan establishes a framework for employee ownership.

- It outlines the responsibilities of the Compensation Committee and eligibility requirements.

- Companies must ensure compliance with relevant tax laws and stakeholder interests during plan execution.

Looking for another form?

Form popularity

FAQ

ESPPs can be either qualified or non-qualified. Qualified plans are more common and must adhere to the rules laid out in Section 423 of the Internal Revenue Code. However, qualified ESPPs should not be confused with qualified retirement plans that grow tax-deferred and are subject to ERISA regulations.

Insiders are legally permitted to buy and sell shares, but the transactions must be registered with the SEC. Legal insider trading happens often, such as when a CEO buys back company shares, or when employees buy stock in the company where they work.

When you buy stock under an employee stock purchase plan (ESPP), the income isn't taxable at the time you buy it. You'll recognize the income and pay tax on it when you sell the stock. When you sell the stock, the income can be either ordinary or capital gain.

A qualified ESPP is a plan which is designed and operates according to Internal Revenue Section 423 regulations. Under a qualified ESPP, employees purchase stock at a discount from the fair market value, yet do not owe taxes on that discount at the time of purchase.

An employee stock purchase plan is an employee benefit that allows you to purchase shares of your employer's company stock. It's a convenient way to buy the shares, thanks to the fact that contributions are often deducted pre-tax directly from payroll.

A qualified stock option is a type of company share option granted exclusively to employees. It confers an income tax benefit when exercised. Qualified stock options are also referred to as "incentive stock options" or "incentive share options."

An employee stock purchase plan (ESPP) is a company-run program in which participating employees can purchase company stock at a discounted price.At the purchase date, the company uses the employee's accumulated funds to purchase stock in the company on behalf of the participating employees.

Non-qualified ESPPs are plans that do not meet the criteria outlined in Section 423 of the Code. A non-qualified ESPP may look exactly like a qualified ESPP, but it doesn't generate the same tax benefits to employees as a qualified plan.

An employee stock purchase plan (ESPP) is a company-run program in which participating employees can purchase company stock at a discounted price.At the purchase date, the company uses the employee's accumulated funds to purchase stock in the company on behalf of the participating employees.