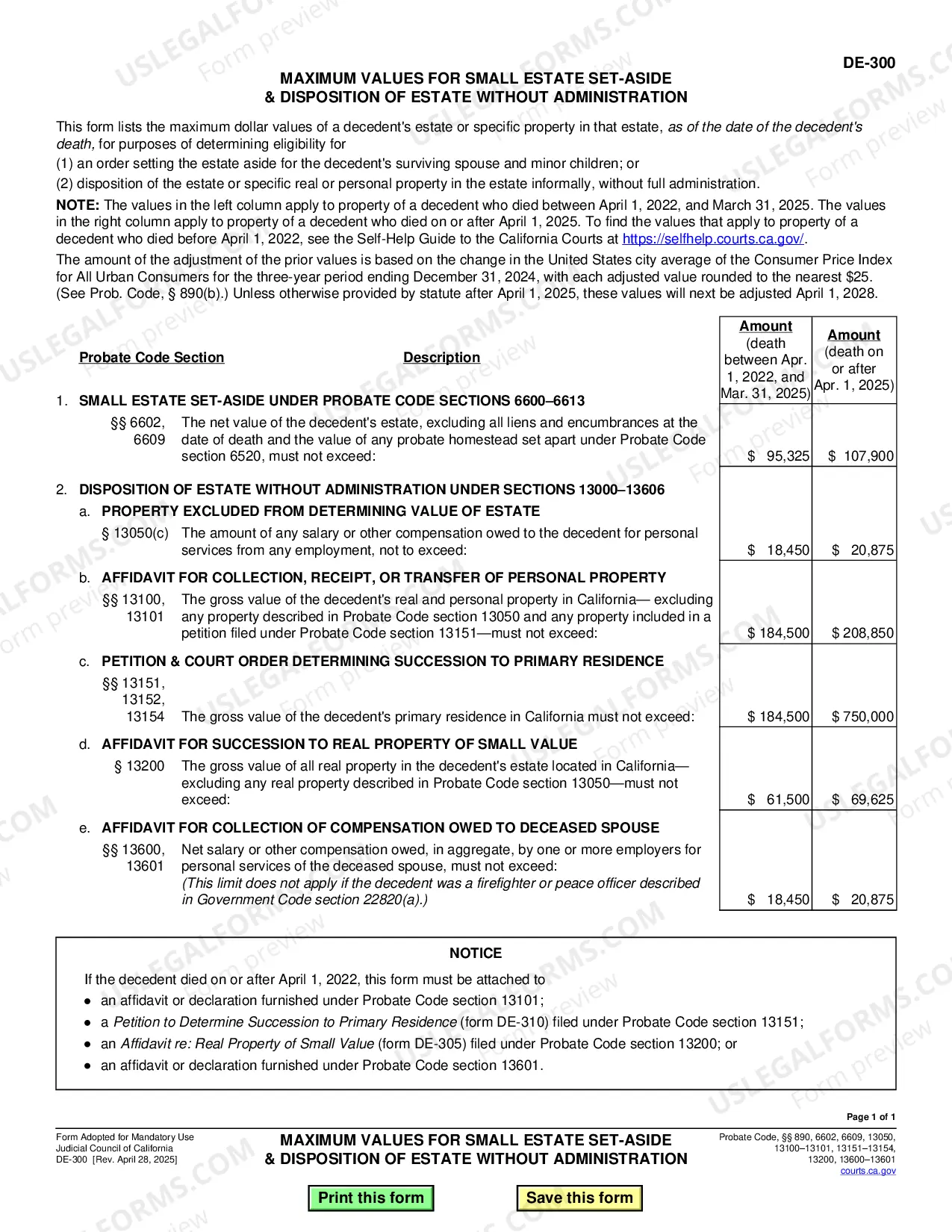

Judgment Foreclosing Mortgage and Ordering Sale

About this form

The Judgment Foreclosing Mortgage and Ordering Sale is a legal document used in judicial foreclosure cases. Unlike non-judicial foreclosures, which do not require court intervention, this form is needed when a mortgage or trust deed lacks a power of sale clause, mandating the lender to seek a court ruling to foreclose. This form outlines the court's decision to order the sale of the mortgaged property to satisfy the debt owed by the borrower.

Form components explained

- Parties involved: Identification of the plaintiff and defendant.

- Judgment details: Court's findings, including amounts due and property descriptions.

- Order for sale: Specifies how and when the property should be sold at public auction.

- Financial obligations: Outlines the distribution of sale proceeds and liabilities of the defendant.

- Property description: Provides specific details about the property being foreclosed.

When to use this document

This form should be used in situations where a lender needs to foreclose on a mortgage through the court system. It is typically necessary when a borrower has defaulted on payments and the mortgage does not include a power of sale clause. Use this form to ensure compliance with court requirements and to facilitate the sale of the property to recover owed debts.

Intended users of this form

- Lenders or mortgage holders seeking to recover debts through judicial foreclosure.

- Borrowers facing foreclosure who need to respond to a lender's court action.

- Attorneys representing clients in mortgage foreclosure proceedings.

How to complete this form

- Identify and list the parties involved in the foreclosure case.

- Enter the court's cause number and the date of the court's decision.

- Specify the details of the property to be sold, including its legal description and location.

- Indicate financial amounts to be paid from the sale proceeds, including debts and attorney fees.

- Finalize the document with signatures from the judge and relevant officials, along with necessary certifications.

Notarization requirements for this form

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include accurate property descriptions, which can lead to legal disputes.

- Omitting signatures from required parties, invalidating the form.

- Forgetting to enter the correct cause number or court details.

Why use this form online

- Convenience of downloading and completing the form at your own pace.

- Access to reusable templates that can be easily edited to meet specific needs.

- Reliability of having forms drafted by licensed attorneys to ensure legality.

Looking for another form?

Form popularity

FAQ

Phase 1: Payment Default. Phase 2: Notice of Default. Phase 3: Notice of Trustee's Sale. Phase 4: Trustee's Sale. Phase 5: Real Estate Owned (REO) Phase 6: Eviction. The Bottom Line.

When a junior mortgage holder has been sold-out in a first-mortgage foreclosure, that junior mortgage holder usually can, depending on state law, sue you personally on the promissory note to recover the money it loaned you.

When a junior lienholder forecloses, a senior lienholder recovers nothing from the sale proceeds. But the senior lien remains intact and the foreclosure buyer takes title to the property subject to the senior lien.

Yes, a second mortgage holder can foreclose, even if you are current on your first mortgage.After taking care of expenses, the mortgages will be paid off in order of priority; until the first mortgage is fully paid off, the second mortgage holder will not receive any funds.

If a foreclosure sale results in excess proceeds, the lender doesn't get to keep that money. The lender is entitled to an amount that's sufficient to pay off the outstanding balance of the loan plus the costs associated with the foreclosure and salebut no more.

You get behind in your mortgage payments. The bank sends a letter notifying you of its intent to begin foreclosure. The bank files a lawsuit. The bank gives you notice of the lawsuit. You have a chance to respond.

Following a first-mortgage foreclosure, all junior liens (including a second mortgage and any junior judgment liens) are extinguished and the liens are removed from the property title. But the second-mortgage debt and creditor's judgment remain, even though they're no longer attached to the foreclosed property.

Following a first-mortgage foreclosure, all junior liens (including a second mortgage and any junior judgment liens) are extinguished and the liens are removed from the property title. But the second-mortgage debt and creditor's judgment remain, even though they're no longer attached to the foreclosed property.