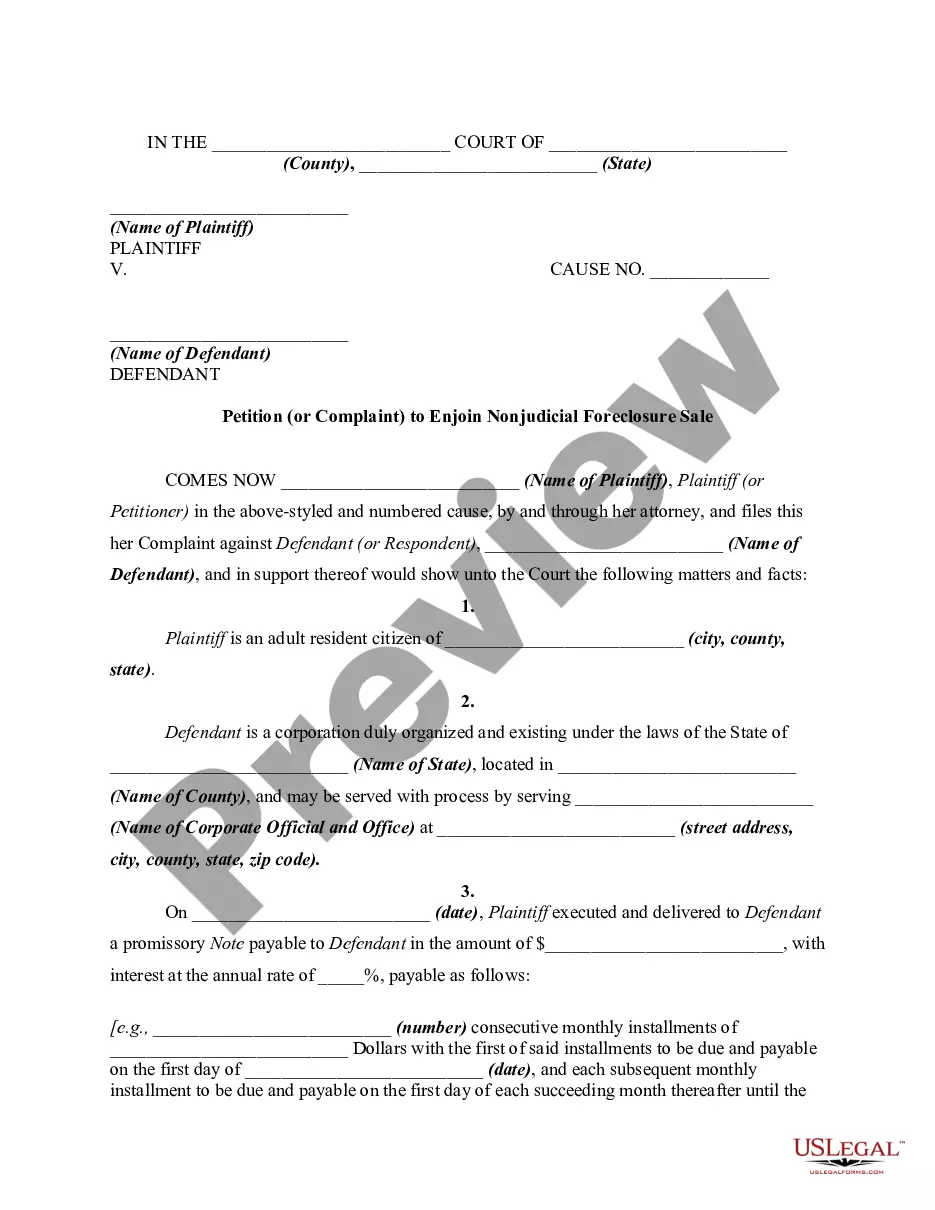

Petition to Enjoin Foreclosure Sale and Seeking Ascertainment of Amount Owed on Note and Deed of Trust

What this document covers

The Petition to Enjoin Foreclosure Sale and Seeking Ascertainment of Amount Owed on Note and Deed of Trust is a legal document used to request a court to stop a foreclosure sale. This form is essential when the borrower believes that the enforcement of the mortgage would be inequitable and cause irreparable harm. It differs from other foreclosure-related forms by specifically seeking to ascertain the amount owed on a note and deed of trust before the foreclosure proceeds.

What’s included in this form

- Names of the plaintiff and defendants involved in the case.

- Details about the property, including legal description and purchase price.

- Allegations concerning ownership and amounts owed.

- Requests for a preliminary injunction against the foreclosure.

- Demand for the court to ascertain the amount that may be due.

- Signature lines for the plaintiff and their attorney.

Common use cases

This form should be used when a borrower seeks to prevent a foreclosure sale on their property due to uncertainties surrounding the owed amounts. It is particularly needed in situations where the borrower believes they have overpaid or disputed ownership claims related to the property being foreclosed upon. Use this form if a foreclosure sale is imminent and you do not have another legal remedy to resolve the situation.

Who can use this document

- Borrowers facing foreclosure proceedings.

- Homeowners disputing the amount owed on a mortgage.

- Individuals involved in legal disputes regarding property ownership.

- Attorneys representing clients in foreclosure cases.

Steps to complete this form

- Identify and enter the names of the plaintiff and defendants at the beginning of the form.

- Provide personal information including the residence of the plaintiff and defendants.

- Fill in the details concerning the property, including purchase date and legal description.

- State the amount paid for the property and mention any outstanding amounts relevant to the note.

- Include your requests for the court's intervention and provide relevant evidence showing a need for action.

- Sign the document and have your attorney (if applicable) also sign and complete their information.

Notarization guidance

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all necessary parties in the lawsuit.

- Not providing adequate details about the property and the situation leading to the foreclosure.

- Missing signatures or improperly completed notarization, if required.

- Submitting the petition too late, missing court-mandated deadlines for foreclosure defense.

Benefits of using this form online

- Convenient access allows for completion at your own pace.

- Editable templates make it easy to customize the document to your specific situation.

- Reliable resources provided by licensed attorneys ensure legal compliance.

Looking for another form?

Form popularity

FAQ

This petition is a court filing used to pause a foreclosure sale and to have the court determine the exact amount owed on the note and deed of trust. It is intended for borrowers who believe enforcing the mortgage would be inequitable or that the amount due is disputed. It’s used when a foreclosure sale is imminent and other remedies are not available.

Filing this petition does not automatically require paying the entire unpaid balance. The form seeks a preliminary injunction to stop the foreclosure and a court determination of the amount owed on the note and deed of trust, which may affect what must be paid. The outcome depends on the court’s assessment of the asserted amounts.

Borrowers and lenders may choose a deed of trust because it creates a security interest tied to the property and, in some contexts, may involve a different foreclosure process than a mortgage. This form addresses disputes tied to that instrument by seeking to enjoin foreclosure and to ascertain amounts owed on the note and deed of trust.

In some jurisdictions, a deed of trust may permit nonjudicial foreclosure, which can be faster than a judicial foreclosure on a mortgage. This form, however, pauses the process with a preliminary injunction and requires the court to determine the exact amount owed, ensuring accurate payment decisions before any sale proceeds.

This form requires identifying the plaintiff, defendants, and property details, including ownership. Whether one is on the deed or the mortgage can affect standing and claims in a foreclosure case, but the form’s purpose is to stop the sale and ascertain the amount owed on the note and deed of trust.

This Petition uniquely combines an injunction to halt the foreclosure sale with a separate request for the court to ascertain the amount owed on the note and deed of trust, using the ownership and property details listed. Other foreclosure forms may seek only to stop a sale or pursue standard remedies without determining the exact unpaid amount.