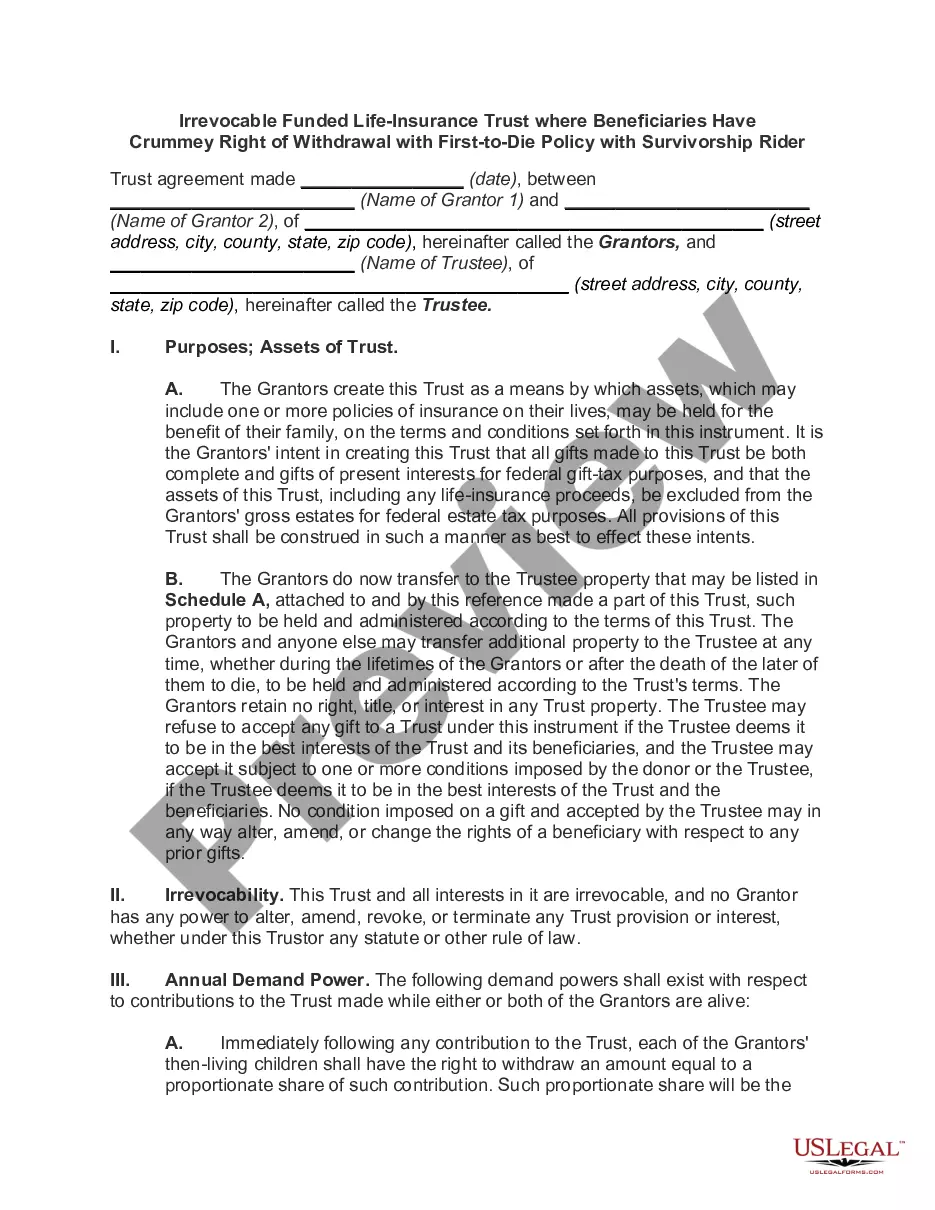

Irrevocable Trust Funded by Life Insurance

Overview of this form

The Irrevocable Trust Funded by Life Insurance is a legal document that establishes a trust where life insurance policies and other assets are placed for the benefit of designated beneficiaries. This form is distinct because it provides significant estate tax savings and grants flexibility in managing the assets, unlike traditional life insurance policies that may limit distribution options. By using this form, individuals can ensure their chosen beneficiaries receive the insurance proceeds without the delay of probate, while also helping to minimize estate taxes upon their death.

Key components of this form

- Identification of the Trustor and Trustee, including their names and contact details.

- Transfer of assets, including life insurance policies and other properties into the trust.

- Trustee's rights and responsibilities regarding the management of the trust estate.

- Instructions for premium payments and managing income generated from the trust.

- Procedures for the disposition of trust assets after the Trustor's death.

- Provisions regarding the irrevocability of the trust and the powers granted to the Trustee.

Common use cases

This form should be used when an individual (Trustor) wishes to create an irrevocable trust specifically benefiting from life insurance policies. It is suitable in situations where the Trustor wants to provide financial security to beneficiaries upon their passing, optimize estate taxes, or manage assets more efficiently compared to traditional arrangements. The form is especially beneficial for those with significant life insurance policies looking to minimize their taxable estate.

Intended users of this form

- Individuals seeking to minimize estate taxes through effective asset management.

- Anyone who wishes to ensure that life insurance proceeds are distributed according to their wishes without going through probate.

- People looking for a structured way to manage their insurance policies and other assets for the benefit of their chosen beneficiaries.

- Financial planners and estate attorneys advising clients on trust and estate planning strategies.

Instructions for completing this form

- Identify the parties involved by filling in the names and addresses of the Trustor and Trustee.

- Specify the properties and insurance policies being transferred by listing them in the designated exhibits.

- Detail how the trust income should be managed and distributed during the Trustor's lifetime.

- Include instructions for the distribution of trust assets after the Trustor's death, ensuring clarity on beneficiary rights.

- Sign and date the agreement, ensuring compliance with any additional state requirements.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, notarization can add an extra layer of validity and credibility to the document.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to adequately identify all assets to be included in the trust.

- Not clearly defining the powers and responsibilities of the Trustee.

- Omitting beneficiary designations or providing unclear instructions for asset distribution.

- Neglecting to review state-specific requirements that could affect trust validity.

Benefits of completing this form online

- Convenient access to legal documents that can be downloaded and customized easily.

- Editability allows users to tailor the trust agreement to their specific needs.

- Reliability, as the forms are drafted by licensed attorneys to ensure legal compliance.

Summary of main points

- The Irrevocable Trust Funded by Life Insurance helps manage the proceeds of life insurance for beneficiaries.

- This trust offers significant estate tax advantages and ensures the designated distribution of assets.

- It is crucial to complete the form correctly to avoid common mistakes and ensure compliance with state requirements.

Looking for another form?

Form popularity

FAQ

Contact an Attorney. A trust is a legal entity; therefore an attorney should be consulted to prepare the trust documents. Designate the Trustee. Because the trust will be irrevocable, you are not permitted to act as the trustee. Choose the Beneficiaries. Considerations.

The price to establish a trust varies according to your estates attorney's legal fees. However, expect to pay $1,600 to $2,000. Although setting up a trust is more expensive, it gives you more control over how the funds are spent and when your child gets access to the funds.

Trusts are not considered individuals; therefore, life insurance proceeds paid to trusts are generally subjected to estate tax. Also, the proceeds payable to a trust may not qualify for the inheritance tax exemption provided by some states for insurance payable to a named beneficiary.

Often, trusts are created during the grantor's lifetime, but they aren't funded until after the grantor dies. If you're a trustee of such a trust, there are certain steps to take to transfer assets into the trust: Assist the executor of the estate in making an orderly transfer of assets into the trust.

A life insurance policy can fund a trust that eventually creates some available cash for future expenditures, such as anticipated estate taxes.When the grantor dies, the face value of the policy pays into the trust, bypassing the grantor's probate estate entirely.

Putting your life insurance policy in trust involves a legal arrangement that helps to ensure that the money from that policy is used exactly as you intended, regardless of the value of your estate.It also means that your beneficiaries will receive the money much quicker, whether a will has been written or not.

Gifting cash or other assets to an ILIT is a common and simple funding method. In addition to lifetime exemption gifts, in 2019, each individual has the ability to give an annual gift of $15,000 (indexed for inflation) to another individual each year without incurring any gift taxes.

An irrevocable life insurance trust (ILIT) is created to own and control a term or permanent life insurance policy or policies while the insured is alive, as well as to manage and distribute the proceeds that are paid out upon the insured's death.

An irrevocable life insurance trust (ILIT) is created to own and control a term or permanent life insurance policy or policies while the insured is alive, as well as to manage and distribute the proceeds that are paid out upon the insured's death.