Notice of Default under Security Agreement in Purchase of Mobile Home

What is this form?

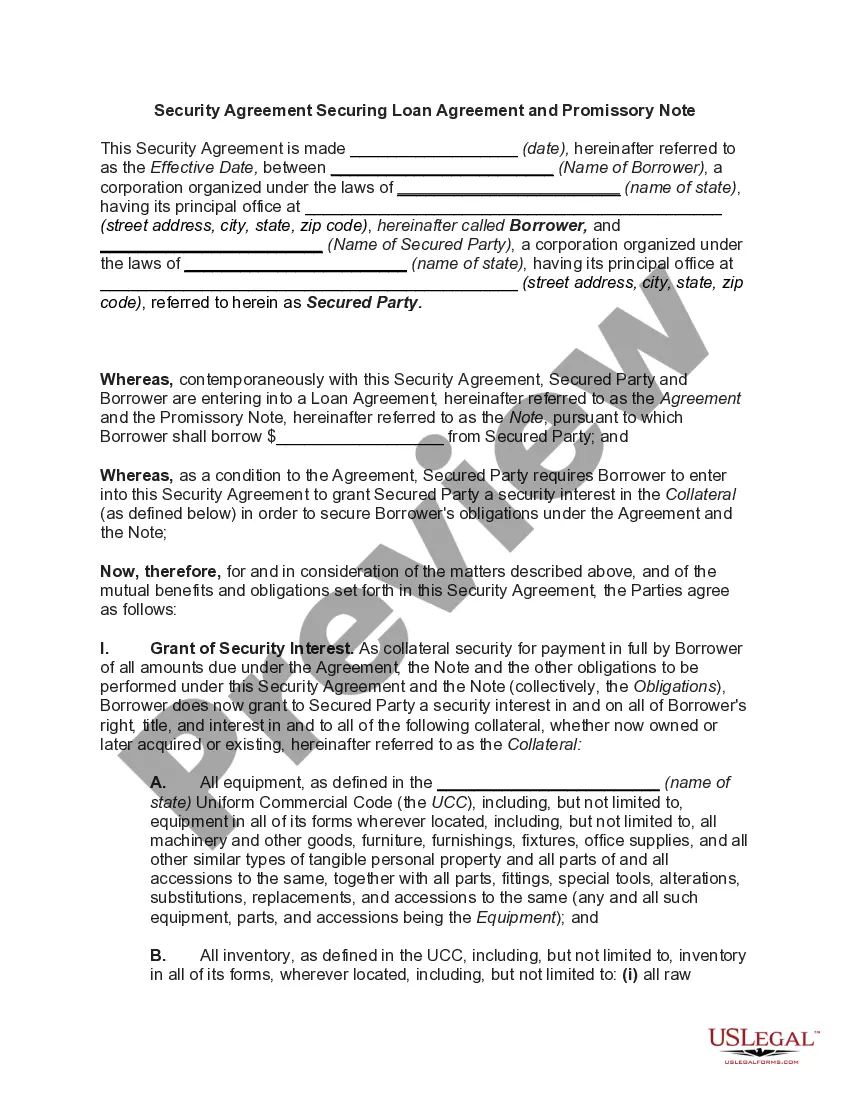

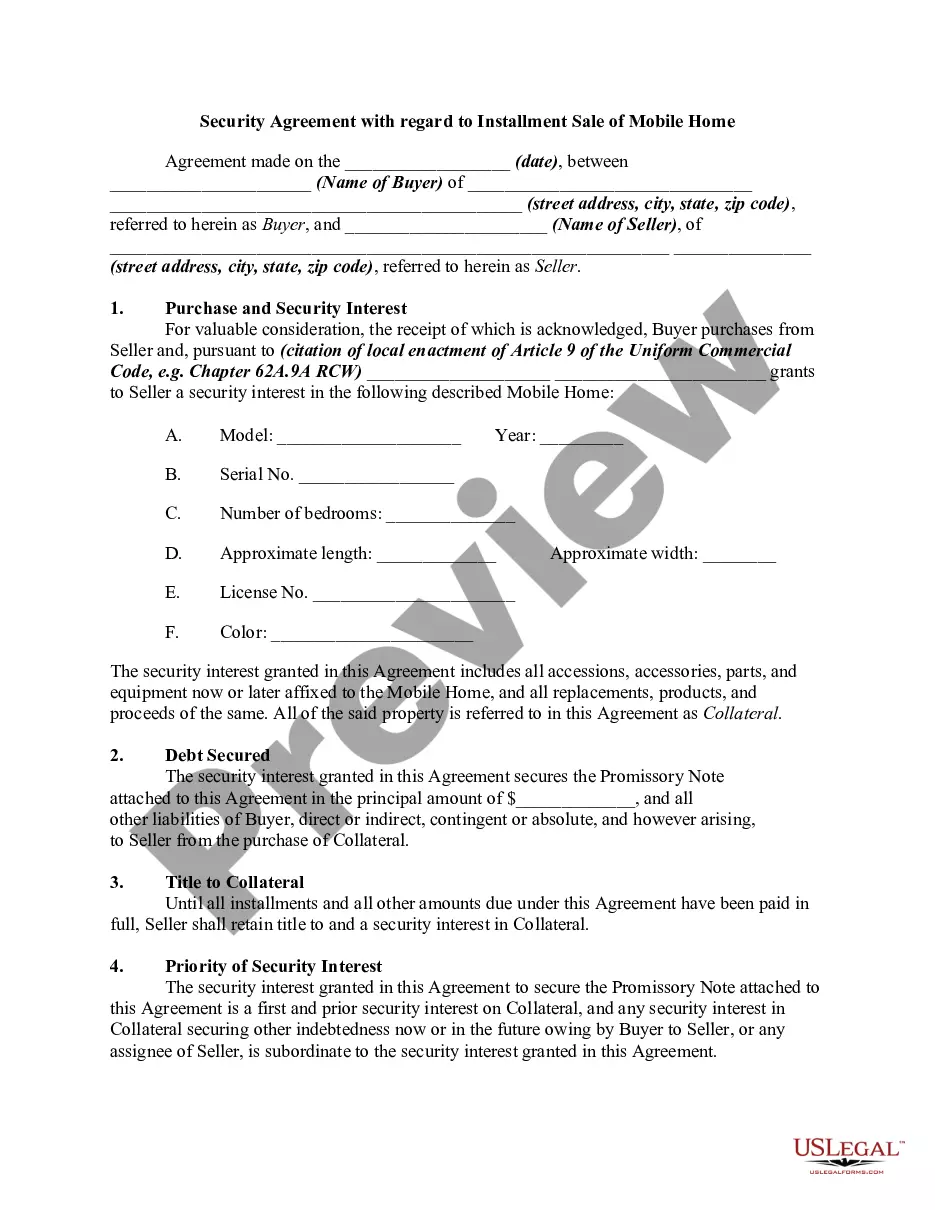

The Notice of Default under Security Agreement in Purchase of Mobile Home is a legal document that notifies a mobile home owner of their default under a financing agreement. This form allows a creditor to inform the debtor of the specific nature of the default and the creditor's rights to repossess the mobile home if the debt is not cured. Unlike general default notices, this form is tailored for secured transactions involving mobile homes, ensuring compliance with specific legal requirements associated with personal property collateral.

Key components of this form

- Name and address of the mobile home owner.

- Details of the security agreement and description of the default.

- Information on how to cure the default.

- Outstanding amounts owed, including any fees or expenses.

- Signatures of the creditor and date of the document.

When to use this form

This form should be used when a mobile home owner has failed to meet the obligations outlined in their security agreement. It is applicable when the creditor intends to take legal action to repossess the mobile home due to non-payment or other default conditions. The notice is a formal requirement that ensures the debtor is informed of their legal standing and provides an opportunity to remedy the situation before the repossession occurs.

Who this form is for

- Creditors who have a secured interest in a mobile home.

- Mobile home owners who are facing default on their security agreements.

- Legal professionals assisting clients in secured transactions.

How to complete this form

- Identify the mobile home owner by entering their name and address at the top of the form.

- Describe the security agreement, including any relevant details about the transaction.

- Clearly state the nature of the default to inform the debtor of the specific issues.

- Indicate what actions the debtor can take to cure the default, including any necessary payments.

- Have the creditor sign and date the form to execute it formally.

Notarization requirements for this form

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide detailed information about the default.

- Not clearly stating the cure options available to the debtor.

- Leaving out the creditor's signature or date, which can invalidate the notice.

Benefits of using this form online

- Convenience of downloading and printing the form instantly.

- Editable fields allow you to customize the document for your specific situation.

- Access to forms drafted by licensed attorneys, ensuring legal accuracy.

Legal use & context

- The Notice of Default serves as a formal legal requirement, providing notice to the mobile home owner.

- Using this form promotes transparency in the collection process for creditors.

- The content of the form must comply with state laws regarding repossession and secured interests.

Main things to remember

- The form is vital for creditors seeking to notify mobile home owners of default.

- Proper completion and delivery of the notice are essential to uphold legal rights.

- Users should be aware of state-specific requirements for repossession processes.

Looking for another form?

Form popularity

FAQ

Voluntary repossession. In a voluntary repossession, the homeowner voluntarily surrenders the home to the lender. If a manufactured home is wrapped up with the land as collateral for the loan, the lender will likely forecloseeven if the manufactured home is still classified as personal property.

You can pay off the difference of the mortgage right away if you have the cash on hand. You could also take out a loan for less money with a lower interest rate than the mortgage. Another option you have is to short sale your mobile home.

After a repossession order, you have no house, but you may still have the debt. This depends on how much of your mortgage is unpaid. If the mortgage amount due is low, the bank or lender will return you your money after paying all the fees and recovering its debt once the sale is made.

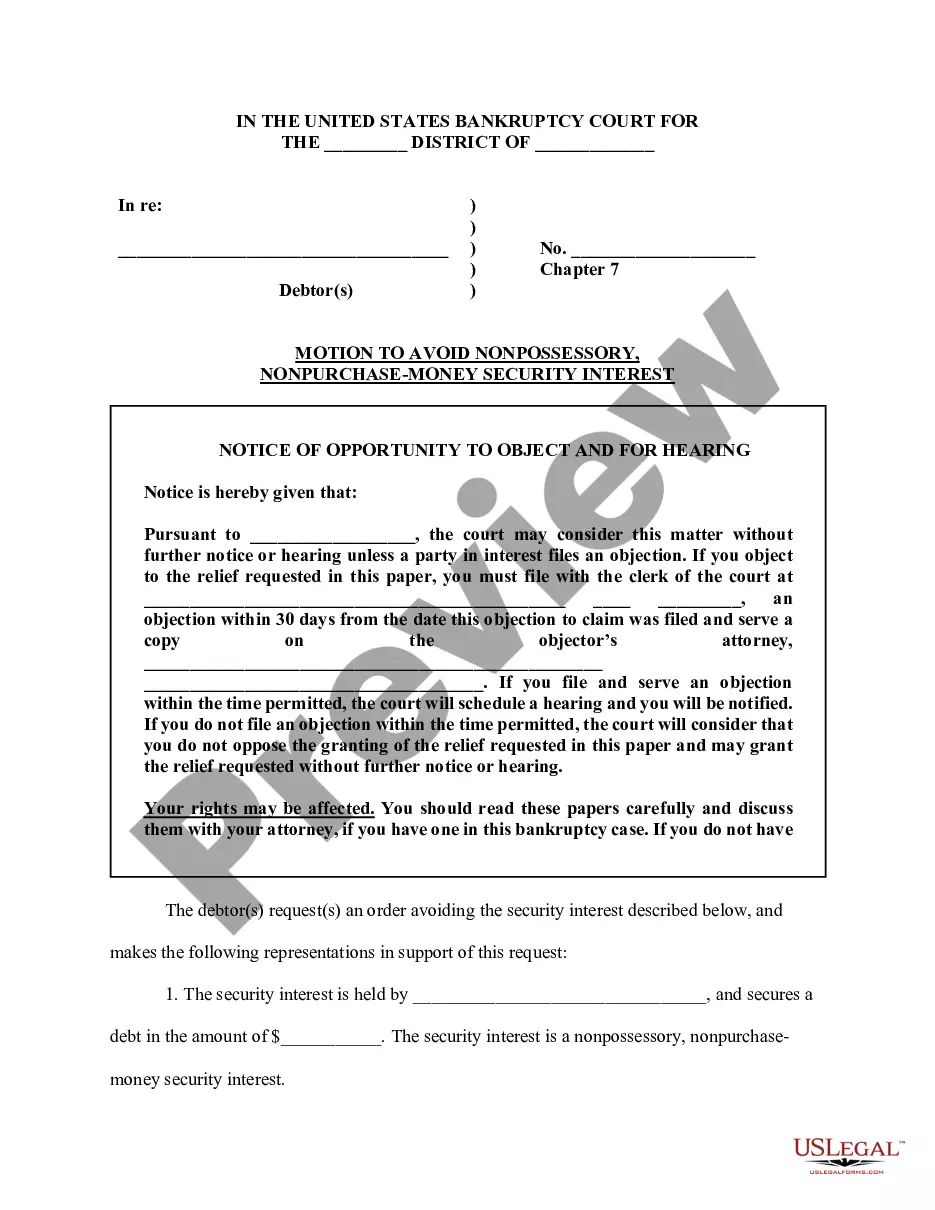

The term purchase money security interest (PMSI) refers to a legal claim that allows a lender to either repossess property financed with its loan or to demand repayment in cash if the borrower defaults. It gives the lender priority over claims made by other creditors.

What Happens if the Manufactured Homeowner Defaults on the Loan? If the borrower defaults on loan payments for a manufactured home, the creditor can repossess or foreclose the home.Generally, if the home is personal property, the creditor repossesses the home.

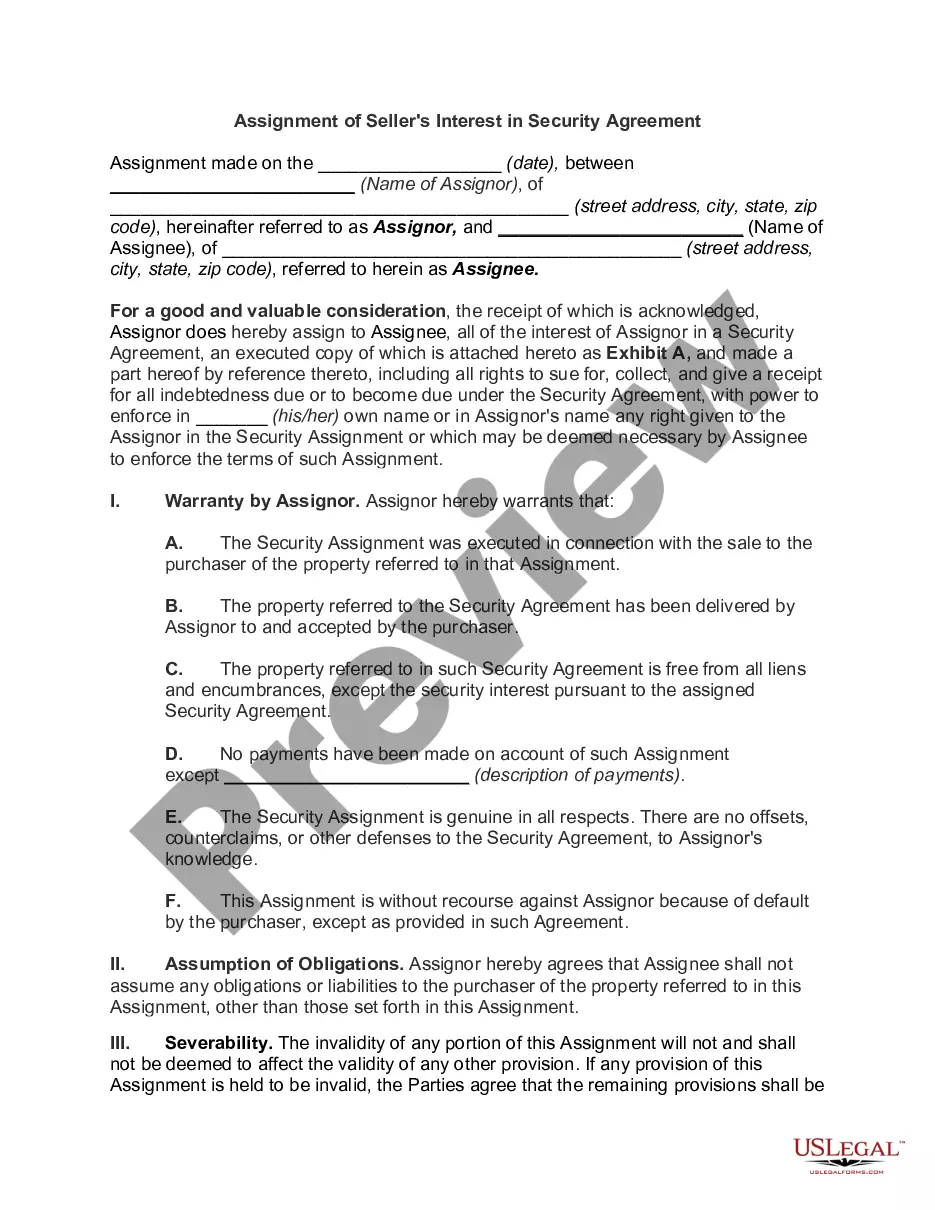

A security agreement is a document that provides a lender a security interest in a specified asset or property that is pledged as collateral. Security agreements often contain covenants that outline provisions for the advancement of funds, a repayment schedule, or insurance requirements.

A repossession takes seven years to come off your credit report. That seven-year countdown starts from the date of the first missed payment that led to the repossession. When you finance a vehicle, the lender owns it until it is completely paid off.