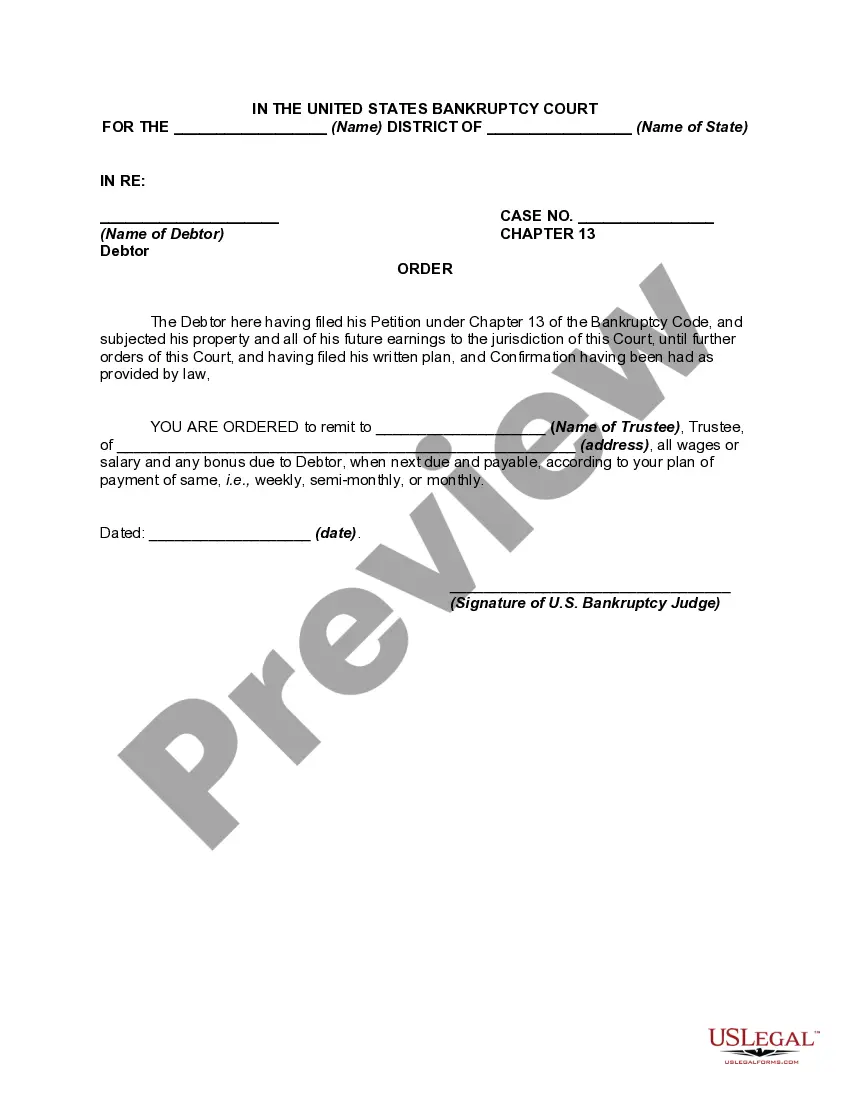

Order Requiring Debtor's Employer to Remit Deductions from a Debtor's Income to Trustee

Overview of this form

The Order Requiring Debtor's Employer to Remit Deductions from a Debtor's Income to Trustee is a legal document used in the context of Chapter 13 bankruptcy. This form allows a court to require an employer to deduct specified amounts from the debtor's income and remit them to a bankruptcy trustee. This process facilitates structured repayment of debts as outlined in a confirmed Chapter 13 repayment plan.

Key parts of this document

- Name of the court and jurisdiction

- Name and case number of the debtor

- Details of the trustee including their address

- Specified dollar amount to be deducted from the debtorâs income

- Source of income from which deductions will be made

- Start and end dates for the deductions

Situations where this form applies

This form is used when a debtor has filed for Chapter 13 bankruptcy and has a confirmed repayment plan. It is necessary when the court orders the debtor's employer to make income deductions to ensure that payments are made to the bankruptcy trustee in accordance with the plan.

Intended users of this form

- Individuals who are filing for Chapter 13 bankruptcy

- Debtors who require their employer to deduct payments from their income

- Bankruptcy trustees overseeing the repayment plans

- Employers responsible for processing income deductions for employees in bankruptcy

How to complete this form

- Identify the appropriate court name and jurisdiction.

- Fill in the debtorâs name and case number accurately.

- Enter the name and address of the trustee overseeing the bankruptcy.

- Specify the amount to be deducted from the debtor's income and the income source.

- Indicate the start and end dates for the deductions as stipulated in the repayment plan.

- Obtain the signature of the U.S. Bankruptcy Judge to finalize the order.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. Always check your jurisdiction's requirements to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include the correct case number or debtor's full name.

- Not specifying the exact amount to be deducted from income.

- Leaving out the start and end dates for the deduction schedule.

- Omitting the trustee's accurate contact information.

Benefits of completing this form online

- Convenient access to the form anytime, from anywhere.

- Editable document that can be tailored to individual needs.

- Ensures compliance with current legal requirements and standards.

- Quickly downloadable for immediate use in bankruptcy proceedings.

Main things to remember

- The form is essential in Chapter 13 bankruptcy cases for enforcing income deductions.

- It must be completed accurately to ensure compliance with court orders.

- Direct income deductions help facilitate timely payments to the bankruptcy trustee.

Looking for another form?

Form popularity

FAQ

In both cases, the bankruptcy court can discharge certain debts. Once a debt has been discharged, the creditor can no longer take action against the debtor, such as attempting to collect the debt or seize any collateral. Not all debts can be discharged, however, and some are very difficult to get discharged.

Chapter 7 is the most common type of bankruptcy and is often referred to as a straight bankruptcy. Under Chapter 7, you can eliminate most of your unsecured debts and some secured debts by surrendering your assets. Unsecured debts are debts not secured with collateral, including most personal loans and credit cards.

The potential disadvantages of bankruptcy include: Loss of credit cards. Many credit card companies automatically cancel any cards you hold when you file. You will probably receive numerous offers to apply for unsecured credit cards after filing.

Bankruptcy is a legal status that usually lasts for a year and can be a way to clear debts you can't pay. When you're bankrupt, your non-essential assets (property and what you own) and excess income are used to pay off your creditors (people you owe money to). At the end of the bankruptcy, most debts are cancelled.